Multifamily Investors Returning as Values Stabilize

With construction tapering, confidence is making a comeback.

Just as interest rates spiked more than three years ago, multifamily developers unleashed a torrent of new construction, primarily across the Sun Belt. That’s when investors who had fueled higher values in the sector abruptly exited the market. Softening rent growth or rent declines amid rising vacancy in the most overbuilt cities kept most of them on the sidelines.

Since then, multifamily values either have hit bottom or are just a few inches away in overbuilt markets. Strong renter demand is reducing the supply glut as construction starts have declined more than 47 percent over the 12 months ending in September, according to Avison Young.

Meanwhile, monthly home mortgage payments have stayed some $825 higher than rents for the past couple of years, and developing properties is more difficult given the higher cost of capital and inflation, according to William Dunkel, a market intelligence analyst at Avison Young. Combined, these elements are creating a compelling investment thesis, especially in markets enjoying population and job growth, including Dallas, Phoenix and Austin, Texas.

“A slowdown in construction in some of these growing markets means there won’t be a lot of new buildings competing for residents,” said Dunkel. “And with occupancy going up, net operating income will go up and more sales will pencil out.”

Just as interest rates spiked more than three years ago, multifamily developers unleashed a torrent of new construction, primarily across the Sun Belt. That’s when investors who had fueled higher values in the sector abruptly exited the market. Softening rent growth or rent declines amid rising vacancy in the most overbuilt cities kept most of them on the sidelines.

Since then, multifamily values have either hit bottom or are just a few inches away in overbuilt markets. Strong renter demand is reducing the supply glut as construction starts have declined more than 47 percent over the 12 months ending in September, according to Avison Young.

Source: Yardi Matrix

Moving off the sidelines

A correction of around 15 to 20 percent since multifamily values peaked in early 2022, along with decelerating construction, is beckoning investors who can buy apartment assets below replacement cost, noted Hessam Nadji, president & CEO of Marcus & Millichap.

At the same time, owners who have been waiting for dramatically lower interest rates before selling are beginning to capitulate, he added. While Wall Street prognosticators expect the Federal Reserve to cut the federal funds target rate one more time this year, after its October cut of 25 basis points, the days of 3 percent interest rates prevalent a few years ago have permanently given way to a rate environment of about double that.

Apartment sales totaled $111.2 billion in the first three quarters of 2025, a year-over-year increase of 9 percent, according to MSCI Real Assets. The average price was down .08 percent in the third quarter from a year earlier, although capitalization rates remained flat at 5.7 percent, the company reported.

There is more inventory because operators believe a large interest rate cut is unlikely, Nadji pointed out. “We saw the market beginning to move forward about a year ago, and it’s gaining momentum as we speak. New capital is coming in.”

Market timing

One of those new sources, Stockdale Capital Partners, is delving into the multifamily sector after years of focusing on hotels, offices, retail properties and medical offices. In early October, the firm paid cash for its first multifamily asset, Amelia at Farmer’s Market, a six-year-old, 297-unit luxury residential building in downtown Dallas.

The company focuses on employment-driven “micro locations” that have been shielded from a run-up in supply or are positioned for healthy rent increases amid declining supply beginning in 12 to 18 months, according to Sam Palmer, a managing director with Stockdale.

For example, in late October Stockdale expected to close on a property in the North Scottsdale suburb of Phoenix, a metro that institutional investors have avoided because of concession wars. But, Palmer pointed out, those battles are occurring in overbuilt communities on the west side of the Phoenix area, while in the more insulated North Scottsdale submarket, concessions are waning.

“In 2026, some markets have the potential to see a pop in valuations and that’s why we think the time to buy in Dallas and Scottsdale, Ariz., is now, and next year it might be Nashville and Austin, Texas,” he noted. “It’s like a wheel that’s turning—certain markets are finally absorbing supply and reaching equilibrium.”

