Moody’s Update: Excess Supply in the Multifamily Housing Sector

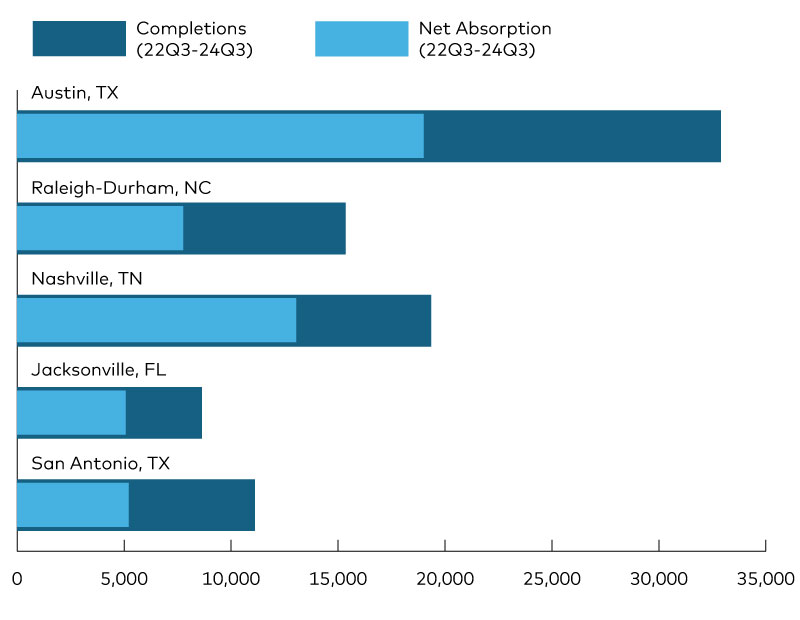

The top 5 most oversupplied multifamily markets, according to Moody's Analytics. Read the report.

In the third quarter, the multifamily housing sector continued to endure supply-side challenges, with vacancy rates climbing from 5.3 percent this time last year to 5.8 percent for Q3 2024, the highest recorded since 2011. The ongoing development of new apartment units buoyed the rent level, with the national asking rent reaching $1,845. However, as demand slowly catches up with the glut of new units, the market has been experiencing frictional excess supply, which put downward pressure on revenue growth through higher vacancy rates and lower (if not negative) rent growth.

READ ALSO: National Multifamily Report – September 2024

Excess supply is defined as total completions less net absorption over the past 24 months, overlapping the deceleration and stabilization period in the recent multifamily market cycle. When expressed as a percentage of each metro’s inventory, excess supply can be compared across metros by controlling for size effects. When excess supply is negative, it can be interpreted as excess demand —net absorption outpacing total completions. Moody’s CRE data shows that out of the 82 primary multifamily metros, Austin was the most oversupplied, with an excess supply to inventory ratio of 4.8 percent, followed by Raleigh-Durham at 4.4 percent and Nashville at 3.9 percent. Meanwhile, Columbia exhibited the highest excess demand at -1.0 percent.

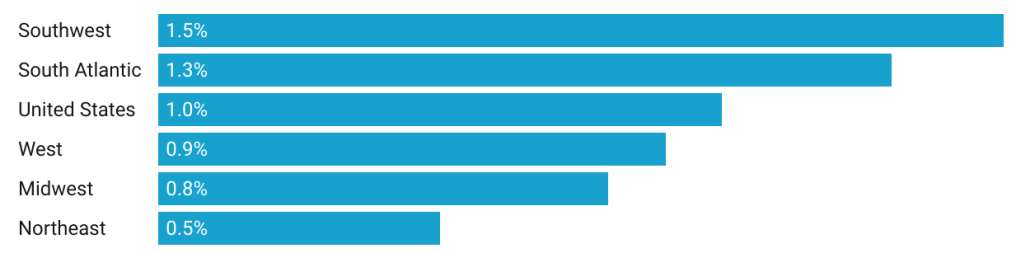

Although excess supply varies by metro, the above chart illustrates regional level trends. The Southwest region topped the list with the highest excess supply as a percentage of inventory at 1.5 percent, while the Northeast had the lowest at 0.5 percent. The national average was at 1.0 percent. This observation aligns with the first table, where three of the top five metros with the greatest excess supply fall into the South Atlantic region, while the Southwest accounts for the remaining two. High investment returns, low interest rates, and strong demographic tailwinds for the Southwest and South Atlantic regions from late 2021 to early 2022 fueled their recent inventory growth, but normalization of demand in recent years led to the current excess supply.