Multifamily Cap Rates Stabilize as Investor Sentiment Strengthens

A new survey from CBRE finds strong indicators for multifamily investors on pricing and performance.

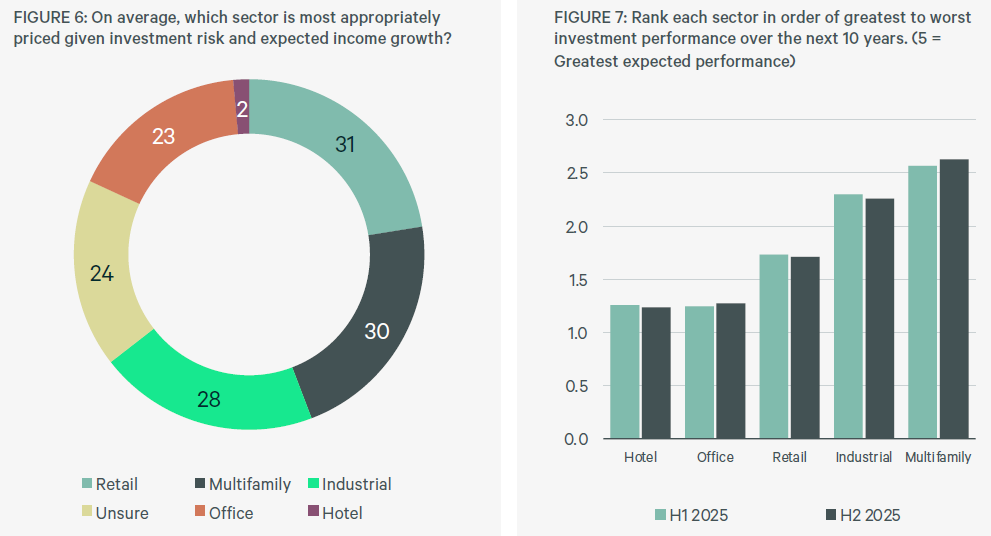

Multifamily will outperform other commercial real estate sectors over the next 10 years, according to a new cap rate survey of professionals from CBRE capital markets and other valuation experts.

Respondents to CBRE’s “U.S. Cap Rate Survey H2 2025” also felt multifamily asset pricing was the most appropriate given the risks and income growth potential, placing just slightly behind retail in their choices. The survey is based on approximately 3,600 cap rate estimates from more than 200 CBRE capital markets and valuation professionals in more than 50 U.S. markets provided in early December.

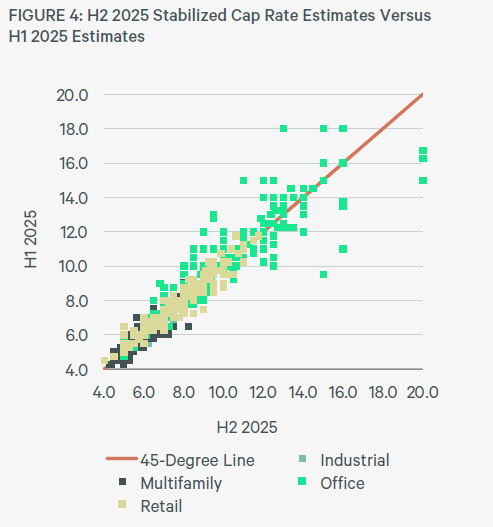

Multifamily investors should find other good news in the new survey that shows that cap rates stabilized across major commercial real estate property types in the second half of 2025. The report states that this signals that most pricing resets have already occurred, the markets are nearing equilibrium and CRE appears to have entered a new cycle.

Most respondents also believe yields have reached their cyclical high. However, those surveyed differed on when cap rates may begin to compress.

Responses to the survey come as volatility is easing and investor sentiment is strengthening despite continued concerns over the U.S. economy, trade policy and future interest rates.

Tommy Lee, co-head of Capital Markets, U.S. & Canada, for CBRE, said in prepared remarks the market is transitioning from volatility toward stability and the outlook is increasingly positive, particularly for pricing of multifamily assets. Lee said most investors now expect cap rates to hold steady or decline. Combined with clearer risk pricing and improved capital availability, the stabilization of cap rates is paving the way for renewed investment activity, Lee stated.

