Will Lower Rates Bring Banks Back?

Multifamily borrowers could see traditional avenues reopen.

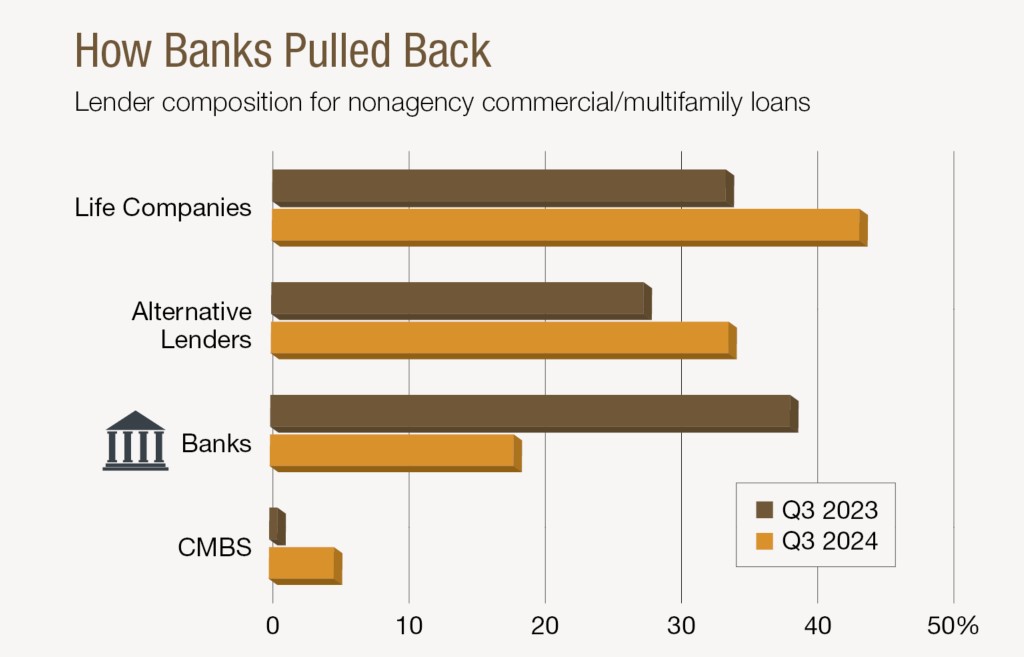

Multifamily direct lending by banks has dropped significantly in the last 18 to 24 months. One real estate leader described it as “almost nonexistent,” while another likened it to a freeze that hasn’t thawed.

Banks continue to be in a “highly restrictive lending mode” that has resulted in much lower loan-to-value ratios, increased selectivity of projects they will back and, in many cases, the requirement to make substantial deposits to the bank, noted Joe Iacono, CEO of Crescit Capital Strategies.

“They’ve been much more cautious about who they’re working with and with much more stringent underwriting,” said Iacono.

But there are signs of improvement.

“We’re seeing an increase in construction loans over the last 90 days,” reported Andy Scott, senior managing director with JLL Capital Markets. “The larger banks are definitely beginning to move back into the market.”

Mortgage borrowing started picking up in the third quarter of last year as the Federal Reserve began cutting interest rates, noted Jamie Woodwell, vice president & head of commercial real estate research at the Mortgage Bankers Association.

Multifamily originations increased 56 percent year-over-year in the third quarter, according to the MBA’s report on outstanding debt. Agency and GSE portfolios and mortgage-backed securities hold the largest share of outstanding debt at $1.03 trillion (49 percent), followed by banks and thrifts with $630 billion (30 percent); life insurance companies with $244 billion (12 percent); state and local government with $99 billion (5 percent) and CMBS, CDOs and other ABS issuances with $68 billion (3 percent). In the third quarter, banks and thrifts increased their holdings by the slimmest margin—up $4.7 billion, or 0.8 percent.

