National Multifamily Report – June 2026

The first half was solid, though still below pre-pandemic expectations.

The U.S. average advertised asking rent increased by 1 percent during the first half of 2026, according to Yardi Matrix’s latest survey of 140 markets. While on par with previous years, growth still fell below the pre-pandemic rate of 2.7 percent recorded between 2013 and 2019. Year-over-year, rates ticked up 0.2 percent in June, climbing $4 to $1,763. The single-family build-to-rent sector’s improvement rate outpaced its multifamily counterpart, with rents going up 1.1 percent during the first six months of 2026. The market’s performance turned annual growth positive at 0.2 percent in June as advertised rents climbed $6 to $2,234.

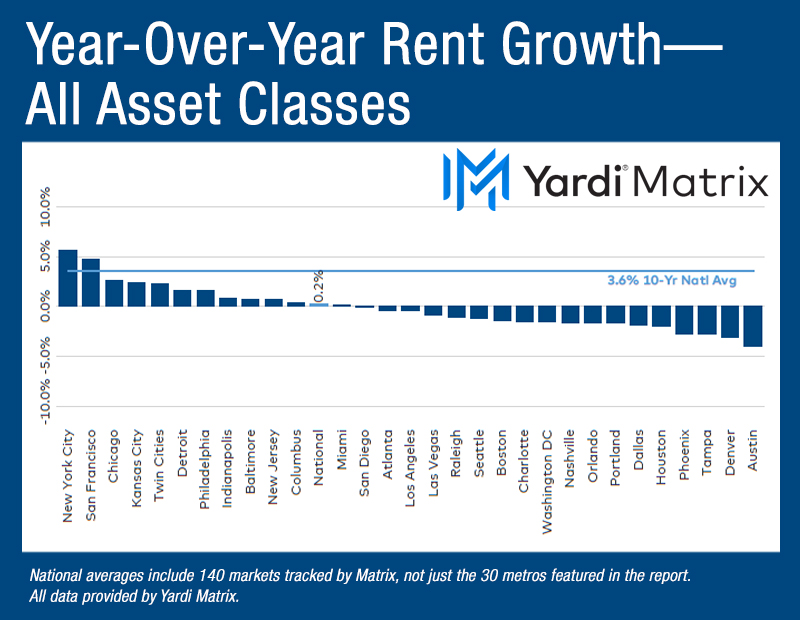

Gateway and Midwest markets continued dominating advertised rent growth charts, with New York leading the way at a 5.6 percent year-over-year increase in June, followed by San Francisco (4.7 percent) and Chicago (2.6 percent), as well as Kansas City (2.4 percent) and the Twin Cities (2.2 percent). Sun Belt metros posted the usual negative rent growth, with Austin, Texas, rates declining 4.0 percent, while Denver (-3.1 percent) and Tampa, Fla. (-2.8 percent) followed the same trends. Moderating demand characterized by an absorption of just 108,000 units during the first five months, down 61 percent year-over-year, together with persistent deliveries, played a part in the 0.6 percent annual decline in the national occupancy, which stood at 94.1 percent in June.

Market-level RBN performance spreads widen

Short-term gains clocked in at 0.2 percent in June, while advertised rates ticked up 0.7 percent during the second quarter—a figure below the 1.8 percent pre-pandemic average growth rate. More than two-thirds of Matrix’s top 30 markets recorded monthly gains, with both Lifestyle and Renter-by-Necessity ticking up by 0.2 percent in June. However, RBN spreads were wider with markets such as New York (2.6 percent) and San Francisco (0.4 percent) witnessing heightened growth while metros such as Charlotte (-0.4 percent), Austin and Houston (-0.3 percent each) softened. This gap reflects affordability pressures in lower-income households amid a bifurcating economy, which reduces the capacity of such residents to absorb rent increases.

Despite headwinds, investors continue to seek a foothold within the multifamily sector. With limited equity opportunities, entities increasingly turn toward debt as a means of securing a spot on the capital stack. This year’s proliferation of debt products underscores the burgeoning supply, including a bullish appetite for the pooling of multifamily-only CMBS deals for the first time since the Great Recession. Freddie also started offering junior credit-linked notes not secured by properties instead of the junior B-pieces of its K-Series. Other new debt products include D2 Asset Management and Natixis’ offering, which may go as high as 75 percent loan-to-value, as well as JP Morgan and MF1, which issued a multifamily-only CMBS deal in May, to name a few.

Advertised single-family build-to-rent rate growth turned positive, increasing 0.2 percent year-over-year in June, climbing $6 to $2,234. Rents increased despite softening demand, as occupancy rates declined by 30 basis points to 94.7 percent in June, down from a year ago. A divergence emerged in property performance, with Lifestyle rent growth recording a 0.2 percent annual decline while RBN rates grew 3.3 percent. At a granular level, the spread reached as high as 950 basis points with markets such as Nashville (down 0.5 percent Lifestyle, but up 11.5 percent RBN) and the Inland Empire (down 2.2 percent Lifestyle, up 11.1 percent RBN).