NAHB Special Report: Why Apartment Vacancies Will Rise in 2026

Economists at the International Builders' Show predict that the market will cool following a pandemic-era boom.

With the Covid pandemic in the rearview mirror, housing economists found a silver lining for the multifamily industry, one that appears to be reaching its expiration date. During the shutdown years, the sector experienced a period of growth as residents fled the top urban centers looking for areas that offered more space to spread out with pandemic restrictions.

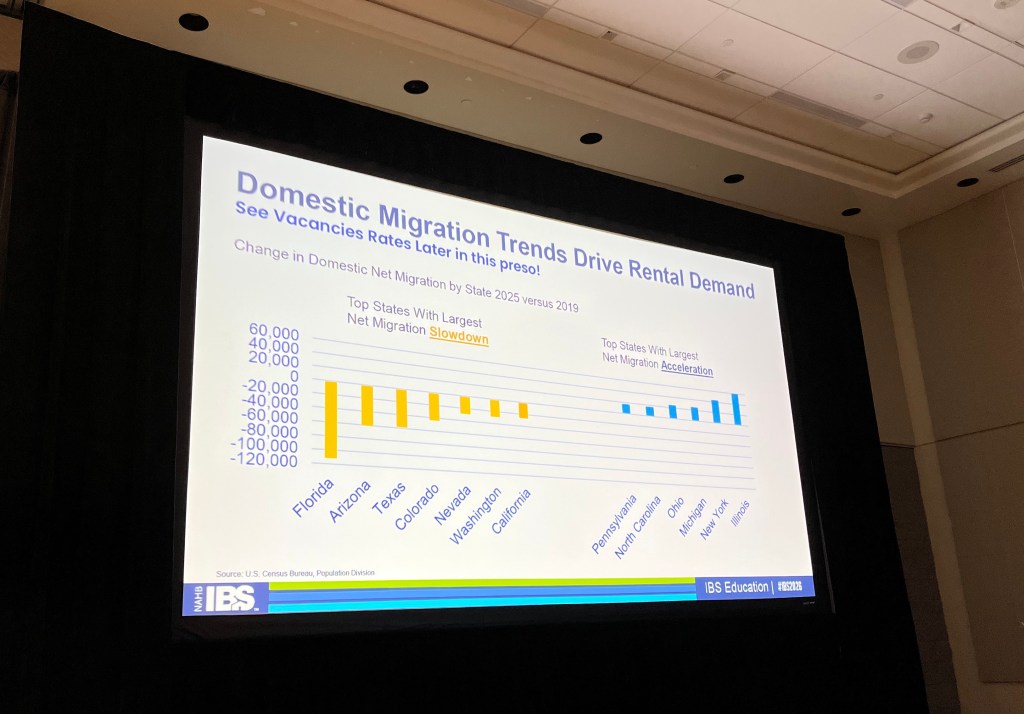

Now, the pandemic era boom is being challenged by a reduction in immigration, domestic migration trends from state to state, a softer labor market and rising vacancies. Economists speaking at the National Association of Home Builders International Builders’ Show in Orlando predict a slowing rental market in the months ahead. Multifamily is moving toward a more constrained development environment according to Molly Boesel, senior principal economist at Cotality, and Danushka Nanayakkara-Skillington, NAHB’s assistant vice president for forecasting and analysis.

The factors at play

Last year, multifamily property sales rebounded following a three-year slump, increasing 15 percent as new supply came on the market. This turnaround was broad, with 80 percent of metros seeing an increase in sales compared to only 20 percent of metros in 2024.

“The regional sales shifts were notable, as we saw particularly strong growth in Midwest and California metros,” said Boesel. “However, some Sun Belt markets that surged in 2024 posted declines in 2025.”

With the U.S. still experiencing home affordability challenges, many residents are staying in the rental market. High supply helped push multifamily rents down one percent year-over-year in 2025 while single-family rent growth slowed. Multifamily rents remained strong in supply-constrained metros such as Chicago, New York and Philadelphia. Rents weakened in Phoenix, Tampa and Las Vegas where, inventory is not an issue. Investor sentiment appears strong.

READ ALSO: Will Multifamily Investment and Development Volumes Grow in 2026?

“The national multifamily vacancy rate ran up to a record high of 7.3 percent in December,” said Boesel. “We’re past the peak of a multifamily construction surge, but a healthy supply of new units is still hitting the market and colliding with sluggish demand, causing vacancies to continue trending up.”

Boesel added that multifamily property values declined four percent in 2025 compared to 2024, and that they are roughly 28 percent below the 2022 high. However, values are now eight percent above 2019 values. And the lending side of the market is still experiencing a rise in delinquency rates, but that remains well below office building delinquencies. “Delinquency rates are rising due to higher interest rates, changes in property market fundamentals and uncertainty about property valuation,” said Boesel.

Apartment starts decline

On the construction front, multifamily starts peaked in 2022 at 547,000 units. Then starts declined sharply to 355,000 units in 2024. The year-end government data for last year has not yet been released, but NAHB’s Nanayakkara-Skillington expects a modest rebound for 2025, with starts forecasted to have increased by 16 percent to 413,000 units. Looking ahead, Nanayakkara-Skillington anticipates multifamily starts to fall five percent in 2026 to an annual pace of 392,000 units and decline an additional six percent in 2027 to 367,000 apartments. This would be a leveling off to near pre-pandemic levels.

“The multifamily market has slowed due to tighter financing and elevated construction costs, and is moving towards a more constrained development environment,” said Nanayakkara-Skillington. “However, despite the pullback in starts, multifamily completions reached a 38-year high in 2024, with 608,000 units initiated during the boom years were delivered to market.”

Interestingly, the composition of multifamily production has shifted toward larger properties, as 50+ unit buildings accounted for 54 percent of completions in 2024, the highest share in decades. Meanwhile, the missing middle construction sector—which includes development of townhouses, duplexes and other small multifamily properties—remains limited.

READ ALSO: Live Local and ED-1: How Does Policy Drive Development?

According to Nanayakkara-Skillington, the multifamily segment of the missing middle (apartments in two- to four-unit properties) has generally disappointed since the Great Recession, totaling just 4,000 starts in the third quarter of 2025, representing only three percent of multifamily production. Zoning issues continue to be challenging in so many markets.

“However, in addition to tight lending conditions and high construction costs, the local regulatory environment continues to be a major headwind to faster growth,” said Nanayakkara-Skillington. NAHB’s most recent Multifamily Occupancy Index measuring apartment owner sentiment provides another positive indicator. Respondents expressed a high reading of 74 using a scale of 0 to 100.

And don’t forget the potential influx of young adults—including the ones who have been living at home with parents—as they enter the housing market. This new population of renters is yet another reason for the apartment industry to see the glass half full as 2026 gets under way.