Discount Deals Signal a New Cycle

Price adjustments present opportunities for stabilized property purchases.

Earlier in the decade, when interest rates were 0 percent or near 0 percent, multifamily investors bet on rising rents and capitalization-rate compression to drive highly leveraged returns. Today, amid a significant revaluation of assets, investors are buying stabilized assets well below replacement cost and banking on multifamily’s proven stability.

The transition has signaled the official arrival of a new market cycle in a higher but arguably more normalized interest rate environment. It suggests that a growing number of sellers continue to capitulate to the idea that the elevated cost of capital regime—and the uptick in cap rates—will persist.

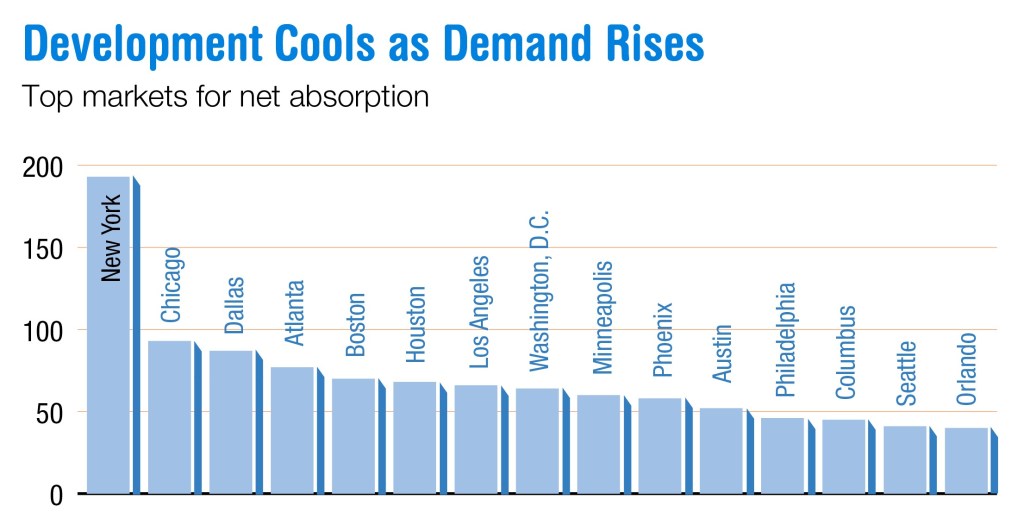

It also indicates that investors are betting that ramped-up demand will eventually negate oversupply issues as development cools. Indeed, markets such as Austin, Phoenix and Atlanta—all of which experienced booming apartment construction over the last few years—were among the top 15 markets ranked by absorption in the second quarter, according to CBRE.

“If you can acquire multifamily assets at the right basis, you’ll have some runway to raise rents as the next cycle really takes off and construction goes away or lessens significantly,” said Jon Siegel, co-founder & CIO of RailField Partners.

Founded by former Fannie Mae executives, the 12-year-old firm initially focused on Texas but has since expanded its presence to the Mid-Atlantic, the Southeast and, most recently, the Midwest.

Among other deals, RailField is currently looking at an asset that’s in a better location and would cost less than a similar property it bought a few years ago in the same Southeast submarket, according to Siegel.

For Slate Asset Management, the new dynamic has reignited interest in U.S. multifamily equity investments after preferring the credit side of the business over the last several years. In July, the $9 billion global alternative asset investor paid $226.5 million for 1,600 units across six apartment communities concentrated in major metros Phoenix, Atlanta and Tampa, Fla.

The supply story has impacted everything from A- to C-quality assets, so there could be some volatility in the short term. As markets get closer to equilibrium and rents grow moderately again, we’re in good shape. If they outperform, that’s gravy.

—Brennen Degner, Co-Founder & CEO, Platte Canyon Capital

The asset, fetched for about 40 percent below replacement cost, matched Slate’s appetite for workforce housing with low rent-to-household income metrics relative to the market, shared Peter Tsoulogiannis, CIO & partner at the firm’s Chicago office.

That approach tends to promote steady cash flow growth over time, he added. Slate also emphasizes infill locations that are close to employers, supermarkets, schools, medical services and other everyday essentials.

“We like getting assets that are fundamentally sound that were trading for much higher prices when interest rates were 0 percent. That allows us to make what we think is a more rational real estate investment decision.”

Dialing up discounts

Slate typically looks for opportunities where sellers who are facing a debt maturity or interest rate caps expiration will accept a discount, noted Tsoulogiannis. It’s a strategy being followed by other apartment investors, including Blackfin Real Estate Investors.

In June, Blackfin acquired a nine-year-old, 120-unit garden style apartment community in Augusta, Ga., for $17.3 million or some $144,000 per door. That represented a discount of more than 40 percent to what such an asset was trading for a few years ago, said Doug Root, a co-founder & managing partner of the firm.

Like other investors, Root reported that sellers are returning to the market for the second or third time after previously pulling deals over the last couple of years because of unmet price expectations. Root and other investors acknowledge that many are holding out for a decline in interest rates to boost value and refuse to meet buyer price expectations. That’s the case even in markets like the Southeast that have seen significant new supply and declining rent growth or rental rates in freefall.

