2026 Senior Living Trends: Demand Leads, Capital Reopens

With occupancy on the rise and new supply lagging, the sector enters 2026 on solid footing.

Senior housing is entering 2026 with the wind at its back—a continuation of the momentum the sector has built over the past several years. Demand from older adults continues to rise, even as development pipelines remain thin by historical standards. Operators and capital providers describe a market that now rewards precision over scale and execution over experimentation. Financing is available, though at a premium, and affordability for middle-income seniors remains one of the industry’s most pressing unresolved challenge.

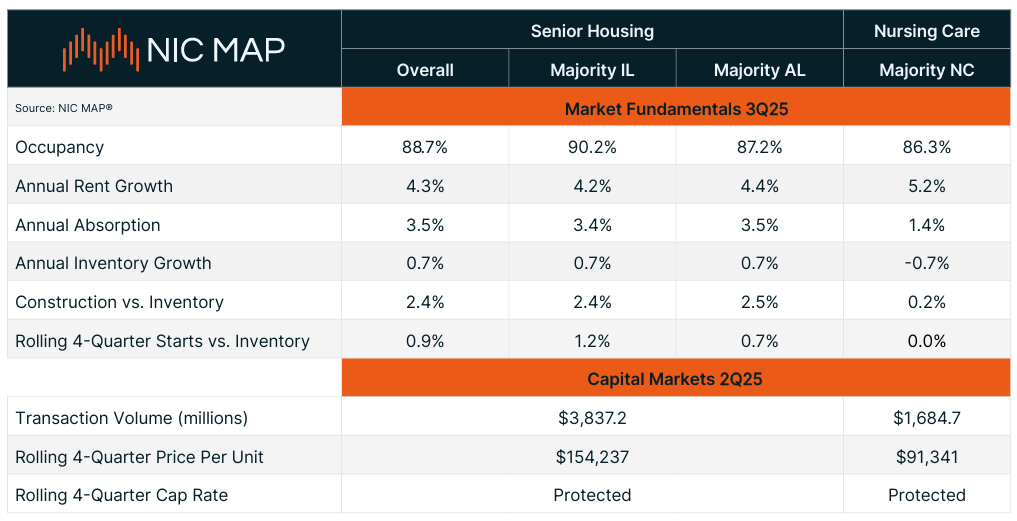

The data helps paint that picture. National senior housing occupancy reached 88.7 percent in the third quarter of 2025, up 0.7 percent quarter-over-quarter and marking the 17th consecutive quarterly increase, according to NIC MAP, partner of the National Investment Center for Seniors Housing & Care. Independent living climbed to 90.2 percent and assisted living to 87.2 percent, while inventory growth hit a record low in 2025.

The combination of rising move-ins and limited new supply points to a tight near-term environment—further evidence of strong demand fundamentals and a development pipeline that continues to lag behind demographic needs.

Brief 2025 recap

The senior housing sector closed 2025 on firmer footing than many anticipated. Leasing velocity and rent growth moved faster than expected, and capital became easier to secure.

“Debt availability improved markedly and investor appetite returned in a big way,” said Mike Gordon, global CIO at Harrison Street Asset Management.

Transaction activity picked up across the board. The JLL Seniors Housing Capital Markets closed multiple sales and financings throughout the year—from single assets to large portfolios. Construction, bridge and permanent financing were all available, with debt “as liquid as it’s been since the pandemic,” according to Senior Managing Director Aaron Rosenzweig. JLL placed multiple loans in 2025 with spreads “at or below about 200 basis points,” he noted. Construction financing has also loosened, typically at 60 to 65 percent loan-to-cost and 250 to 325 basis points over the index, with guarantees that burn down as projects de-risk.

Meanwhile, transaction activity has also strengthened. JLL’s 2025 investor survey reported rolling four-quarter deal volume at its highest level since the second quarter of 2022, with most respondents expecting cap-rate compression over the next 12 months and planning increased allocations to the sector.

But even amid this renewed activity, costs remain stubborn, prompting capital to become more selective and pushing a premium on strong operators and disciplined execution. Developers are also forced to navigate through high costs, which will likely keep inventory growth close to record lows.

