Denver Multifamily Report – September 2024

Details on what’s shaping this key Rocky Mountain market.

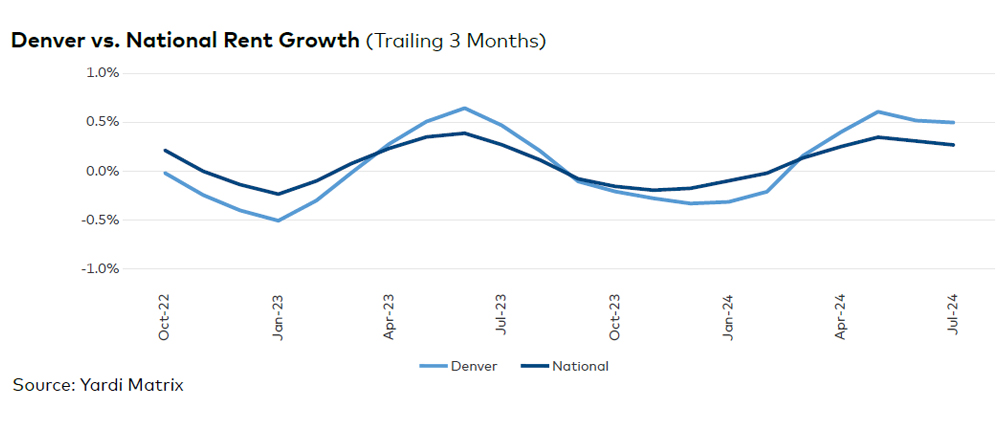

Steady population and employment expansion helped Denver’s rent growth rebound toward the end of the first quarter, and the positive momentum continued amid a strong development pipeline. Average advertised asking rents rose 0.5 percent on a trailing three-month basis through July, to $1,960, while the occupancy rate for stabilized properties declined 30 basis points year-over year, to 94.8 percent, in June. The average U.S. advertised asking rent was up 0.3 percent, on a T3 basis through July, to $1,743, while occupancy declined 40 basis points, to 94.6 percent.

Denver’s jobless rate rose to 4.0 percent in June. The rate was the highest it’s been since early 2022 and 10 basis points ahead of the U.S. figure, according to preliminary data from the Bureau of Labor Statistics. Employment slowed to 0.9 percent over the 12-month period ending in May, below the 1.3 percent national average. The metro gained 6,400 jobs. The government and education and health services sectors added a combined 24,100 positions. Meanwhile, the largest losses were recorded in trade, transportation and utilities (-8,700 jobs) and mining, logging and construction (-5,100 jobs).

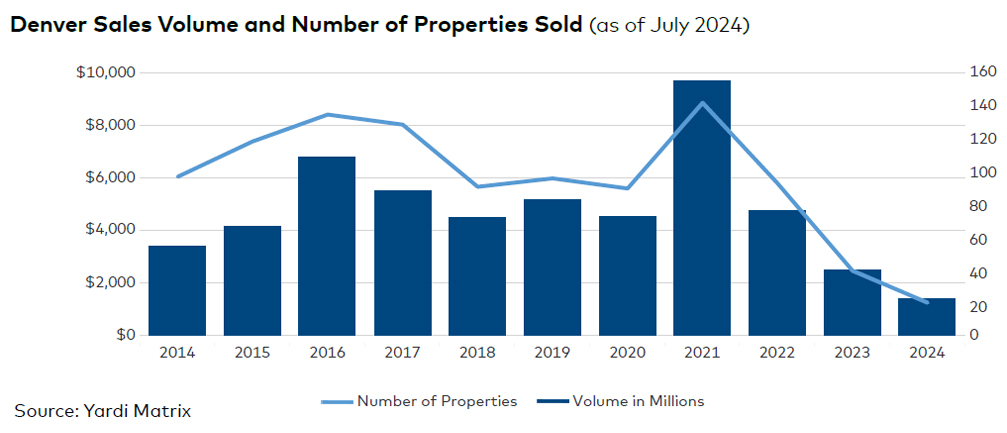

Development was strong, with a robust pipeline and steady deliveries, but new construction decelerated significantly. In 2024 through July, developers delivered 6,871 units and had another 39,088 underway. Investment activity remained limited, totaling just $1.4 billion, with the average per-unit price down 14.3 percent since December.