A Closer Look at the Multifamily Maturity Wall and Refinancing Crisis

Last year’s loan maturities represented nearly triple the 20-year average, creating unprecedented pressure.

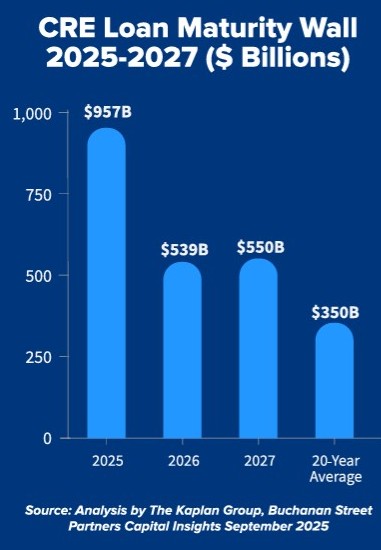

Refinancing risk for multifamily and commercial real estate debt will remain high for at least the next two years as much of the $957 billion in loans—including $310 billion in multifamily debt—that matured in 2025 received extensions.

While borrowers may have bought some time to pay off loans, new estimates point to another large wave of maturities this year as interest rates remain elevated and banks stay cautious when it comes to CRE lending. For 2026, the maturity wall is estimated at $539 billion, rising to $550 billion in 2027.

A report by The Kaplan Group on the State of U.S. Business Debt states that the total amount of CRE loans that matured in 2025 represented nearly triple the 20-year average, creating what it calls unprecedented refinancing pressure. Adding to the financing challenges, cap rates for multifamily properties range between 5.4 to 5.7 percent. Additionally, compressed yields, despite surging financing costs, can create negative leverage scenarios. “Nearly half of apartment properties may struggle to secure refinancing at sustainable terms,” according to the report.

In its outlook for 2026, the group states improvement in financing conditions is likely to be slow and uneven with outcomes depending on sector, geography and how aggressively companies manage cash, debt and collections.

READ ALSO: Real Estate Fundraising Recovers, but It’s Not Because of Multifamily

The Federal Reserve’s shift from a 5.25 peak policy rate in 2023 to the mid-3 percent range by late 2025 provides only partial relief because many borrowers are refinancing into structurally higher-for-longer debt costs than the 2010s.

At the most recent meeting of the Federal Open Market Committee on Jan. 28, Federal Reserve Chairman Jerome Powell announced that the Fed decided to keep rates steady with the federal funds rate at 3.5 to 3.75 percent. The last cut was in December, when the Fed agreed to a 25-basis-point reduction. The rate is now down 75 basis points from a year ago, when the target range was 4.25 to 4.5 percent.

A steep climb

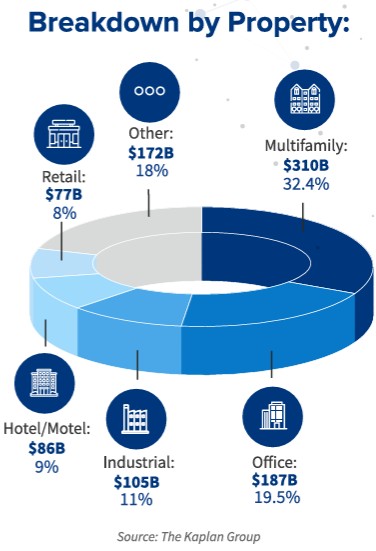

The report notes the $310 billion multifamily maturity wall is the steepest for borrowers to climb, representing 32.4 percent of the $957 billion total CRE debt that matured in 2025. The next highest piece of the maturity pie is the office sector, with $187 billion in loans due, or 19.5 percent of the total. A catchall category called “other” takes up 18 percent of the debt, with $172 billion in maturing loans. Industrial debt amounting to $105 billion represents 11 percent of the total, with hospitality loans totaling $86 billion, or 9 percent and retail loans totaling $77 billion representing 8 percent of maturing debt.

Of the total $957 billion in CRE loans maturing in 2025, The Kaplan Group estimated only 50 to 55 percent were paid off.

The report states there is severe distress in securitized commercial real estate debt because the commercial mortgage-backed security delinquency rates are 7.29 percent—nearly six times higher than traditional bank loans. The multifamily CMBS delinquency rate was 6.59 percent as of September, according to The Kaplan Group.

The delinquency rates for other lender types were: 1.29 percent for banks and thrifts; 0.61 percent from Fannie Mae and 0.51 percent life from insurance companies. The overall CRE delinquency rate was 1.57 percent as of the second quarter of 2025.

Multiple pressure points

The Kaplan Group’s analysis stated sustained pressure from multiple pressure points rather than a single crisis moment have created the conditions that borrowers will have to continue to navigate as they attempt to manage their debt in 2026. The report points to tighter credit, higher-for-longer interest costs and tariff-driven price shocks that have reshaped the risk landscape for U.S. companies.

“The maturity wall is at unprecedented highs at a time that interest rates are increasing, making refinancing extremely difficult. Lenders fear a wave of defaults that could make the collateral less valuable, leading to massive losses. The situation is so precarious that many lenders chose to give short term extensions to 2025 maturities to avoid immediate defaults,” Dean Kaplan, president, The Kaplan Group, told Multi-Housing News.

Kaplan said the current multifamily maturity wall is fundamentally different from previous CRE debt crises in both scale and structural dynamics because it is a direct result result of the extraordinary acquisition activity in 2020-2022 when multifamily was seen as a pandemic-resilient asset class.

“Unlike previous crises where falling values and distress were the primary drivers, today’s multifamily maturity wall is characterized by a severe interest rate mismatch. Properties underwritten at 2.5 to 3.5 percent interest rates in 2021 are now facing refinancing at rates in the 5 to 6 percent range or higher,” Kaplan said.

For example, the sharp increase in tariffs made it much more expensive for many businesses to bring in supplies from other countries in 2025. The report estimates there was a 342 percent tariff rate increase that generated $80.3 billion in new costs from January through July 2025. The higher costs put more pressure on company budgets to borrow more money for operating expenses.

High-vulnerability sectors like construction, retail, electronics and import manufacturing were among those impacted the most with tariff costs rising an estimated 10 to 25 percent. The increased tariff rates created acute working capital strain in import-dependent sectors, according to The Kaplan Group.