Thin pipelines, longer timelines

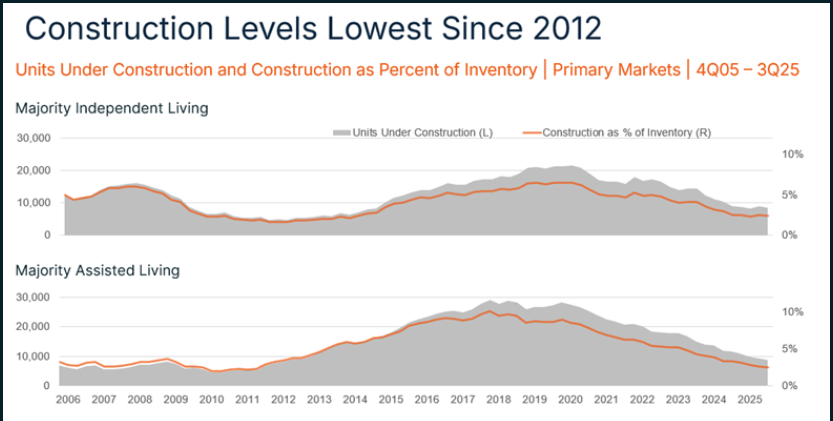

Senior housing supply indicators remain tight. NIC MAP data shows annual inventory growth at just 0.7 percent in the third quarter of 2025.

“Even if construction starts pick up in 2026, it will be a few years until new supply starts to come onto the market in a meaningful way,” said Lisa McCracken, head of research and analytics at NIC.

One reason is timing. McCracken notes that the average construction cycle has now stretched to 29 months, meaning projects that break ground in early 2026 are unlikely to open before 2028. With average cycles approaching two and a half years, stabilized properties stand to benefit from limited near-term competition and tightening market conditions.

Against this backdrop, developers say they are proceeding selectively rather than broadly. “We’re greenlighting new development because the fundamentals and risk profile make sense, focusing on premier senior communities on irreplaceable sites in affluent micro-markets with high barriers to entry and multi-year predevelopment processes,” said Gordon.

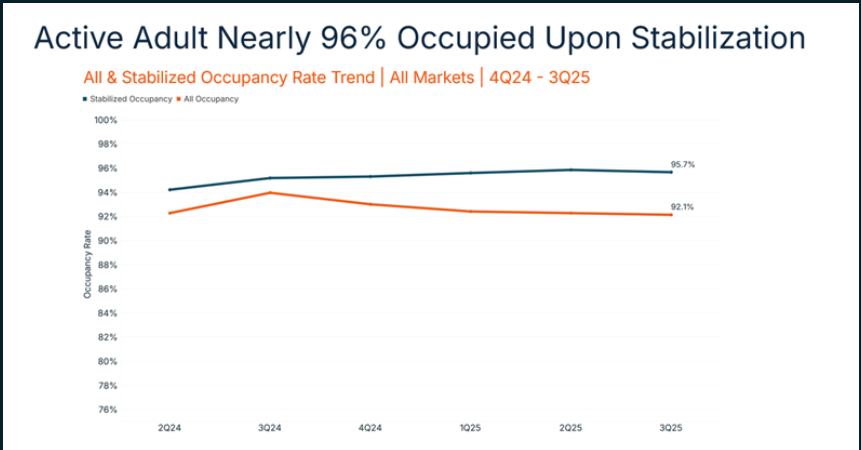

A growing share of that activity is tied to active adult rentals, which McCracken describes as “an additive rather than a substitute” for traditional senior housing, acting as a bridge between conventional multifamily and independent living.

“The resident profile is very different, and the price point is generally well below what is charged for a typical independent living unit, along with a number of other differentiators,” she said.

For now, this segment is still nascent. The national penetration rate was slightly below 1 percent in 2025. Scale is concentrated in a handful of metros, with Dallas alone accounting for nearly 7 percent of the national active adult inventory.

