National Student Housing Report – May 2026

Preleasing remains ahead of last year’s pace, according to the latest Yardi Matrix data.

Preleasing at Yardi 200 universities reached an estimated 71.6 percent in April for the 2026-2027 academic year, up 200 basis points from March, according to the latest Yardi Matrix student housing report. While leasing remains ahead of last year’s pace, operators have reported a more competitive environment due to increased new supply and softness in the conventional multifamily sector.

April preleasing trailed the levels recorded during the same period in 2022, 2023 and 2024, reflecting a slower leasing cycle than the market experienced during the post-pandemic surge. Preleasing growth increased 7.6 percent month-over-month in April, below the 8.6 percent average monthly gain recorded between January and March. Despite the slower pace, student housing occupancy remains on track for another strong year.

The student housing report noted that same-store rent growth was just 0.4 percent in April, suggesting that much of the increase in asking rents is being driven by leased-up properties rather than broad-based pricing gains across the sector. Nevertheless, the recent improvement may indicate that operators are regaining confidence in pricing as the summer leasing season approaches.

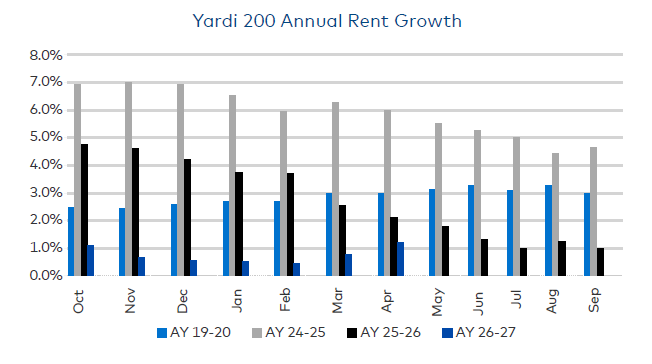

Several markets continued to post strong rent performance, despite broader deceleration trends. Utah State University recorded 7.8 percent annual rent growth in April, while James Madison University reached 7.6 percent and Iowa State University posted 6.6 percent growth. Meanwhile, some of the markets that experienced steep rent declines earlier this year showed signs of stabilization, including Northern Arizona, Baylor University and the University of Tennessee.

Some student housing markets near full occupancy

Several universities are already approaching last year’s final occupancy levels. Among markets with at least five reporting properties, Virginia Tech led the nation at 97.2 percent preleased, followed by the University of Missouri at 93.7 percent, Western Carolina at 93.3 percent, Penn State at 92.7 percent and James Madison University at 91.3 percent. Clemson University, Northern Arizona University and the University of Cincinnati were all within four percentage points of their fall 2025 occupancy levels.

The University of Cincinnati posted one of the strongest year-over-year improvements in preleasing, alongside Northern Arizona, the University of Iowa, the University of Nebraska and Clemson. Several of these schools are already nearing last year’s occupancy despite recording lower occupancy rates than many peer institutions in 2025.

At the other end of the spectrum, some markets continue to face leasing challenges. Houston, UT-Arlington, Cornell University, Sam Houston State University and UC Berkeley reported some of the lowest preleasing levels in April, all remaining well below the national average. Several large universities with substantial construction pipelines, including North Carolina State, the University of Tennessee, the University of Central Florida, Arizona State University and Purdue University, also trailed last year’s pace.

The average advertised rent per bed across Yardi 200 universities reached $931 in April, up 1.2 percent year-over-year. While rent growth remains below the levels recorded during the previous three leasing seasons, April marked the second consecutive month of acceleration, after growth increased from 0.4 percent in February to 0.8 percent in March and 1.2 percent in April.