It’s like a wheel that’s turning—certain markets are finally absorbing supply and reaching equilibrium.

—Sam Palmer, Managing Director, Stockdale Capital Partners

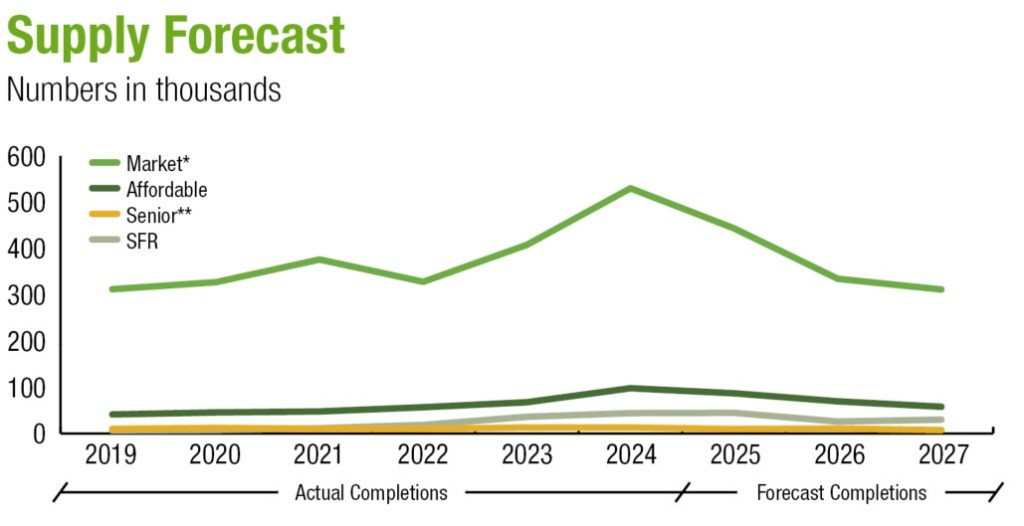

Palmer and others think that multifamily values will grow more materially across a broader range of markets beginning in 2027. The exact timing depends on how much new supply developers continue to deliver in particular markets before construction fully winds down. Data provider Yardi Matrix recently projected that market-rate apartment completions nationwide will slide to roughly 311,000 units in 2027 after peaking at nearly 530,000 units in 2024.

Investors flush with cash are eyeing the dynamics, trying to figure out when to strike, according to Rob Martinson, president of Garrett Cos., which builds and manages projects primarily in the Sun Belt and Midwest. Some who have come off the sidelines are willing to accept a temporary shortfall in cash flow to lock in a deal.

“Investors who jump into the market now know that the long-term metrics are still extremely favorable,” shared Martinson. “Natural supply and demand at a minimum are going to stabilize, and we should move back to pretty consistent rent growth.”

Banking on growth

Given the prospect of better values over the next one to three years, however, Garrett is holding on to properties longer. A few years ago, the developer opportunistically sold assets upon stabilization to take advantage of unbridled investor demand fueled by near-zero benchmark bond yields at the height of the pandemic.

“We’re at an inflection point where the potential increase in profits in 12 to 24 months is going to be accretive versus harvesting profits now and redeploying the capital,” he observed.

The economy will also play a key role in how fast and how far multifamily values will rise in a more normalized interest rate environment, but some key indicators are sending mixed signals. The Bureau of Labor Statistics, for example, recently reported that it had overstated hiring over the 12 months ending in March by 911,000 jobs. Still, in late October, the Federal Reserve Bank of Atlanta estimated that third-quarter gross domestic product grew at an annual rate of 3.9 percent.

“If we continue to see this level of economic growth, I think multifamily pricing is unlikely to move backwards,” said Sam Tenenbaum, head of multifamily insights for Cushman & Wakefield. “If we were to see a recession, there would be more downward pressure on prices, but that’s not our base case. The multifamily market is on pace for the third-best year for renter demand going back to at least 2000.”