Harvard Housing Study: The Nation’s Market Stays Subdued

Can the industry climb out of the trough?

“The state of the nation’s housing is, in a word, subdued,” said Harvard Joint Center for Housing Studies’ Senior Research Associate Dan McHugh during a webinar on Wednesday. The discussion accompanied the release of the JCHS State of the Nation’s Housing 2026 report.

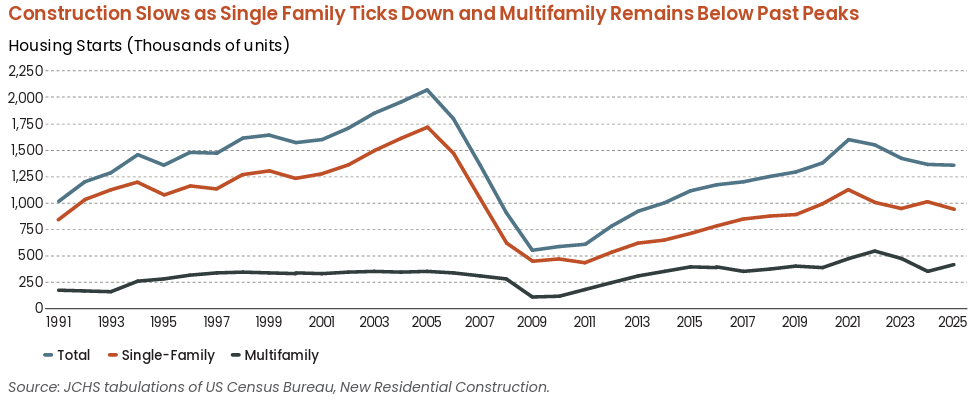

“Construction is down, home sales are flat and costs and cost burdens are up against that backdrop,” McHugh said. “Whether it’s consumer confidence, job growth, population growth or inflation, the underpinnings of housing demand have weakened and activity has slowed as a result.

“Supply shortages are a challenge as well, even as vacancy rates rise and inventories build,” McHugh continued. “Shortages of housing remain most severe at the low end of the market, as evidenced by the crisis of affordability for lower-income households, which continues to be dire.”

Subdued indeed, but not quite everything is gloomy in the housing sector. McHugh also noted that the report found growing momentum in the public sector to address the housing affordability crisis. An increasing number of government actions are being taken, mainly at the state and local level, to remove various construction roadblocks and increase housing development, he said.

Weakening demand, mismatched supply

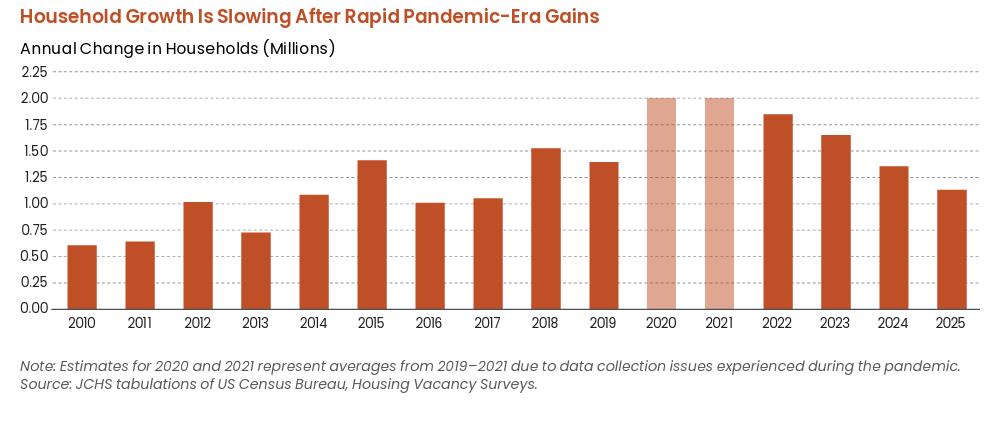

Household formation slowed for the third consecutive year in 2025, according to the report, driving down demand for residential properties. As recently as 2021, U.S. household formation was around 2 million; by 2025,that number was just 1.1 million, which the report calls “consistent with the more modest levels averaged across the 2010s.”

Young adults historically form households more than any other demographic, but the 2020s headwinds against them are particularly brisk: a weakened job market, mountains of student debt and a pessimistic consumer sentiment. Data backs it up: In 2025, the US added only 116,000 jobs, the smallest amount in a non-recession year since 2002, according to the Bureau of Labor Statistics.

