Orlando Closes the Year in Style

As population gains further bolster demand, multifamily rents are prone to above-trend growth in the foreseeable future.

By Robert Demeter

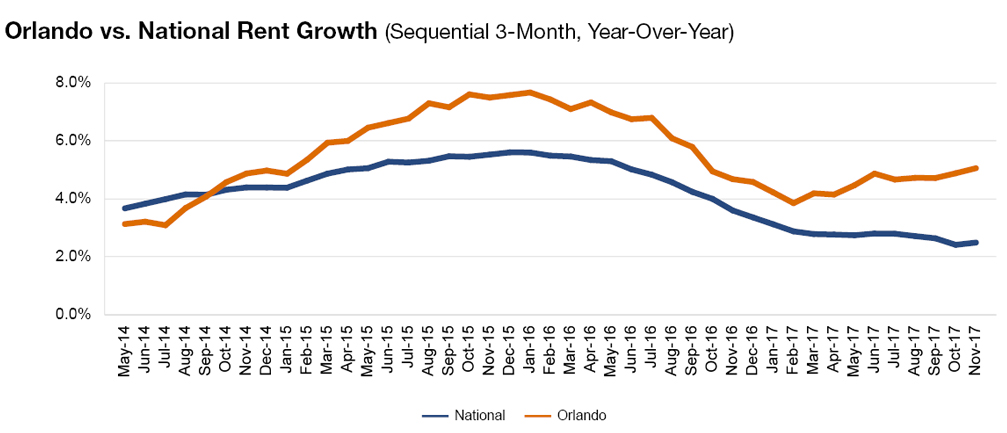

Orlando rent evolution, click to enlarge

Solid population and job gains are keeping Orlando’s economy on track, along with generating rental demand and balancing out the city’s rapidly growing multifamily pipeline. Investors didn’t shy away from the metro in 2017. Rather, they pushed transaction volume to a cycle peak almost an entire quarter before year-end, signaling once more that the city’s rental market is thriving.

Orlando added 26,200 jobs in the 12 months ending in September 2017, marking a 3.3 percent increase, well above the 1.9 percent national average. Employment gains were highest in the leisure-and-hospitality sector, followed by construction and transportation. Financial activities saw an uptick, too, adding 3,700 jobs year-over-year, mainly due to Deloitte’s and ADP’s recent expansions in the city. In addition to an overhaul of Interstate 4, there is a $1.3 billion construction of a train station underway, along with a $1.8 billion airport renovation, a handful of mixed-use developments and more than 8,300 multifamily units.

Some 5,200 units came online in 2017 through November, less than 500 of them in fully affordable properties, as developers continue to focus on upscale projects. This trend continues to put pressure on low- and middle-income residents, with working-class rents growing at a faster rate than those for higher-end communities. And as population growth further bolsters demand, Orlando rents are prone to above-trend growth for the foreseeable future.