Twin Cities Multifamily Report – January 2024

While still healthy, the Minneapolis-St. Paul market has slowed.

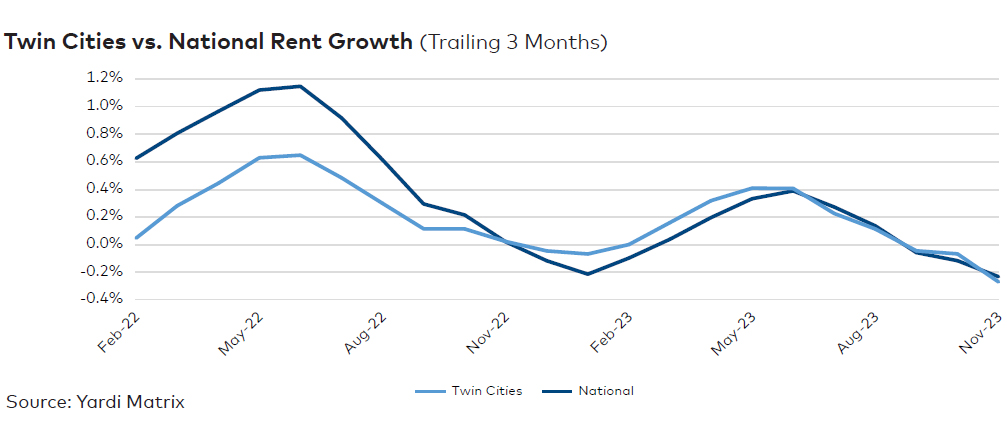

The Minneapolis-St. Paul market showed moderate results toward the end of 2023, with rents down 0.3 percent on a trailing three-month basis, to $1,473. That was similar to the slide in the national average, which was down 0.2 percent to $1,713 as of November. Both were affected by seasonal trends. In a rare feat for this year, the average overall occupancy rate in stabilized properties was flat over 12 months in the Twin Cities, at 95.1 percent in October.

The metro added 32,800 net jobs in the 12 months ending in September 2023, up 1.8 percent, 60 basis points below the national rate. The unemployment rate clocked in at a very tight 2.9 percent as of October, 100 basis points lower than the U.S. figure, according to preliminary data from the Bureau of Labor Statistics. A survey conducted by the Minneapolis branch of the Federal Reserve found that high interest rates had a less significant impact on the infrastructure and industrial sectors than on the residential market.

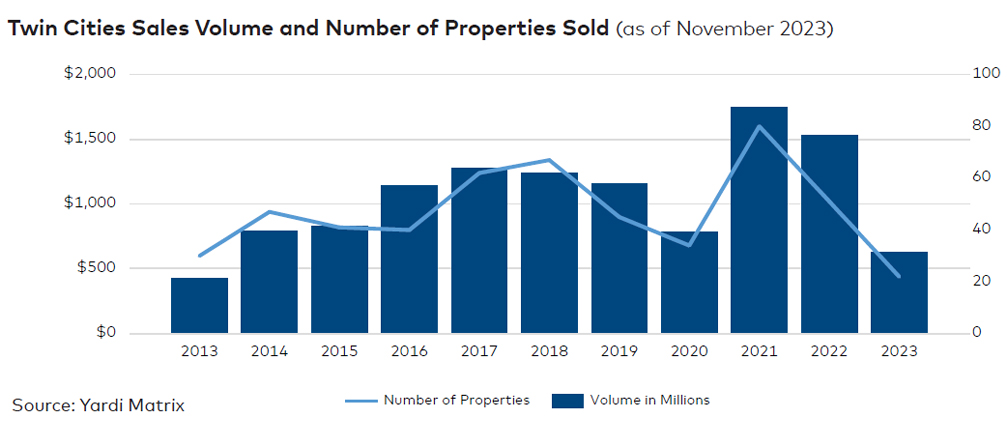

Developers had 18,416 units under construction as of November 2023. Of the apartments underway, more than 8,000 units broke ground in 2023 through November, keeping the pipeline’s pace close to figures recorded in 2022. Investment, on the other hand, saw a major slowdown, with only $631 million in multifamily transactions in the first 11 months of the year. That fell significantly short of the $1.5 billion recorded during the same time frame of 2022.