Los Angeles Multifamily Report – November 2024

Some key metrics are up year-over-year.

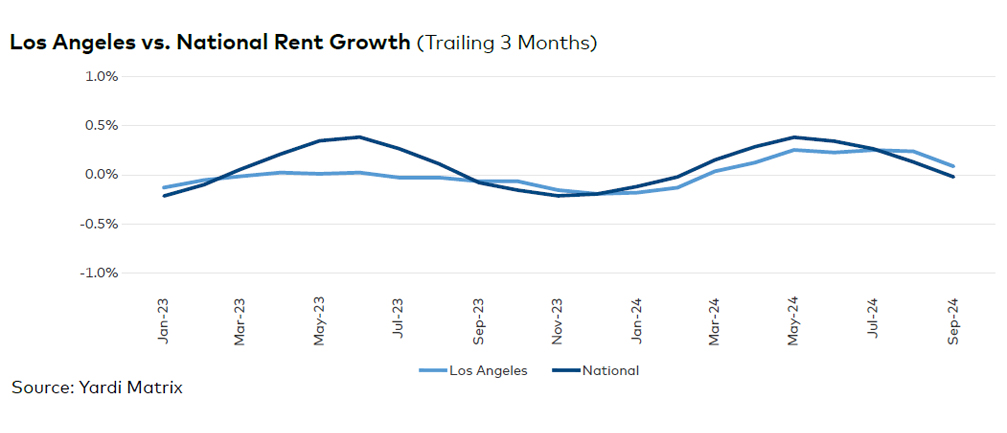

Los Angeles posted steady multifamily fundamentals at the end of the third quarter. Average advertised asking rents rose 0.1 percent on a trailing three-month basis through September, to $2,634, moderating in line with the seasonal trend, while the U.S. rate remained flat, at $1,750. Rent in the metro was also up 0.5 percent year-over-year, while the national figure was 0.9 percent. Demand remained robust, as evidenced by the occupancy rate in stabilized properties, which rose 10 basis points, year-over-year through September, to a solid 96.1 percent.

In the 12 months ending in July, the employment market in Los Angeles expanded 0.8 percent, 50 basis points behind the national rate. Only two sectors lost jobs—professional and business services (-5,500 jobs) and manufacturing (-2,900 jobs). Gains were led by education and health services (45,600 jobs) and will continue to grow, with projects such as the $1.7 billion Harbor-UCLA Medical Center Replacement Program and UCLA Research Park expected to provide a boost. Meanwhile, unemployment rose to 6.7 percent in August, the highest level since 2021 and well behind the 4.2 percent national rate.

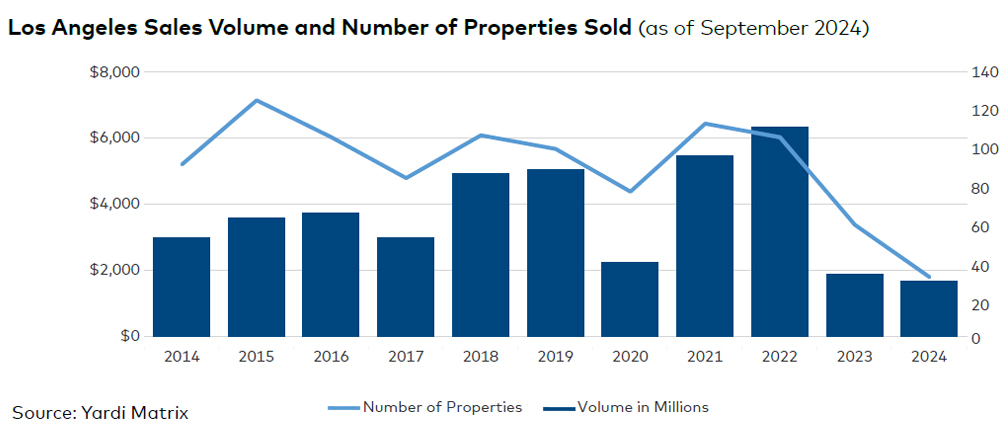

Deliveries totaled 5,956 units through September, and new construction remained well below the volume recorded last year. Still, nearly 31,000 units were underway. Investors traded $1.7 billion in multifamily assets during the first three quarters, for an average price per unit that increased 11.6 percent year-to-date, to $367,043.