Multifamily Fundamentals Stabilize as Market Demand Diverges

Markets supported by strong domestic migration are better positioned to maintain stability.

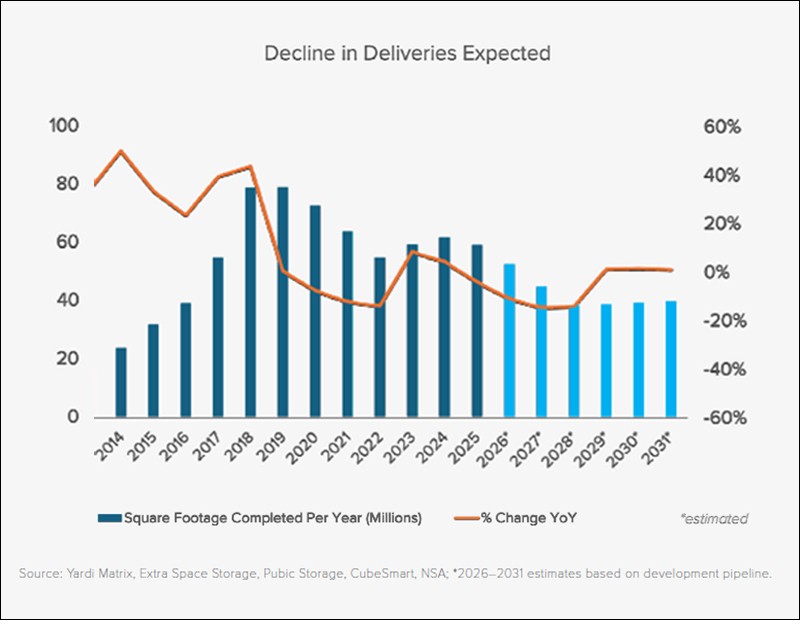

U.S. multifamily fundamentals are firming, as the market moved past the peak of the recent supply surge. The national vacancy rate rose to 6.8 percent in the first quarter, up 30 basis points from a year earlier. While the vacancy rate remains elevated, the relatively modest increase indicates that upward momentum has plateaued as absorption improves.

Rent performance tells a similar story. Asking and effective rents increased 0.6 percent quarter-over-quarter, lifting average effective rents to $1,825 per unit. Although growth remains subdued following late‑2025 softening, current trends support stabilization rather than a renewed acceleration in rents.

While national conditions stabilized, performance remains uneven across the country. Markets that experienced the most aggressive construction activities during the recent development cycle, which peaked in late 2024 to early 2025, now face greater near-term vacancy and rent pressure as newly delivered properties enter the lease-up phase.

Dallas, Phoenix, Charlotte and San Antonio highlight this pattern. Vacancy rates in these markets rose further in early 2026, exceeding the national increase, with year-over-year gains generally ranging from approximately 10 to 110 basis points, while rent growth lagged the national average.

Supply-constrained and high-demand markets show greater resilience. New York ranked among the tightest multifamily markets in the first quarter, while rent growth in coastal, technology-focused markets such as San Francisco and San Jose ranked among the strongest across the 79 primary markets tracked by Moody’s Analytics. These outcomes show that while national conditions are stabilizing, demand differences increasingly shape market-level performance.

Migration and household formation trends

Over the next eight quarters, multifamily demand faces the risk of slower household formation, which could reduce the market’s ability to absorb supply quickly. Census data show that U.S. population growth slowed sharply in 2025, declining to 1.8 million from 3.2 million in 2024. A decline in net international migration drove the slowdown, while natural change, measured as births minus deaths, held roughly flat.

New arrivals are more likely to form renter households, so changes in immigration tend to affect multifamily demand the most. The effect, however, often comes with a delay, as the headship rate measured by one over the number of people in the same household is low for new immigrants.

Reliance on immigration varies across states. Net international migration accounted for about 81 percent of population growth in Washington state from 2021 to 2025 and nearly all of the growth in both Massachusetts and New Jersey during the same period. On the contrary, Florida, Texas, and the Carolinas rely more heavily on domestic migration and natural population increase, making them less sensitive to slower international inflows.

Both charts focus on a selected group of states that experienced net population gains from 2021 to 2025, allowing for clearer comparison of how differences in immigration reliance shape demand trends. Changes in multifamily occupied stock provide an early illustration of how exposure to immigration contributes to uneven market outcomes. As illustrated in Chart 2, the occupied stock index rose strongly across all covered states from 2023 to 2025, before growth moderated from 2025 to 2026.

Immigration decreases across the country

Utah and South Carolina, which relied less on immigration as a source of population growth over 2021 to 2025, posted stronger occupied stock gains in the most recent period. Washington state, which relied more heavily on immigration as a source of population growth, posted weaker occupied stock gains from 2025 to 2026 than Utah and South Carolina.

Multifamily demand has also softened in Washington D.C., though population trends there suggest that weakening labor market conditions, including slower hiring momentum, played a larger role than immigration exposure alone.

Markets with greater reliance on international inflows, especially across the Northeast, Midwest and West Coast, face greater downside risk when supply remains elevated. In these areas, even a modest cooling in renter demand could slow rent growth and place renewed pressure on vacancy rates. Markets supported by strong domestic migration, limited construction, or both are better positioned to maintain stability.

—Posted on April 24, 2025