JOLTS Survey Indicates Trouble in Job Market

Underneath the surface, troubling signs of structural unemployment lurk. The labor force participation rate has yet to show any signs of rebounding during the recovery.

Headline employment numbers indicate a healthy labor market, but the Job Openings and Labor Turnover Survey paints a much different picture.

Headline employment numbers indicate a healthy labor market, but the Job Openings and Labor Turnover Survey paints a much different picture.

Unemployment numbers for the month of July were welcomed with headlines proclaiming the solid growth of the labor market, and in many respects the labor market in the United States has never looked better. Unemployment rates, from the traditionally cited U-3 through the broadest measure of U-6, are at lows not seen in more than a decade. Weekly initial unemployment claims are at their lowest levels since the early 1970s, a time in which the labor market was nearly half of the size that it is today.

Yet underneath the surface, troubling signs of structural unemployment lurk. The labor force participation rate, for one, has yet to show any signs of rebounding during the recovery. Beginning during the Great Recession and steadily declining for the half decade thereafter, the labor force participation rate has settled in a range between 62.5 and 63 percent for the last few years. Some of the decline in participation is undoubtedly being driven by an aging workforce, but not all of the five percentage point drop since the Great Recession can be attributed to retiring baby boomers.

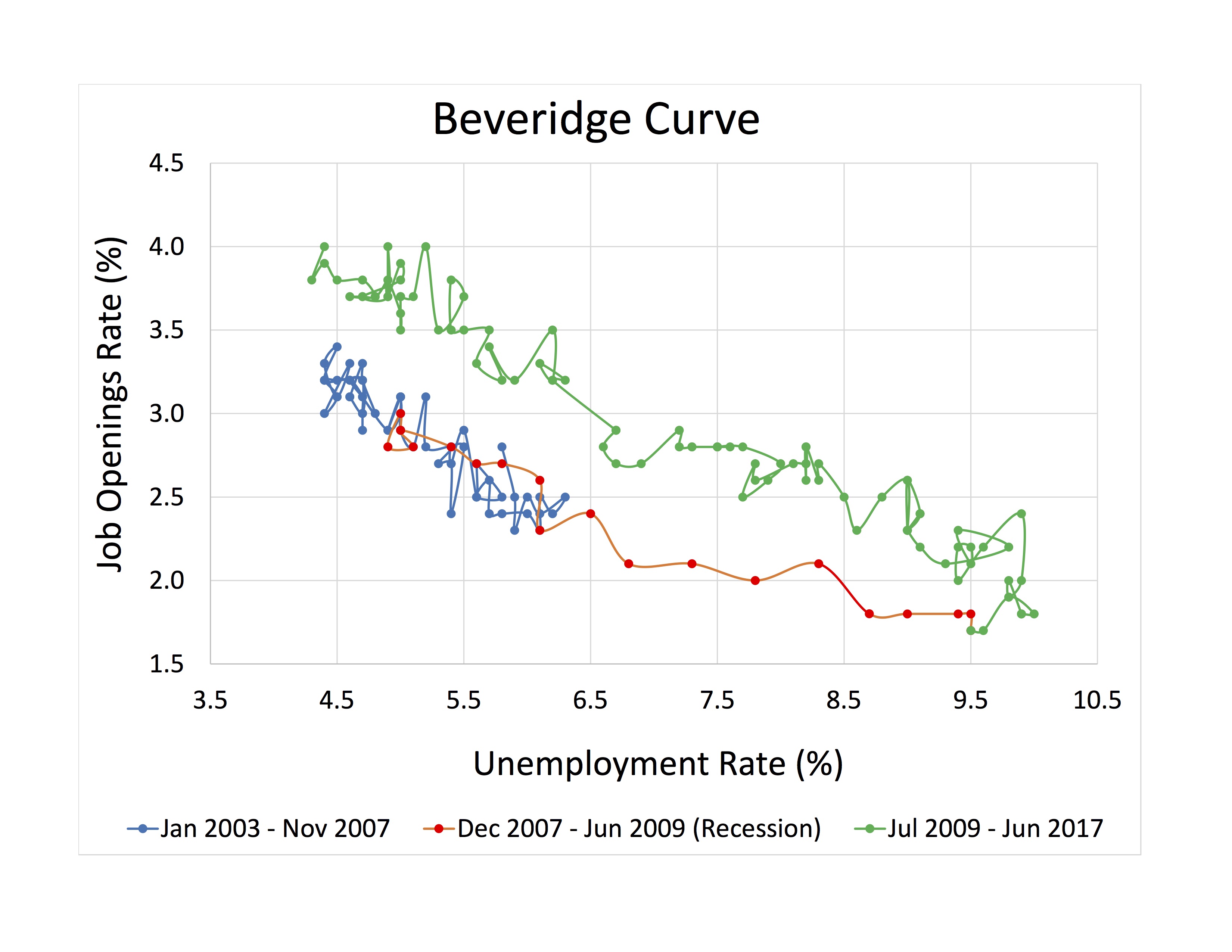

More disconcerting are the numbers that come from the Job Openings and Labor Turnover Survey (JOLTS). The survey measures hires, job openings, separations, quits and layoffs from the demand side, surveying establishments to gage labor shortages. It is said that JOLTS are one of Federal Reserve Chair Janet Yellen’s favorite labor market statistics, yet the release largely gets overlooked in the press. As we move further and further into what economist consider full employment, alternative indicators like JOLTS will become vital to assessing the condition of the labor market. One useful instrument to gauge the health of the labor market is the Beveridge Curve, which graphs the relationship between the unemployment rate and the jobs opening rate. The curve demonstrates that as the unemployment rate increases the job openings rates falls, and vice versa. It is graphed with the unemployment rate on the horizontal axis and the opening rate on the vertical and a curve that moves outward, where a given rate of unemployment is associated with a higher level of job openings, indicates a more inefficient labor market than a curve closer to the axes. Since the onset of the Great Recession, the Beveridge curve has seen a significant outward shift, indicating a skills mismatch in the labor force.