“Capital in the debt space is as liquid from every provider as I’ve seen in a long time,” said Nate Sittema, vice chairman of CBRE’s debt and structured finance group. “That includes the money center or regional banks, in what has felt like a tectonic shift.”

Matt Scarola, head of multifamily investments at Integra Investments, said his firm is considering financing a Miami market-rate project with a bank loan due to lower interest rates. Integra has historically had good banking relationships, particularly for its new development projects, but it had become tougher to negotiate over the last 18 to 24 months, and the banks couldn’t compete on pricing, added Scarola.

Active regional banks

Not all banks were on the sidelines.

Centennial Bank has “had a pretty robust year” with loans for new multifamily and other residential projects, including luxury condos, according to J.C. de Ona, the firm’s Southeast Florida division president. Centennial is a national company, but most of its activity is in Florida and Texas.

“We’ve never had issues where we had to stop lending or pull back,” indicated de Ona, noting that Centennial has always had conservative underwriting. “We’ve been consistent with our underwriting and how we see things. We’ve always sensitized our projects just to make sure that they could perform in a higher-interest-rate environment.”

De Ona added that higher rates combined with rising construction costs made it difficult for some projects to pencil, causing several planned rental properties to become for-sale condominium projects.

Asked about loan-to-cost ratios, he said back in peak times they were at 70 percent LTC on multifamily properties. But those numbers fluctuate, depending on land costs and cash flow, and can range from 50 to 65 percent LTC.

The lower LTC and loan-to-value bids from banks at 50 percent leverage means the borrower has to come up with more money, according to Rob Gilman, head of Anchin’s real estate group. Now that rates are coming down, some are considering variable-rate loans again.

Regional banks were being selective and avoiding riskier deals, he said, because of concerns over distressed assets, rising maturities and decreasing property values.

“If a larger bank had to write off a $50 million loan, you know their liquidity wouldn’t be as affected as much as for a regional, where the $50 million makes a big difference,” indicated Gilman.

Using lending capacity

Matt Jones, chief investment officer at Harbor Group International, a real estate investment firm that owns 57,000 apartments and is also a bridge lender, said banks are focused on addressing asset management issues within their own books rather than direct lending.

Investment banks have balance sheet lending capacity but are using it in other capital market financing strategies.

“Everybody that we know who has a CMBS lending platform is very actively quoting CMBS loans,” Jones said, noting there is extreme demand for this product, particularly in the single-asset, single-borrower market.

HGI buys bonds that have multifamily or office properties as collateral in a business line known as securities repo.

“I’ll buy the Triple A (bonds) and I’ll put 50 percent leverage on the bond,” shared Jones. “That leverage comes from the banks that have this securities repo business.”

Many banks have been active in note-on-note or warehouse financing as an alternative to direct lending. “By doing that, the banks get a better capital treatment and so the return on their capital is much better, and they end up in the 50 or 55 percent loan-to-value position but with better capital treatment versus if they had written the loan directly,” said Iacono.

Funding sub-lines for debt funds and bridge lenders gives larger banks access to real estate without the oversight of a direct lending deal, Sittema noted.

Regulatory impact

Part of the loan volume slowdown can be attributed to concerns over regulations regarding capital reserve requirements as well as rollover of existing loans. But as the year progressed, regulatory pressure softened while the banks boosted their cash reserves and began to put credit out.

Having some capital requirements is a good thing, de Ona suggested. “I think there were banks that maybe got a little too aggressive, and you need to be careful about that, too.”

Iacono noted that larger banks are in “pretty good shape capital-wise.”

“Now they may have regulators looking at the balance sheets and worried about the CRE exposure as well, but I think it is a tale of two cities frankly between the larger banks vs. the local and regional banks,” he stated.

Some industry officials are looking to the new federal administration for regulatory relief. President Donald Trump is a developer who understands financing, de Ona said. Easing regulations could mean savings so banks could have more lending capacity.