Oahu’s Improving Office Market Sees Strong Investor and Leasing Activity

In the context of an improving economy led by tourism, Oahu’s office market remained stable during the second quarter of 2014, with a positive quarter-over-quarter net absorption of 14,094 sq. ft.

By Adriana Pop, Associate Editor

Oahu, Hawaii—In the context of an improving economy led by tourism, Oahu’s office market remained stable during the second quarter of 2014, with a positive quarter-over-quarter net absorption of 14,094 sq. ft.

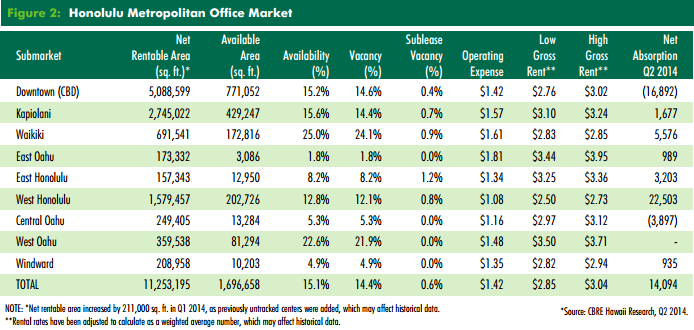

In Honolulu, research data from CBRE shows that the vacancy rate decreased, going from 14.5 percent in Q1 to 14.4 percent by mid-year, while the average gross asking rent of $2.95 per square foot remained relatively stable for the prior six quarters.

In Honolulu, research data from CBRE shows that the vacancy rate decreased, going from 14.5 percent in Q1 to 14.4 percent by mid-year, while the average gross asking rent of $2.95 per square foot remained relatively stable for the prior six quarters.

These trends can be attributed to the higher demand for office space generated by tourism-based businesses statewide.

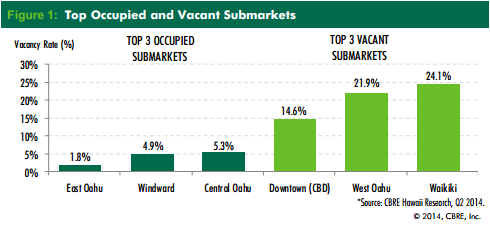

The city’s suburban area experienced the highest improvements in vacancy, as well as increased long-term leasing activity. East Oahu, Windward and Central Oahu are the region’s most occupied submarkets, while Downtown Honolulu, West Oahu and Waikiki experience the highest vacancy rates.

The city’s suburban area experienced the highest improvements in vacancy, as well as increased long-term leasing activity. East Oahu, Windward and Central Oahu are the region’s most occupied submarkets, while Downtown Honolulu, West Oahu and Waikiki experience the highest vacancy rates.

The second quarter of 2014 also ended with a series of notable office building sales in Honolulu. In June for instance, two California firms—Atalanta Realty Investments and McKinney Capital Group—purchased a total of three Downtown office properties.

The second quarter of 2014 also ended with a series of notable office building sales in Honolulu. In June for instance, two California firms—Atalanta Realty Investments and McKinney Capital Group—purchased a total of three Downtown office properties.

For the first half of 2014, however, the Oahu office market experienced a negative year-to-date net absorption of 113,622 sq. ft. Also, the total positive net absorption of 14,049 sq. ft. in Q2 2014 was lower than the total positive net absorption of 53,136 sq. ft. in Q2 2013.

Hawaii’s unemployment rate decreased year-over-year, going from 4.9 percent in 2013 to 4.4 percent during Q2 2014, according to a report released by the Bureau of Labor Statistics. This rate continues to be lower than the national average of 6.3 percent and has remained so for the past 35 years.

In Honolulu, the overall unemployment rate was 4.2 percent as of May 2014. Year-over-year, employment in the city’s office-using sectors increased by 2.5 percent for the financial services industry and by 1.1 percent for the professional and business services sector.

Hawaii’s retail sector remains positive

The overall retail market in Hawaii experienced a positive quarter-over-quarter net absorption of 20,236 sq. ft. during Q2 2014, according to the CBRE Inc. Hawaii Second Quarter 2014 Hawaii Retail MarketView.