“You would think that sellers would be more motivated, but we haven’t seen nearly the transaction volume that we had hoped for,” said Root, whose firm is focused on the Southeast, Mid-Atlantic and Northeast. “We’re optimistic we’ll see more in the near term, but it’s difficult to get anything done today.”

Fits and starts

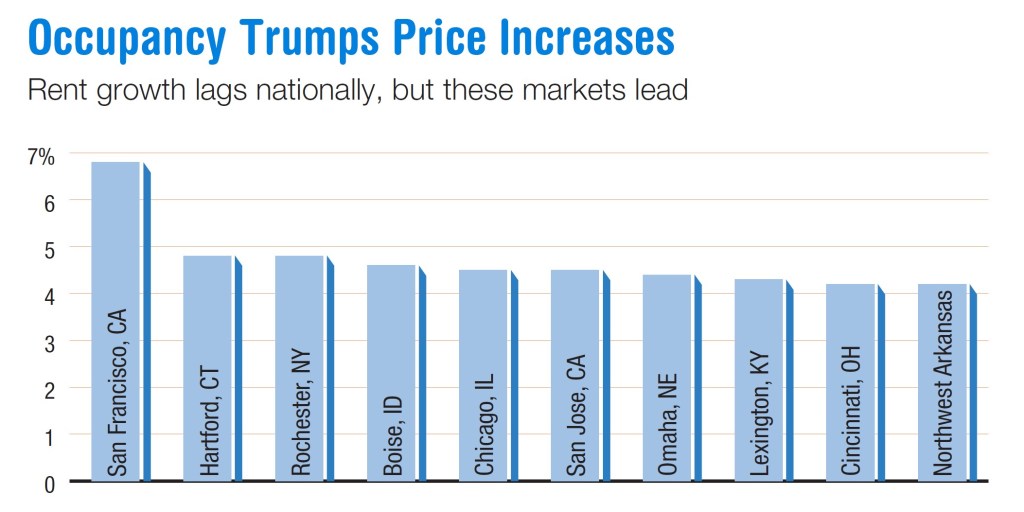

That sentiment is reflected in transactions, which began the year on an upswing and buoyed the transaction outlook, observers say. But apartment sales volume of $35.1 billion in the second quarter this year represented a decline of 14 percent from the prior year, according to commercial property researcher MSCI Real Assets, which tracks sales of $2.5 million and up. Volume for the first half of 2025 was still up 5 percent year-over-year. Meanwhile, MSCI reported that average apartment cap rates of 5.7 percent in the second quarter was more than 100 basis points higher than in 2022.

In addition to sellers capitulating, lenders that have provided extensions to strained borrowers over the past couple of years could help break a bid-ask logjam and fuel more sales, suggested David Welk, managing director of Origin Investments, a sponsor of multifamily funds and Delaware Statutory Trusts. That’s because some lenders have written down apartment loans in an orderly manner over time and are in a better position to demand a paydown of the debt or sale of the property, he added.

Origin has completed three acquisitions over the last year in off-market or lightly marketed transactions. In May, it paid $91.5 million for Broadstone Optimist Park, a two-year-old, 323-unit apartment complex in Charlotte, N.C., that sits between two entertainment districts and near a light rail station and an urban trail. Origin renamed the project Charlotte NoDa, and Welk estimated that it would cost around $105 million to build a similar property today.

“What we’re looking for is relative value, and we felt good about the basis of that purchase,” he said. “It was built by one of the best merchant builders in the region, it’s an infill location, it’s close to transit and there’s a lot of retail going up around it that’s joining good existing retail. Those elements make sense for a long-term hold.”

Despite some submarket supply concerns with 1,500 to 2,000 units coming online in the near future, Origin is forecasting average annual rent growth of 5.1 percent over the next five years based on a proprietary artificial intelligence tool the firm developed to inform investment decisions. Units renting for less than $1,700 at Charlotte NoDa should revert to a submarket mean of $2,000 over time, Welk noted.

A bottom bet

Platte Canyon Capital, an investment firm launched by multifamily veterans in January, is taking a similarly contrarian view in Salt Lake City, Denver, Dallas, San Antonio and Austin, Texas. Those markets have experienced a boom-to-bust rent movement to varying degrees, typically amid oversupply, and the firm is looking for sellers facing capital stack distress, reported Brennen Degner, co-founder & CEO of Platte Canyon Capital. That means, after paying peak prices for apartment assets a few years ago, borrowers want to extricate themselves from deals rather than wait years to recover lost value.

In July, the firm joined with an L.A.-based institutional investor for its first acquisition, a garden-style community in San Antonio. The property initially opened in 1984 with 116 units and another 152 units were added in 2017. Degner declined to reveal the purchase price but estimated it at a third of replacement cost.

Whether pursuing a vintage or newer asset, the key is investing at a basis supported by the current fundamentals, he said. At the company’s San Antonio property, low rental rates should help maintain the asset’s competitive edge, along with nearly $5 million geared toward interior upgrades, the installation of in-unit washers and dryers, amenity enhancements and exterior improvements.

“The supply story has impacted everything from A- to C-quality assets, so there could be some volatility in the short term. But as markets get closer to equilibrium and rents grow moderately again, we’re in good shape. If they outperform, that’s gravy.”