Moody’s Update: Population Shifts Shape Housing Demand

How migration trends influenced the multifamily market last year. Read the report.

In 2024, the multifamily housing market experienced substantial inventory growth, adding nearly 300,000 units in 79 major metros tracked by Moody’s, representing one of the highest construction booms on record. This expansion led to slight imbalance between supply and demand, raising the national vacancy rate by 10 basis points each quarter throughout the second half of the year and closing 2024 at 6.1 percent by the fourth quarter of 2024—the highest level since 2011.

Despite rising vacancy, the sector achieved 0.7 percent growth in national asking rent over the year to $1,850, nearly reaching its peak in the third quarter of 2023. Looking ahead, it is anticipated that an additional 15 percent of units will be added to the total investible universe across the US.

READ ALSO: Will the Rental-to-Condo Conversions Trend in South Florida Last?

Demographic factors are crucial. They shape housing demand, suppress the frictional oversupply, and support positive rent growth. Rapid population growth, a resilient labor market, and strong wage growth last year were woven into the demand story. Meanwhile, limited trade-up options among potential first-time homebuyers over the past few quarters left renting an obvious alternative for many. Over 15 percent more units were absorbed compared to last year, equivalent to 57 percent more than the sector’s long-term average from 2000 to 2019.

The US Census Vintage 2024 estimates indicate that the nation’s population reached 340.1 million, the fastest annual growth observed since 2001 with a nearly 1 percent increase between 2023 and 2024. A rapid rebound in immigration is a major driver of this, while the natural increase (natural birth minus death) stayed below historical average.

