The Outlook for Urban Multifamily Real Estate

With the new focus on suburbia, what will come of the urban multifamily investment market? Jason Weissman of Boston Realty Advisors explains.

Jason S. Weissman

A multitude of investors and investment groups have been routinely upping their ante to acquire hard real estate assets year-over-year. This diverse group includes a tapestry of family offices, hedge funds, institutional investors, high net worth individuals, wealth advisory firms and foreign equity, all of whom share a common goal—a need to put their money to work.

According to EY’s 2020 Global Alternative Fund Survey and following a multiyear trend, allocations to real estate increased to 26 percent from 23 percent the prior year.

The real estate industry in the U.S. is estimated to be worth more than $18 trillion and represents 13 percent of the GDP. Real estate investment opportunities include a large swath of assets to select from. One of the largest and most active segments of the industry is multifamily real estate in urban markets—specifically gateway cities throughout the U.S.

Historically, the urban multifamily sector has been one of the most secure and steady real estate investments, even during the Great Recession. For nearly 50 years, the global trend toward urbanization has been in vogue. People moved to cities in droves. The vital investment ingredients of high occupancy rates and consistent cash flow with little distress has made investing in urban multifamily a steady bet.

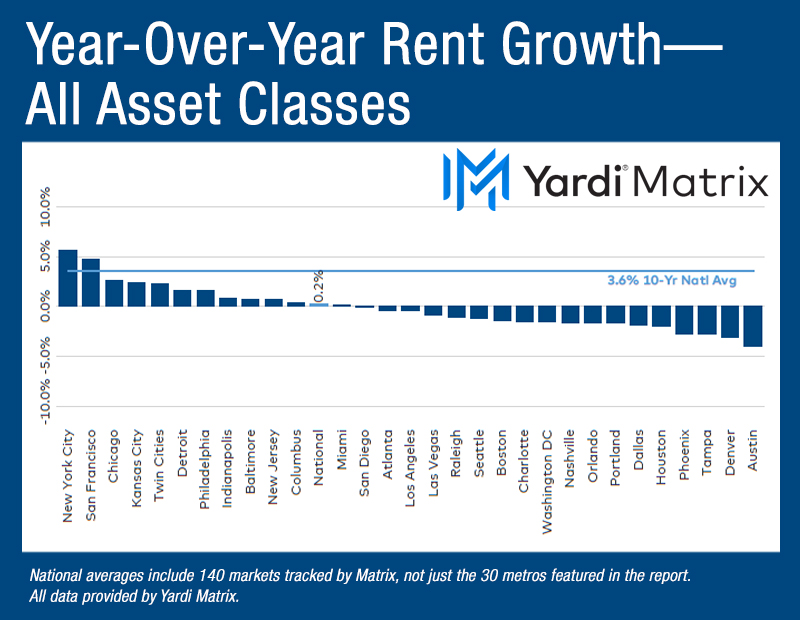

For the first time in decades, this sure bet on urban multifamily is up for debate. Since the start of the pandemic, investor appetite has augmented. As a result of most employees working from home, the appeal for urban multifamily has transitioned to suburban multifamily and suburban single-family rentals. Consequently, publicly traded single-family homebuilders, such as Toll Brothers and Pulte, are trading at all-time highs. Public REITs, who have exposure to urban multifamily, have been some of the weakest performers in the last 12 months.

Amongst many other byproducts of this pandemic, COVID-19 generated economic volatility and market unpredictability. With the new focus on suburbia, what is to come of the urban multifamily investment market?

Optimistic investors acquiring real estate today appreciate the required long-term investment horizon to maximize net operating income. Conservative investors are taking the long view. The good news is mutually shared, as optimists and conservatives alike are all betting on a recovery—with slightly different timelines.

Cautious and hesitant buyers have realigned their conventional underwriting criteria to “risk-off,” driven by their prediction of a rebound within the next four to five years. In the same supply-constrained gateway cities, optimistic, or “risk-on” investors are betting that gateway cities will rebound within the next two years.

History teaches us that cities always come back. Even when at their weakest, cities ultimately prove resilient and become enormous profit centers.

According to a Moody’s Analytics report, issued in the height of the pandemic, U.S. cities with collegiate centers and fast-growing tech hubs will be best positioned for a swift recovery.

In Boston, for example, the life science and technology sectors are tremendous assets for recovery. Recent commitments from companies such as Amazon and LogMeIn, as well as Sanofi and Moderna, all coupled with an abundance of intellectual capital, position Boston as one of the fastest cities to rebound in a post-COVID era.

The life science industry in Boston is expanding from traditional research and development to include biomanufacturing. This market increase has attracted an unprecedented investment for new life science development. In turn, this commercial growth will generate continued demand for multifamily housing throughout the city.

Further elevating support for betting on multifamily today is a recent report by NAREIT that indicated multifamily remained highly resilient in 2020, stating that rent deferrals and forbearances in multifamily properties were a small fraction compared to office and retail properties.

While the valuation of other asset types has tilted and other sectors have hit the investment pause button, cities such as Atlanta, Austin and Boston have urban multifamily properties trading at pre-COVID rates, with no pricing discounts.

Despite the realities of today, rent collection declines and falling occupancy rates—the urban multifamily market is alive and well. To validate this point, Freddie Mac, the nation’s multifamily housing finance leader, set a record in 2020 with $82.5 billion in multifamily loan purchases; most of those deals transacted in the latter half of the year and within gateway cities.

When we realize a full economic recovery, investors that are laser focused on urban multifamily today will be three steps ahead of the more conservative buyers still waiting on the sidelines. The collective investment community should play their cards today. Those that don’t will be kicking themselves in five years for holding their chips.

Jason S. Weissman was born in Boston and graduated from Curry College in three years and received an MBA from Babson College. Weissman founded Boston Realty Advisors in 2001. He launched the firm with multiple service lines under one roof—created leadership roles for multifamily, office, retail, hospitality and user housing—and became the largest, independent real estate services firm in New England. Weissman manages the investment sales and capital markets platform, with an owner-aligned philosophy. He is also the founder of The Broadway Co., a real estate investment company with more than 60 investment properties in North America and is an active member of numerous organizations including the International Council of Shopping Centers.