At the same time, student debt obligations have become so onerous that student loas that are at least 90 days overdue jumped from less than 1 percent in the Q4 2024 to 10 percent in Q4 2025, and consumer sentiment as measured by the University of Michigan is near historic lows.

Housing demand is further threatened by immigration policy, the report noted, with net international migration halving in 2025 year-over-year. The Census Bureau projects that it will drop another 75 percent in 2026 to just 321,000 immigrants to the United States, roughly a third of the 900,000 averaged annually from 2001 to 2019. This comes at the same time as a significant slowdown in U.S. natural population growth due to fewer births and more deaths.

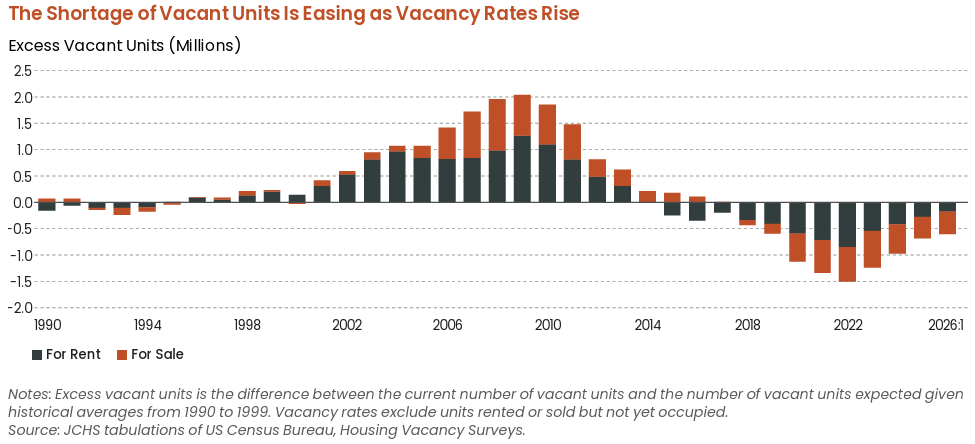

Does the drop in demand mean there will finally be enough housing supply? Unfortunately not, said JCHS Managing Director Chris Herbert during the webinar.

“In 2022 and 2023, by our estimate, we were about 1.5 million units shy of where we needed to be,” Herbert said. “That’s now down to 700,000 units.”

That’s a positive trend, but it is also true overall units are only part of the story. “Even if we get into a place where we have enough supply overall, we still don’t have enough housing that’s affordable for people at the lower end of the income distribution,” Herbert said.

The squeeze is still on renters

Rents fell in many, but not all markets, with the strongest drops in the Sun Belt – markets that previously had seen rapid rent increases and substantial new apartment construction.

That doesn’t mean that rents are low, just not much higher than their post-pandemic highs. In the first quarter of 2026, asking rents for professionally managed apartments were 29 percent higher than in 2020.

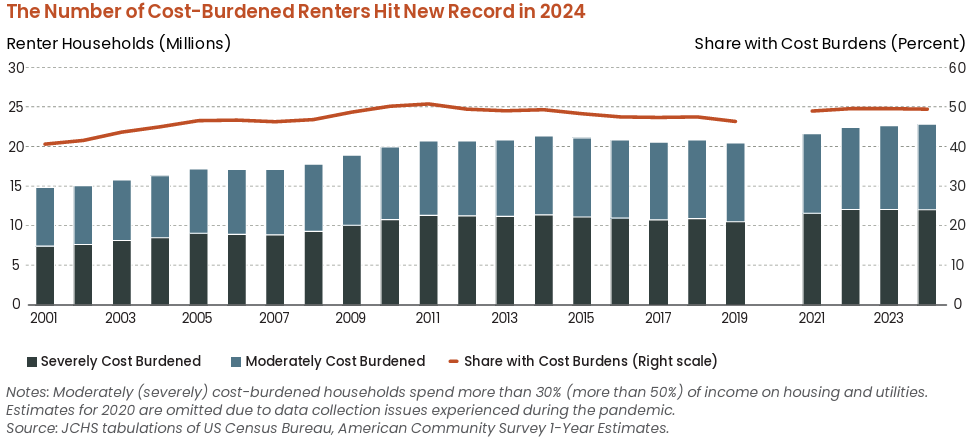

Citing National Low Income Housing Coalition data, the report explained that 11 million households with extremely low incomes competed for 3.8 million affordable and available rental units at last measure in 2024. Overall, renters are especially strained to make ends meet, with cost burdens reaching a new high.

