New Bridges for Affordable Housing’s Financing Gap

Here’s how stakeholders are stepping up and moving projects forward.

The affordable housing sector is evolving as developers address the housing gap across the nation. Challenges these projects have faced over the years continue to shift with the market and ongoing cycles.

Recent legislation, such as the One Big Beautiful Bill jumpstart development, but financing remains uneven across markets. “The effort to put together a capital stack has only gotten more challenging,” said Dave Borsos, vice president of capital markets and student housing at the National Multifamily Housing Council.

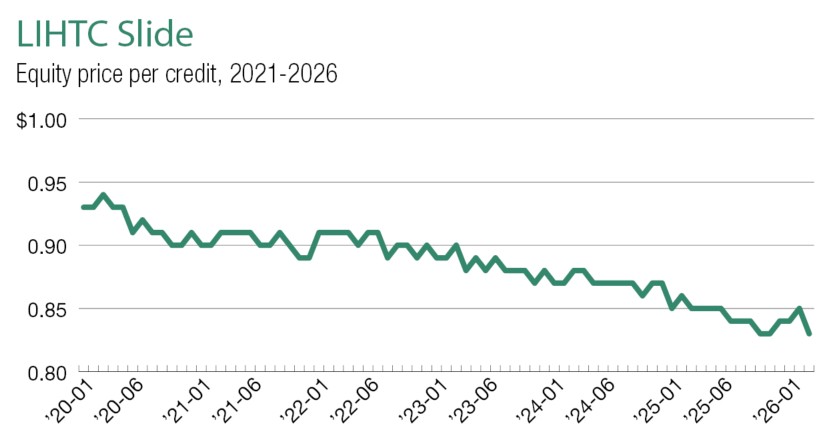

The main challenge in creating a capital stack for development in this environment is a weaker tax credit equity market. This has resulted in developers and investors rethinking and adjusting the way they put affordable financing deals together.

The weakening tax equity is posing a real challenge for tax credit equity on these projects. The One Big Beautiful Bill lowered the bond requirements to 25 percent, so that more projects can qualify for the program.

That has increased the supply of credits, pushing values down to about 80 cents from close to $1. The price reduction has created a gap in developer pro formas that needs to be addressed, noted Julie Sharp, an executive vice president at Merchants Capital.

State programs fill the financing gap

“Every deal is still a challenge,” commented Merchants Capital President & CEO Michael Dury. There’s still plenty of liquidity on the debt side, but the gap in tax credit equity is stalling deals across the board.

“Soft money”—state and local government subsidies such as grants, abatements and tax-increment financing—continues to be a reliable avenue of financing as public agencies find new ways to play a larger role. Stockton Williams, executive director at the National Council of State Housing Agencies, cited a first-of-a-kind program that could provide a model for other states.

As part of Massachusetts’ $5 billion Affordable Homes Act, in 2025 the state launched the Momentum Fund, focused on promoting mixed-income housing development. Administered by MassHousing, a quasi-public housing finance agency, the $50 million vehicle provides low-cost capital that complements privately sourced equity. All told, the fund is initially targeting the development of 1,000 mixed-income units.

The first project to tap into the new funding stream is The Residences at East Milton, a $52 million mixed-income community in Milton, Mass., a suburb south of Boston. Developed by Joseph J. Corcoran Co. and Falconi Properties, the project received $5 million in Momentum Fund equity, plus $29.8 million in permanent financing from Freddie Mac, Berkadia and MassHousing. Twenty-three of the community’s 92 units are designated for residents earning 80 percent of area median income.

There’s a huge amount of debt available in the marketplace right now.

—Dave Borsos, Vice President of Capital Markets and Student Housing, NMHC

On a much larger scale, New York City announced in April that it will invest $4 billion of pension money to finance affordable housing projects under the NYC Housing Investment Initiative. Over the next four years, the vehicle will target mixed-income, workforce and affordable housing while supporting the preservation of existing assets.

On the West Coast, Los Angeles County is also exploring new avenues toward meeting an affordable housing shortfall that’s estimated at 500,000-plus units. A half-cent county sales tax authorized in 2024 is generating funds for supporting affordable housing, with the Los Angeles County Affordable Housing Solutions Agency allocating a portion of the Measure A proceeds.

