Let’s Build the Right Kind of Housing

The American dream of homeownership should not be discarded but adjusted, observes developer Edd Hamzanlui.

We need to build housing urgently, and that includes all types: rentals, single-family homes, affordable and market-rate. The need is monumental, and the time to act is now. However, in our rush to address the housing crisis, we’re overlooking a crucial question: Are we building the right kind of homes for the future?

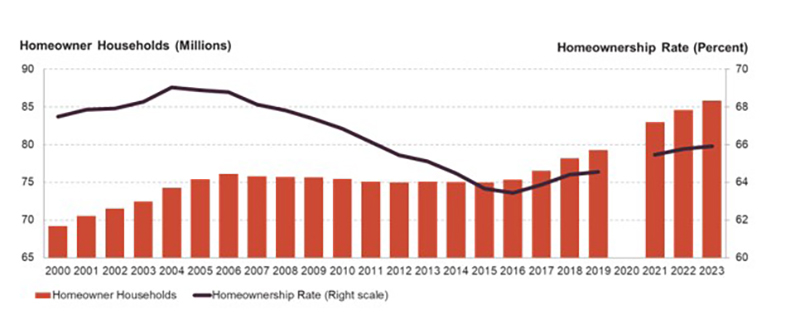

In 2024, rental construction is outpacing homeownership development at a staggering rate. Why? Rising mortgage and construction costs are putting homeownership further out of reach for many, making renting the more affordable option. Over the past year, the U.S. added 855,000 renter households, while multifamily construction reached its fastest pace since 1994, with 563,000 new units annually. Meanwhile, homeownership growth has slowed to its lowest rate since 2019.

READ ALSO: How NCREIF’s Not Put Senior Housing on the Map

This shift isn’t just about temporary housing solutions; it concerns the future of our neighborhoods, cities and the American dream of homeownership. For decades, homeownership has been a primary source of wealth accumulation for middle-class Americans. Yet, the gap between homeownership and rental costs has made this dream increasingly elusive. According to the Federal Reserve’s 2019 Survey of Consumer Finances, the median net worth of homeowners was about $255,000, while renters had a median net worth of only $6,300. This substantial difference highlights how owning a home can build equity and wealth over time.

But why is this happening, and what can we do to change it? The issue extends beyond high mortgage rates or record-breaking construction costs. While these are significant challenges, there are strategies we can implement to make homeownership more accessible to middle-income families.

Before we dive into solutions, let’s take a step back and examine some fundamental shifts in American households over recent decades that have reshaped the housing market:

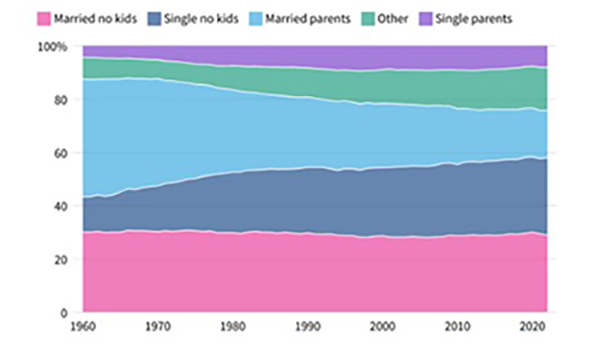

Household Size: U.S. household sizes have been steadily decreasing. In 1960, the average household size was 3.33 people. By 2022, it had dropped to 2.51. This shift reflects broader demographic and social changes, including a rise in single-person households and an aging population. Single-person households, for instance, grew from 13 percent of all households in 1960 to 28.9 percent in 2022. Other contributing factors include fewer children, an increase in older adults living alone and the rise of nontraditional living arrangements such as cohabiting partners.

Delayed Marriage: The average age at first marriage in the U.S. has been steadily increasing. In 1960, men married at a median age of 23, while women married at about 20. By 2018, the median age had risen to 29.8 years for men and 27.8 years for women.

Virtual Lifestyle: Shifting lifestyles and rapid technological advancements have fundamentally changed the way we live, reducing the demand for larger homes. The rise of remote work, online education and minimalistic living means that expansive homes once necessary for traditional offices, media rooms and storage are no longer a priority for many. Instead, more people are embracing a “virtual lifestyle,” where digital spaces replace physical ones. Additionally, modern home appliances are becoming smaller and more efficient, allowing for more compact kitchens and utility areas. Space-saving appliances—like slim-profile refrigerators, foldable furniture and dual-purpose items—are helping people to live in smaller spaces.

The growing trend toward smaller homes is evident. These homes are less expensive to build and more attainable for many middle-income families, meeting both housing needs and modern lifestyle preferences. However, the supply of these highly in-demand affordable homes is not nearly enough. This shortage is largely due to restrictive zoning laws. Contrary to popular belief, builders and developers don’t decide what to build. They respond to existing regulations and constraints, proposing what is the best and most feasible use of the land.

We must focus on building smaller homes for homeownership by optimizing land and infrastructure costs to reduce overall housing expenses. Structural challenges, particularly restrictive zoning and land-use regulations, are impeding the supply of this essential housing type. Comprehensive zoning reform, or upzoning, is needed to empower state and local efforts to deregulate land use and relax zoning laws. Only then will the market be able to respond effectively and make homeownership attainable once again.

Most Recent