As developers and investors weigh where demand is emerging, capital conditions are evolving, as well. Rosenzweig expects permanent financing to remain prevalent into 2026, with sources ranging from Fannie Mae and Freddie Mac to life companies and banks.

Strategies and risks for 2026: precision, affordability and operator quality

As financing loosens and capital grows more selective, operators and developers are adjusting their playbooks for the year ahead. Strategy—in everything from pricing to product design—is becoming as important as demand fundamentals.

Nationwide, Harrison Street expects senior housing fundamentals to remain strong in 2026, with rental rate growth trending between 3 and 6 percent. Active adult communities are projected to fall at the lower end of that range, while higher-acuity units in supply-constrained markets could push toward the upper end. Performance, according to Gordon, will hinge on occupancy, lease-up velocity, retention, input costs and new supply—operational levers that continue to define today’s senior living trends. The objective, he added, is to sustain “consistent, low-to-middle single-digit top-line growth through operating excellence.”

Brightview South River is a senior living community offering independent living, assisted living and memory care options in in Edgewater, Md., owned by Harrison Street and managed by Brightview Senior Living. Image courtesy of Harrison Street

The Springs at Waterfront is a 12-story senior housing property in Vancouver, Wash., part of the 32-acre Vancouver Waterfront master plan along the Columbia River. Image by Moris Moreno, via Harrison Street

Belmont Village San Ramon is a senior living community that opened in early 2025, encompassing 177 units for independent living, assisted living and memory care. Amenities include two restaurants, a library with fireplace, creative arts studio and dog park. Image courtesy of Harrison Street

Achieving that growth, however, depends on navigating one of the sector’s most persistent challenges: affordability, which is closely tied to the financing landscape operators are navigating. Albert Milo, president of Related Urban Development Group, noted that long-term interest rates continue to influence how permanent financing pencils out. He emphasized that his team aims to deliver units that remain affordable for residents and appropriately priced for their markets. In 2026, Related is focusing on mixed-income independent living in Miami-Dade County, targeting the missing middle—residents earning roughly 80 to 120 percent of the area median income—alongside subsidized housing through RAD/Section 8 and income-averaging LIHTC.

“During the last several years, the market has seen annual rent growth of more than 9 percent,” Milo said. “However, we underwrite our projects conservatively and only use a 3 percent growth factor.”

Product design is becoming another critical strategic risk. The sector’s aging inventory poses a challenge as operators prepare for the influx of Baby Boomer residents.

“The average age of senior housing properties today is 24 years, while the typical move-in age is around 80. In that sense, the average property was effectively designed for today’s 104-year-old,” said McCracken, urging operators to modernize senior independent living facilities to meet evolving expectations.

“The Baby Boomers have a very different vision of what is acceptable senior housing and what they are willing to pay for,” she added. “If we do not adapt the product to their changing preferences, we will miss the opportunity in front of us.”

Product adaptation is only one piece of the puzzle. Paired with rising demand and tight supply, it sets the tone for the sector’s outlook heading into 2026.

A constructive 2026 if discipline holds

The foundation for next year is solid: Occupancy is rising and capital is available for well-underwritten projects. The near-term balance favors stabilized assets, but the winners will be those that execute with precision, aligning product and pricing with local incomes, investing in operational excellence and targeting markets where incremental supply is limited.

For developers and operators, the path forward is practicality over scale. The next phase pairs micro-market site selection with authentic affordability and careful pacing of starts. Serving the missing middle can broaden access and demand without overreaching on rents. As McCracken noted, Baby Boomers’ expectations are reshaping what “acceptable” senior housing looks like and operators who adjust early stand to benefit most.

For investors and lenders, a selective expansion is warranted. Debt is available across construction, bridge and permanent loans, though structures continue to reward strong sponsors and credible underwriting. If costs stay contained and lease-up momentum holds, transaction activity should continue to firm alongside confidence.

Absent a renewed cost surge or a turn in financing conditions, the base case for 2026 is constructive: mid–single-digit revenue growth for well-run platforms, steadier liquidity and a sector poised for expansion.