How an Increase in Student Loan Delinquencies Could Affect the Rental Market

Plummeting credit scores could disqualify many renters across the country.

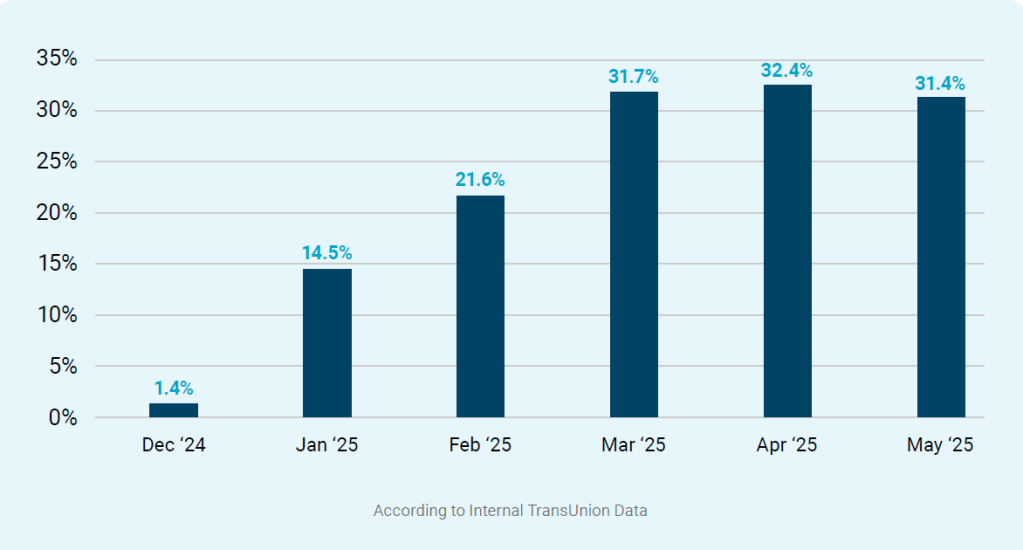

Student loan delinquency rates among renters nationwide have climbed dramatically since payments started again in early 2025, a recent report from TransUnion has found. According to the firm’s Q3 2025 Student Loan Repayment Study, these rates have more than doubled from 14.5 percent in January to 31.4 percent in May, a more than 2,000 percent increase since December of 2024.

With this steep rise in failed payments, a significant number of potential multifamily renters are experiencing dips in their credit scores, falling into lower risk tiers. Consequently, they could be disqualified from leasing, as these scores are often a priority in the screening process.

What does the data say?

According to internal TransUnion Data from the Q3 2025 Student Loan Repayment Study, one in three borrowers is making payments more than 90 days late and one in five stopped paying altogether.

A credit report from Urban Institute shows similar statistics. In its Debt in America interactive map, the data shows that approximately 16 percent of student loan borrowers are at least 60 days behind on repaying their student loans, with a higher concentration of late payments in the South.

READ ALSO: Multifamily Mortgage Debt Outstanding Increased in Q2

Future residents that may have been candidates for multifamily communities earlier this year are now falling below the threshold due to being deemed as higher risk as a result of lower credit scores, according to Maitri Johnson, executive vice president of TransUnion’s tenant and employment screening business.

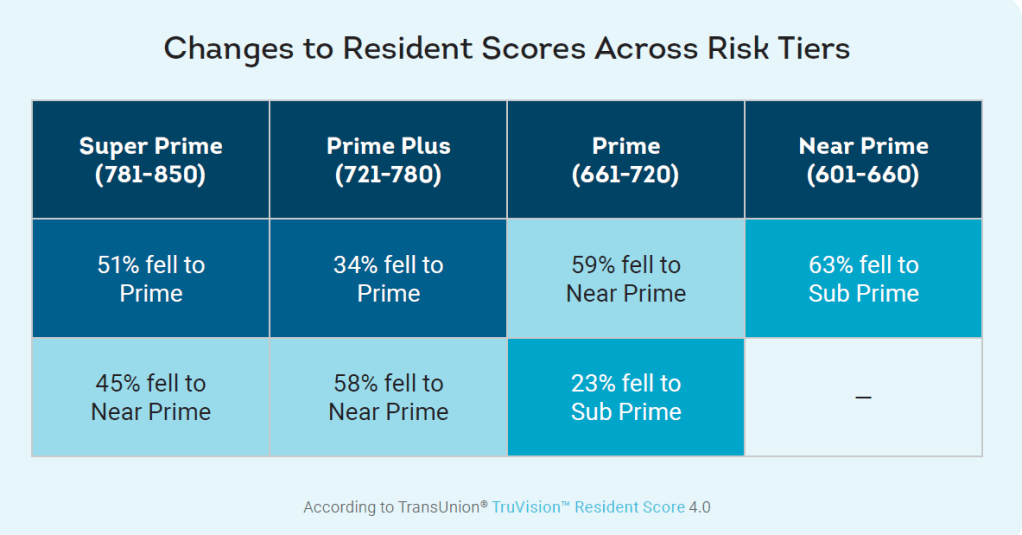

Renters previously in the super prime category—where individuals have credit scores between 781-850—experienced the biggest shift. By the third quarter of 2025, 51 percent fell into the prime category (scores of 661-720) and 45 percent fell to the near prime bracket (601-660), with 2.2 million borrows seeing upwards of a 100-point drop in their score.

“While we knew the results were going to be indicative of some financial stress with some borrowers, the magnitude of the stress was certainly surprising and very concerning,” Johnson told Multi-Housing News, specifically signaling the fall of super prime consumers to near prime.

Lower-risk categories are feeling the effects as well. Renters previously profiled in the prime category saw a 59 percent fall to the near prime group and a 23 percent fall to sub prime, the report shows.

Re-evaluating the criteria

Alongside a shrunken resident pool, other problems that could arise as a result of these skyrocketing delinquencies could take the form of more fraudulent applicants, as well as an increase in evictions, TransUnion explains. In turn, a smaller pool of potential residents could negatively impact vacancy, occupancy and resident retention rates.

“We anticipate and encourage landlords to reevaluate how student loan debt is treated in the approval underwriting process,” Johnson said. “For example, evaluating the balance owed, the age of the student loan and prior payment history on the loan may all be considerations in this re-evaluation, though we encourage property mangers to work with their counsel to determine how best to manage this.”

Johnson’s recommended course of action also includes updating these services and implementing specific multifamily fraud tools. Property managers have been able to streamline the application process with the use of AI to help with resident screening and eliminate manual data entry mistakes.

“When property managers rely on traditional credit scores, they can miss critical details such as eviction history and rental payment behavior,” he said. “That’s why I recommend using a purpose-built rental risk model, so property managers can reduce risk exposure without shrinking their applicant pools. These tools also enable faster and more confident leasing decisions.”