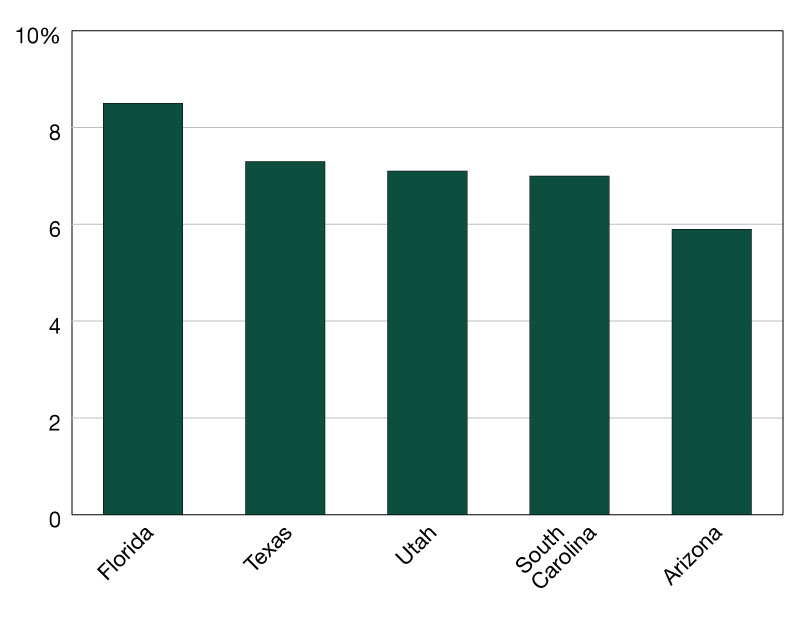

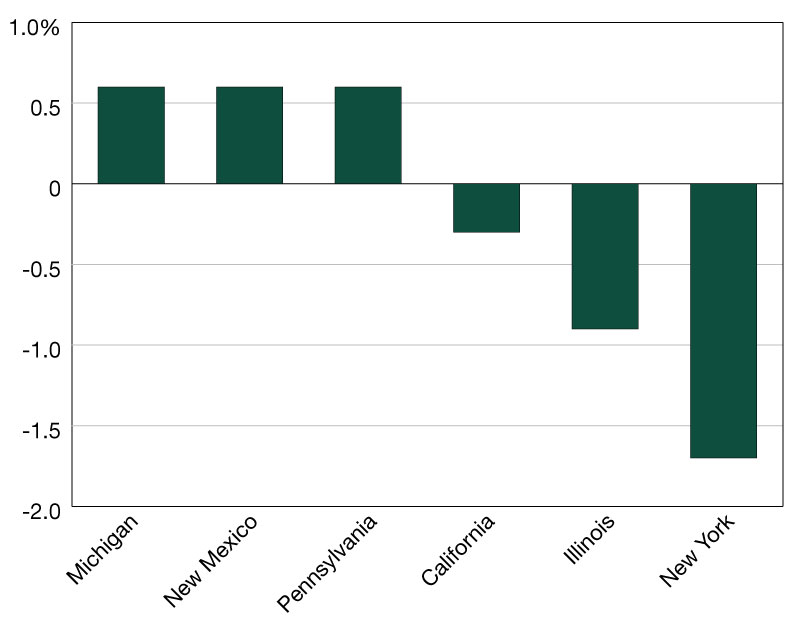

Regionally, the South experienced the most substantial population gains from April 2020 to July 2024, driven by states like Florida that grew by 8.5 percent (1,834,023) and Texas by 7.3 percent (2,141,373). Although Florida benefited from immigration, though, it saw smaller gains from domestic migration. Conversely, the Midwest and Northeast saw comparatively lower growth, with New York experiencing the most significant decline (-1.7 percent or 336,524) from outmigration.

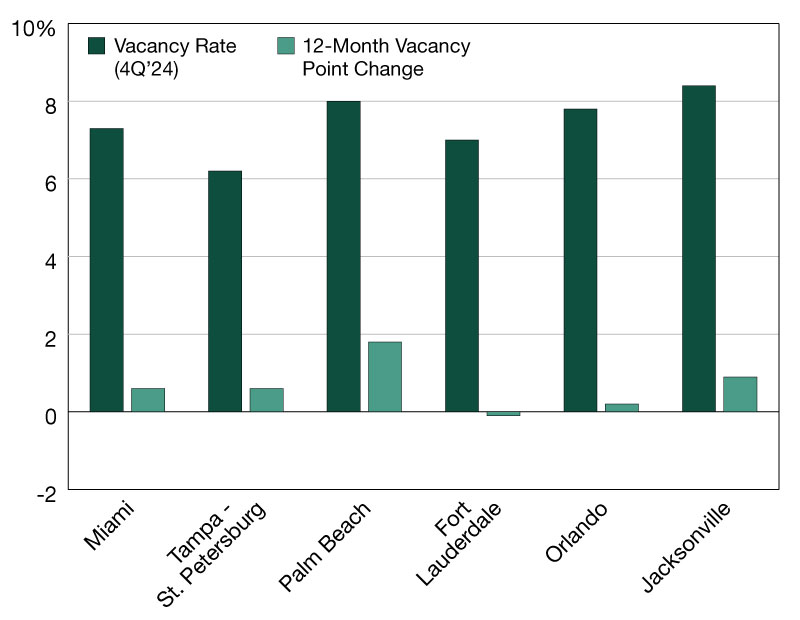

Florida’s significant population growth had varying impacts on the rental markets across the state’s metro areas. Miami, although its vacancy rate is above the national average, stood out with a substantial 12-month asking rent growth of 4.7 percent and an effective rent growth of 4.6 percent. This reflects the metro’s strong rental housing demand fueled by the influx of new residents attracted to the area’s economic opportunities and amenities.

Tampa-St Petersburg avoided major hurricanes and demonstrated stability by maintaining an unemployment rate below the national average, aided by the rapid recovery of its hospitality sector. The metro has a relatively low vacancy rate and a 1.9 percent increase in asking rents. Orlando’s modest rent growth and vacancy changes reflect steady demand influenced by a robust job market, particularly in tourism and professional services, with a vacancy rate of 7.8 percent, indicating potential for improvement.

On the other end, Jacksonville held the highest vacancy rate among the Florida metros along with declining rent growth, suggesting an imbalance of supply and economic challenges that are not aligned with the population rise. Palm Beach and Fort Lauderdale experienced moderate rent growth and vacancy changes, showing steady but less dramatic impacts from population growth. Demographic shifts, particularly population increases driven by immigration impacted the rental demand. Regional performance variations in Florida’s metros highlight diverse responses to population changes, highlighting the importance of understanding local conditions and their demographic trends.

—Posted on January 29, 2025