READ ALSO: MBA-CREF Special Report: Busy Year Ahead for Multifamily Lenders

In fact, the report shows that transaction activity is rebounding, with the CRE market seeing transaction volume increasing by about 19 percent last year. And current trends are indicating a more active investment landscape in 2026, according to CBRE. Several price indices are no longer falling and debt is becoming more available with higher loan-to-value ratios and more lenders entering the market, both banks and non-banks. Borrowers are also finding more predicable underwriting conditions.

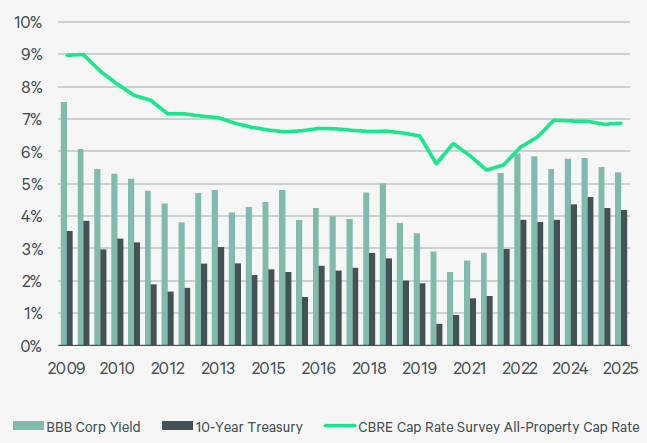

The report noted that 10-year Treasury yields peaked near 4.8 percent in mid-January 2025 and again around 4.5 percent in July, before easing to a 3.9 to 4.2 percent range by year-end. CBRE stated factors included lower inflation and an expectation of continued economic growth.

A closer look at industry expectations

Respondents were much more optimistic about expected changes in cap rates during the last six months of 2025, with nearly 50 percent of participants saying they expect retail, industrial and hotel cap rates to decline. By comparison, in the survey from the first half of 2025, nearly one-quarter of respondents believed cap rates were past their peak and would decrease over the second half of 2025.

In the current survey, the most common response across all categories was “no change.” For the multifamily segments—infill and suburban—there’s a significant increase in the number of respondents who are expecting decreases over the next six months compared to the respondents in the survey from the first half of 2025.

Cap rates around the U.S.

The survey takes a closer look at markets in different regions of the country and cap rates for Class A stabilized and Class A value-add properties. The report shows that major coastal markets, in many cases, were stable or compressed slightly between the first half and second half of 2025. For example, New York City’s Class A stabilized assets went from 4.75 percent to 5.25 percent in the first half to 4.5 percent to 5 percent in the second part of 2025. Class A value-add properties compressed from 5.5 percent to 6 percent to 5 percent to 5.5 percent.

Meanwhile, in Washington, D.C., both infill Class A stabilized and value-add assets remained steady at 4.75 percent to 5.5 percent. Washington, D.C.’s suburban markets, however moved from 4.5 percent to 5.25 percent to 4.75 percent to 5.5 percent for Class A assets and from 4.5 percent to 5.25 percent to 5.75 percent for value-add properties in the latter half.

In the South, Atlanta’s infill Class A stabilized and value-add remained steady at 4.5 percent to 5 percent for the full year. Suburban Atlanta assets, both Class A stabilized and value-add, had the same cap rates. “We’re seeing a real divergence between perception and performance, said Kelli Carhart, head of multifamily capital markets at CBRE. “Even with some NOI pressure, the discount to replacement cost is now so compelling that cap rates are compressing and valuations remain resilient.”

Chicago’s infill and value-add assets saw some decreases between both halves of the year, with the Class A assets going from 5.25 percent to 5.75 percent to 5.25 percent to 5.5 percent and the value-add properties moving from 5.25 percent to 6 percent to 5.25 percent to 5.75 percent. Chicago’s suburban markets saw Class A cap rates move from 5.25 percent to 5.75 percent to 5 percent to 5.5 percent and value-add properties move from 5.25 percent to 5.75 percent to 5.25 percent to 5.5 percent.

On the West Coast, San Francisco Class A infill stabilized assets held relatively steady from 4.5 percent to 5.5 percent in H1 to 4.5 percent to 5 percent in the second half while value-add assets moved from 5 percent to 6 percent to 4.75 percent to 5.5 percent.