In 2024, 22.7 million renter households (49 percent) were cost burdened, including 12.1 million (26 percent) with severe burdens. Nationwide, the number of cost-burdened renters is up by 2.3 million since 2019.

National Multifamily Housing Council President Sharon Wilson Géno said during the webinar that multifamily absorption rates have stayed “relatively consistent with historic norms,” supported by concessions and other adjustments to get units leased. There is still pent-up demand, she said, since about one-third of people under 30 are still living with their parents. If the price point is right, that demand will absorb new units.

At the same time, multifamily development is lagging, Géno said, as the industry grapples with high construction and capital costs.

READ ALSO: National Multifamily Report

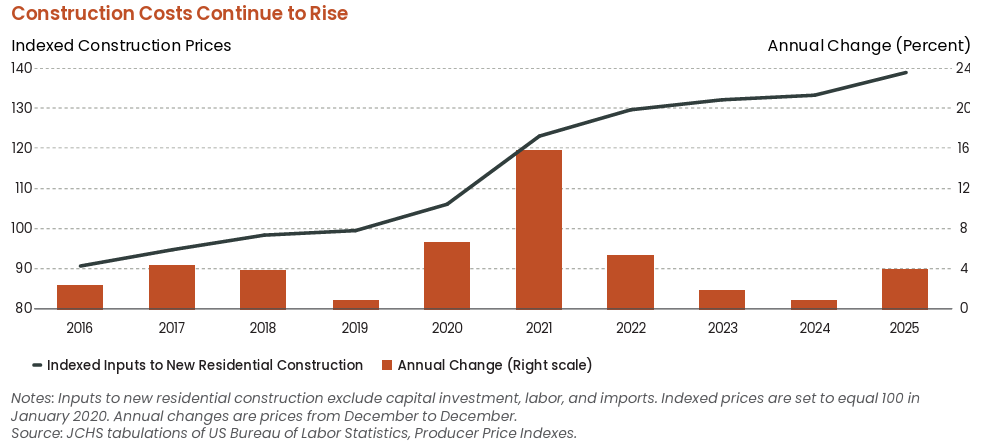

“We saw a surge in construction costs during Covid, and while they flattened off a little bit, and not been as extreme, they haven’t gone down,” she said. “Also, we saw a significant shift in the interest rate environment in 2022 and 2023. We saw, in 2023, as much as 50 percent less production than you would normally see in certain markets.

The situation isn’t quite hopeless, however. Géno also pointed to new technologies as important to the future of the housing market, especially in ways that might help facilitate construction by lowering costs, and easing shortages.

“We’re at this inflection point as a society with the use of technology that promises not only lowering operating costs and improving the experience of residents, but also (to control costs) on the construction side,” Géno said, adding that there’s a real opportunity in the next decade to harness what’s already happening in other sectors and bring it into the housing sector.

Public policy takes aim

According to panelists, the silver lining in U.S. housing is that the problem is so severe now that policymakers from both parties are paying attention, especially at the local and state levels. There has also been some movement at the federal level, such as the expansion of low income housing tax credits last year and the House’s passage of the 21st Century ROAD to Housing Act.

Even so, in light of inadequate federal support, states and localities are expanding their own tools to address affordability, including issuing bonds, creating state LIHTC programs and tapping into more than 800 housing trust funds that collectively generate over $1.6 billion annually, the report found.

Also, state and local governments are encouraging affordable and mixed-income development through revolving loan funds and initiatives like Chicago’s Green Social Housing Ordinance and Seattle’s payroll tax–funded social housing development, the report noted.

“Communities can think about how they incentivize this kind of development, whether it’s lower impact fees or a housing trust fund or the utilization of different inclusionary zoning ordinances,” NeighborWorks America President and CEO Marietta Rodriguez said during the webinar. “It’s going to take all of those tools to really serve and meet the demand that’s in communities today.”

The private sector has an important role to play as well, Rodriguez said. “We would be remiss if we didn’t talk about the importance of leadership at the state and municipal and city level to form strong partnerships with employers, (who) need places for their employees to live, and they need teachers to teach the children of their employees,” she said. “There’s an opportunity to think about what the whole system needs, and bring in employers —large ones— to be part of the solution.”

Despite the current tough times for housing, the webinar participants see glimmers of hope in the years ahead.

“I work with close to 250 local organizations that, despite all of these economic challenges and headwinds, are making miracles happen every day in their communities,” Rodriquez said. “Once you see that kind of work, you can’t unsee it.”