Dallas Multifamily Report – November 2024

There's demand, but there's also a lot of new stock across this city.

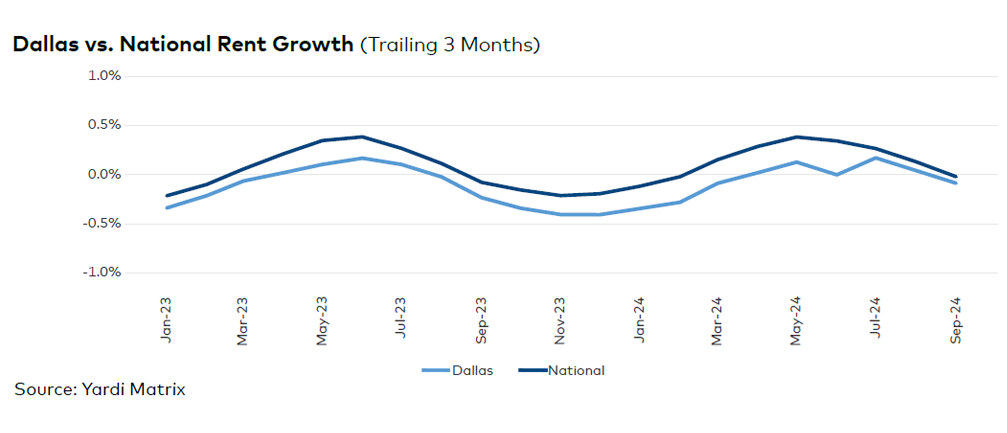

Dallas-Fort Worth multifamily fundamentals remained slow but steady in 2024 through September, as absorption worked its way through high volumes of new supply. Unsurprisingly, advertised asking rents fell 0.1 percent on a trailing three-month basis through September, to $1,541, just as the seasonal slowdown began. Meanwhile, the national rate remained flat, on a three-month basis, at $1,750. Occupancy in stabilized Dallas properties also slid, down 40 basis points year-over-year, to 93.1 percent.

Employment growth continued to moderate, clocking in at 1.6 percent, but remained higher than the 1.3 percent U.S. average. Two sectors lost 12,300 jobs combined in the 12 months ending in July—professional and business services and information. Meanwhile, the bulk of the 57,100 net jobs added came from the government (15,100 jobs) and education and health services (14,100 jobs) sectors. DFW’s unemployment rate stood at 3.9 percent in September, according to preliminary data from the Bureau of Labor Statistics. That was slightly above Texas’ rate and the national figure (both at 4.1 percent). Notable projects underway include the $2.5 billion The Central and the $1 billion redevelopment of Collin Creek Mall.

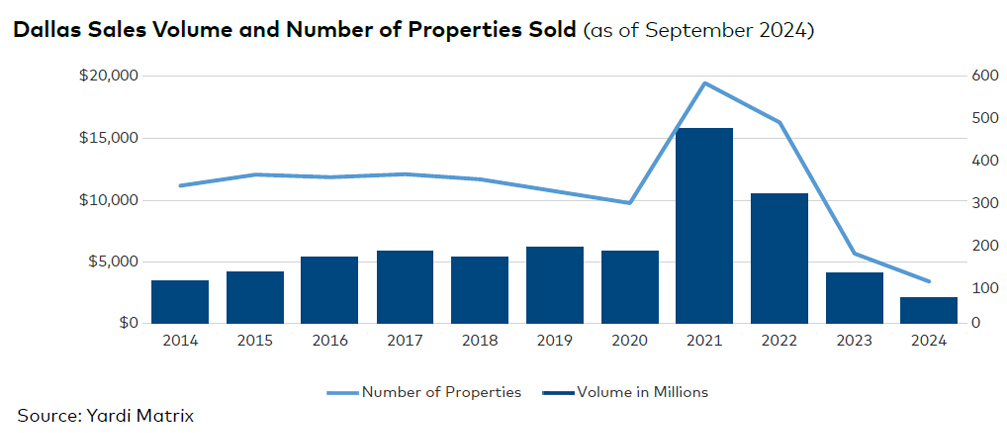

Developers delivered 20,481 units in 2024’s first three quarters, with another 62,211 apartments underway. Investment remained limited, at just $2.1 billion year-to-date through September, for a price per unit that remained virtually flat compared to 2023.