Projects may be eligible whether they need additional financing to complement LIHTC or if they haven’t secured those credits but are eligible for tax-exempt bonds. In April, the agency signed off on its first round of financing—$102 million for 10 affordable projects representing $341 million in investment.

Focus on feasibility

In an environment where construction costs are up and equity flows haven’t kept pace, affordable developers are looking for feasible paths. At The NHP Foundation, the current focus is on preservation and renovation opportunities, rather than new construction. “The timing and availability of resources are rarely, if ever, in sync,” observed Joseph Weatherly, the nonprofit’s CIO. “You’re trying to pin down a lot of moving pieces and parts. The most important thing is that you stay vigilant and understand what’s going on in the market at large.”

Since NHP has a national footprint, understanding each local market is vital. Pursuing a preservation project is a cost-effective strategy that offers more flexible financing and lower risk. As Weatherly noted, a new construction project could cost upward of $300,000 to $400,000 per unit, while a renovation project is a more scalable $80,000 per unit.

In Missouri, the company is working on a preservation project for St. Luke’s Plaza, a 219-unit community in St. Louis’ Central West End. NHP is recapitalizing and renovating the asset through multiple federal and state programs. Completed in 1929, the property is listed on the National Register of Historic Places, making it eligible for historic tax credits, as well as LIHTC financing. NHP is taking a similar approach to financing restoration and preservation projects in Virginia, Weatherly added.

Development hurdles continue to complicate projects across the board, even those that incorporate affordability through mixed-income models. While the strategy aims to balance different revenue streams, it can also add complexity to financing. “No … they’re not easier,” said Jonathan Curtis, managing partner at Cedar Street. Structuring these deals still requires navigating multiple layers of funding and approvals.

If we can solve equity, we could have a lot of affordable housing that could be built and that would solve a major problem.

—Michael Dury, President & CEO, Merchants Capital

The company’s long road to launching its project illustrates the obstacles that often make preservation a more attractive option. For six years, Cedar Street encountered community and city opposition to its plans for 600 Foothill, a mixed-income project in La Cañada Flintridge, Calif., an upscale suburb north of Pasadena, near Los Angeles. The project finally moved forward in November 2025 under the state Housing Accountability Law’s “builder’s remedy.”

The provision enables developers to bypass local approval if the city’s restrictions are not compliant with the state law. California Gov. Gavin Newsom and Attorney General Rob Bonta stepped in on Cedar Street’s behalf. The finished ground-up product will incorporate 80 residential units, with 16 of them being affordable; 16 non-serviced guest units for visitors; and 7.30 square feet of office space. Such barriers to construction highlight how increasingly complex financing and capital stacks are pushing developers toward preservation as a more feasible option.

Developers tap alternative solutions

When it comes to new development opportunities for affordable communities, companies must be more creative to get projects off the ground. To address these challenges, developers are leveraging state and local financing grants alongside new development models to continue advancing projects.

There’s no “silver bullet” for the issue, pointed out Lori Chatman, president of the capital division at Enterprise Community Partners. “The bigger challenge right now is what continues to be the additional gap financing that affordable housing developments often need.”

Chatman suggested a strategy of mixed-income developments that make projects more feasible in this environment. State housing agencies are also expanding their resources to fund these project models. For example, Williams pointed to the tax exemption for “missing-middle” apartment construction in Florida, which has resulted in the delivery of more than 3,100 units since 2023.

Another strategy Chatman promotes is modular housing. She said that in places that Enterprise finances, the company is seeing developers using modular units that can come to market faster and at a cheaper price, when labor and project costs are higher.

On the nonprofit side, NHP is leaning into 501(c)(3) bonds to help the company build and acquire assets. These bonds lower costs and increase in value when they’re sold in the market.

“We’re able to use 501(c)(3) bonds, and because of our credit rating, those bonds are less risky to buyers, which brings our interest rates down,” Weatherly noted.

In the current financing environment, affordable housing projects are not necessarily harder than they were in the past, but they’re facing different challenges. From weaker equity and changing policies on development, new strategies are emerging to build and preserve the housing stock.

“We need to be more creative—both in preserving existing housing and in developing new models without relying solely on federal subsidies,” Chatman said.