A further concern raised by the JOLTS numbers is that job openings are outpacing hires, a recent trend that only began in 2015. Understanding the different methods in which hires and openings are counted explains why the imbalance between the two could be such a massive problem.

For a job to be counted as an opening the company surveyed must be actively recruiting, the position could start within the next 30 days should they find a suitable candidate and it must be open on the last business day of the month. If a job is posted on the first Monday of the month and the position is filled by the third then it does not appear as an opening in the data.

On the other hand, for a hire to be counted, it can be any hire that was made during the month for any length of time. A teenage employee that gets hired at a fast food restaurant and performs so poorly that he is fired on his first day on the job will still nonetheless be counted in hires. Hires are also counted if they are short-term, seasonal, on-call or intermittent.

These different methodologies explain why hires had outpaced openings for so long. In general, hires uses a much more broad definition, measuring flows of workers whereas openings measures the stock of open jobs within a given point at the end of the month.

When digging deeper into the JOLTS data by industry, it is evident that while this issue rears its head in a few sectors of the economy, it is mostly being driven by a skills gap in Health Care and Social assistance sector where in July job openings outpaced hires more than two to one. In June, there were 1.135 million job openings and only 561,000 hires. It is important to note that this is one sector where openings outpacing hires has been the norm since the BLS began the JOLTS survey at the beginning of the millennium. This makes intuitive sense; because jobs in this sector generally require more training and skills than most others, hiring an employee requires more searching and there is more competition for potential employees. Nevertheless, the magnitude of the gap between hires and openings in the health care and social assistance sector is unprecedented. The difference between openings and hires had never crossed the threshold of 400,000 before 2015 but has done so every month since.

Because JOLTS is a survey of establishments and not households, we can see only one side of the coin when it comes to a skills mismatch. We cannot use this data to understand where the supply side imbalances in the labor market are located, but the best guess would be in retail positions that are disappearing by the day. Retailers face an economy in flux, where e-commerce and shifts in consumer behavior are forcing many chains to go out of business and retail employees are getting left behind as a result. Typically retail employees have low levels of skills and education, so if this is the case then the skills imbalance in the labor market could be the new normal.

Most Recent