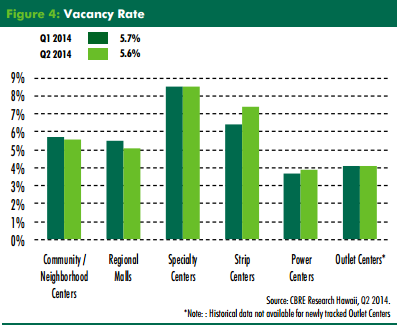

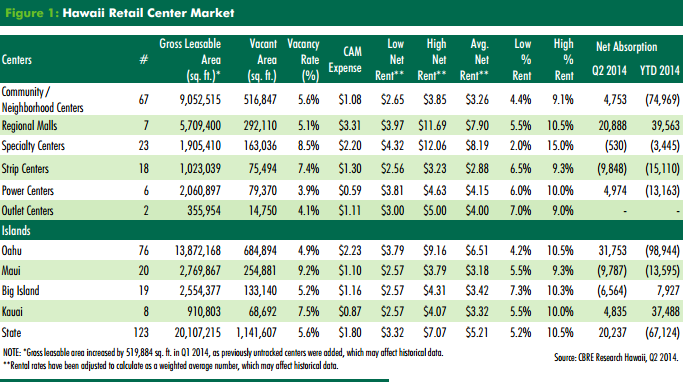

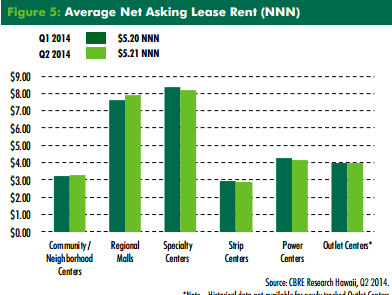

Statewide, the sector’s vacancy rate decreased slightly from 5.7 percent to 5.6 percent within the same period. Community and neighborhood centers saw the greatest vacancy improvements, along with the resort centers, which were the best performing locations since they have a higher exposure to tourists and locals alike. Meanwhile, the occupancy rate for specialty and outlet centers remained flat.

Statewide, the sector’s vacancy rate decreased slightly from 5.7 percent to 5.6 percent within the same period. Community and neighborhood centers saw the greatest vacancy improvements, along with the resort centers, which were the best performing locations since they have a higher exposure to tourists and locals alike. Meanwhile, the occupancy rate for specialty and outlet centers remained flat.

Hawaii’s average gross asking rent, along with the average net asking rate remained virtually unchanged quarter-over-quarter, at 7.00 per sq. ft. triple net (NNN) and $5.21 per sq. ft. NNN, respectively.

Hawaii’s average gross asking rent, along with the average net asking rate remained virtually unchanged quarter-over-quarter, at 7.00 per sq. ft. triple net (NNN) and $5.21 per sq. ft. NNN, respectively.

Leasing and sales activities remained strong, as national retailers continued to expand their businesses across Oahu and the neighbor islands.

Furthermore, by the end of the first half of 2014, Hawaii’s retail and hotel industry attracted a total of more than $1 billion in investments.

Notable transactions and announcements included Macy’s commitment to anchor the regional mall development, Ka Makana Alii in West Oahu, the Royal Hawaiian Center leasehold sale to J.P. Morgan Asset Management (in Waikiki), and Whole Foods Market’s decision to open a flagship store at Ward Properties in Honolulu’s Kakaako district.

Hawaii’s industrial market garners investment interest despite modest negative net absorption

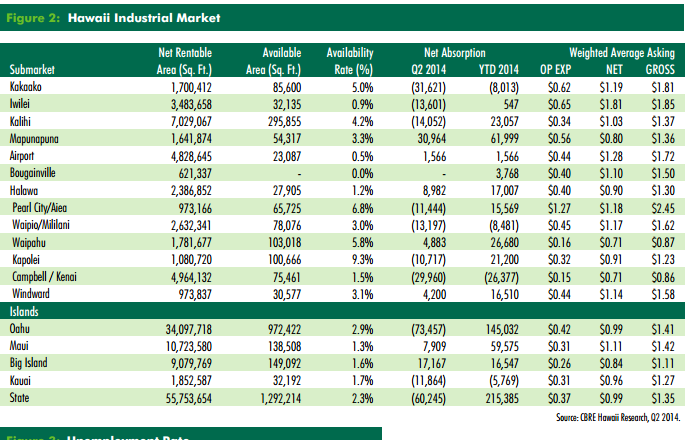

During the second quarter of 2014, Hawaii’s industrial market saw a negative net absorption year-over-year of 60,245 sq. ft., according to the CBRE Inc. Hawaii Second Quarter 2014 Hawaii Industrial MarketView.

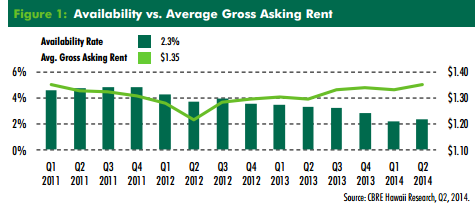

Within the same period, the availability rate decreased across all islands, going from 3.3 percent in Q2 2013 to 2.3 percent in Q2 2014. Pearl City/Aiea, Kapolei and Windward were the best performing locations on Oahu.

Within the same period, the availability rate decreased across all islands, going from 3.3 percent in Q2 2013 to 2.3 percent in Q2 2014. Pearl City/Aiea, Kapolei and Windward were the best performing locations on Oahu.

On a quarter-over-quarter basis however, availability increased slightly, going from 2.2 percent in Q1 to 2.3 percent, while the base asking lease rents remained unchanged at $0.99 per sq. ft. NNN. In the near future however, lease rates are expected to go up with the tightening of the market.

As statewide industrial space remained minimal in Q2 2014, the volume of lease transactions was less than 5,000 sq. ft., below the level of the previous quarter.

As statewide industrial space remained minimal in Q2 2014, the volume of lease transactions was less than 5,000 sq. ft., below the level of the previous quarter.

On Oahu, industrial sales activity totaled about $19 million lower than the level registered in 2013.

Notable industrial land transactions within the same period included the purchase of the 54-acre Kapolei Business Park Phase 2 by Avalon Development Co. and Walton Street Capital LLC of Chicago. The joint venture paid $24 million for the property. In a separate transaction, the companies also acquired the 123-acre Kapolei Business Park West in West Oahu for approximately $60 million. Meanwhile, Eagle Leasing Inc. of Alabama purchased 3 acres of industrial land in Kapolei for $3.8 million.