Institutional Investors Stay Focused on Self Storage Despite Challenges

Even though occupancy is dropping and deliveries are declining, the sector is still attracting significant investor interest.

Despite challenges including a weak housing market, lower occupancy and decreasing deliveries, the self storage industry remains a top-performing asset class that continues to attract institutional investors, according to a DXD Capital report, the latest installment of its Self Storage Quarterly Download series.

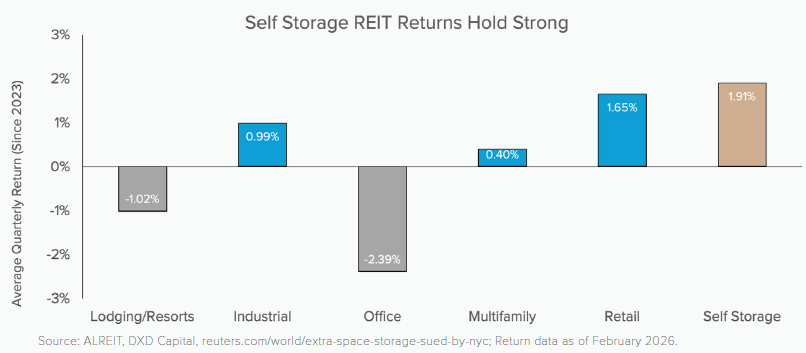

Of the commercial real estate sectors tracked by DXD Capital, the asset class has posted an average quarterly return of 1.91 percent since 2023. By comparison, the first-quarter 2026 DXD Capital trends report notes office and lodging have remained in negative territory at -2.39 percent and -1.02 percent, respectively.

What the report found

The self storage sector is facing a reset, with occupancy dropping below the pandemic-era gains, which reached a high of 96.4 percent in the third quarter of 2021. The first quarter of 2026 marked a new cyclical low, with weighted REIT occupancy dipping below the 92 percent floor the industry had seen as a long-term average to 91.5 percent. This figure falls below the pre-pandemic baseline of 92.8 percent recorded in Q4 2019. DXD Capital points to the residential housing gridlock, noting that without meaningful home transaction volume, the relocation-driven demand is missing.

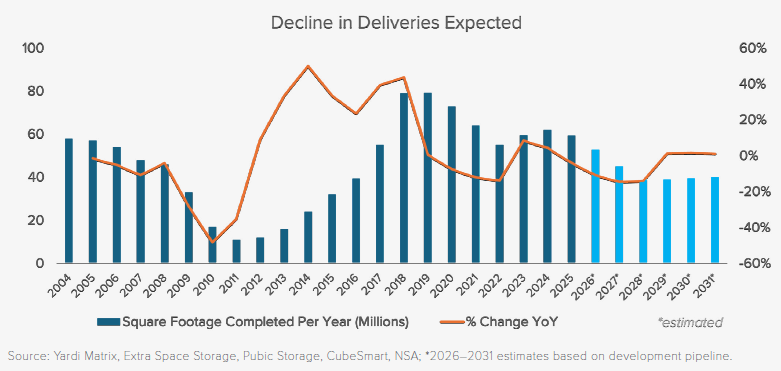

The report states the market appears to be trending toward a new operational baseline that includes recalibrating strategies for a consistent interest rate environment rather than waiting for a return to historical peaks. This change in strategy comes as the supply pipeline is entering a sustained contraction, expected to last at least through 2028.

Deliveries are expected to drop from 59 million net rentable square feet to 51 million net rentable square feet this year, reaching approximately 38 million by 2028. Those are levels not seen since 2016 and nearly half the 79.2 million NRSF delivered in 2019.

But that lower supply should help stabilize occupancy and hold it near current levels through the end of 2026, according to Drew Dolan, principal & fund manager at DXD Capital, a New Mexico-based private equity firm that develops and invests in self storage. Founded in 2020, the firm has a portfolio of more than 41 properties.

In April, DXD Capital opened a 94,975 square-foot Class A self storage facility in Georgetown, Texas, that will be operated by Extra Space. It was the first completed facility of three that DXD broke ground on last year in partnership with Kuwait Financial Centre’s Mar-Gulf Management Inc., and MDI Capital LLC.

READ ALSO: Why Nuveen Sees a Self Storage Investment Window

“The primary stabilizing force is supply. New self storage construction has fallen sharply, which limits the inventory pressure that typically drives occupancy lower,” Dolan told Multi-Housing News. “With demand remaining steady against a constrained pipeline, the conditions for meaningful occupancy erosion simply aren’t there.”

When asked if he expects increases in rental rates due to the decrease in deliveries, Dolan said that self storage “is fundamentally a local business and performance is determined within a three-mile radius, not at the national level.”

He said there will always be markets that outperform and markets that don’t due to local supply-demand balance. But he noted that macro conditions also play a role.

“With deliveries projected to remain constrained through 2028, rental rates and occupancy should grind higher across most markets through the end of the decade. For existing investors, that points to a peak realization window in the 2029 to 2030 timeframe, and the window to position ahead of it is now,” Dolan said.

Institutional investments and mega-mergers

Dolan said institutional capital is actively rotating back into the self storage market, pointing to Public Storage’s $10.5 billion planned acquisition of National Storage Affiliates announced in March.

He said that acquisition “signals the largest operators see consolidation as the path to scale.”

“On the private side, Heitman secured $475 million across its Core+ fund and co-investments, while Blue Vista Capital Management’s $600 million strategic partnership with UBS and Extra Space Storage reflects a growing appetite from sophisticated allocators seeking exposure through structured, operator-aligned vehicles,” Dolan noted.

READ ALSO: What’s Driving All the REIT Mergers?

The recent surge in mega-mergers and strategic joint ventures indicates self storage is now a core institutional staple, according to the report. It is also showing signs of institutional consolidation, dominated by operators who leverage sophisticated data analytics to optimize performance.

DXD Capital calls the pending Public Storage acquisition of NSA, expected to close in the third quarter, as “the critical institutional event of 2026” and signal high institutional conviction in the sector’s long-term durability. Under the deal, Public Storage will add more than 1,000 properties and manage roughly 327 to 328 million NRSF. It will also grow its share of total REIT-managed net rentable square footage from 35 percent to approximately 44 percent. That will make it nearly even with Extra Space Storage, which is currently the world’s largest self storage operator.