Is a Distressed Sales Wave on the Horizon?

With $806 billion in multifamily debt maturing by 2028, apartment property owners find themselves in the same predicament as office owners.

Declining demand for office space amid rising interest rates resulted in lower valuations and a surge in forced or distressed sales in this sector when many borrowers lacked the ability to refinance maturing mortgages. Now, the same circumstances are impacting multifamily debt despite this asset class’s generally high demand and tight occupancy.

Multifamily property values have declined roughly 28 percent below their 2022 peak and 4 percent year-over-year in 2025, according to John Neal Manning, senior managing director at Greysteel.

Unlike the office sector, multifamily is not facing a structural crisis. Rather, multifamily distress is primarily financial and cyclical, driven by the collision of peak-valuation debt maturities, elevated interest rates and a temporary oversupply in certain markets, he pointed out.

“The maturity in multifamily is less about ‘nobody wants the asset’ and more about refinance math not penciling at today’s rates, especially for loans originated in 2021 and 2022 with tight spreads, interest-only structures and floating-rate exposure,” commented Josh Bodin, senior vice president for capital markets strategy and trading at Berkadia.

LIKE THIS CONTENT? Subscribe to MHN’s Finance & Investment Newsletter

While multifamily hasn’t experienced the same valuation collapse as office, fundamental stress is showing up as a large share of owners come off of short-term bridge debt into a much higher rate environment. This has created refinancing gaps that force deleveraging, said Brian Connolly, founder & CEO of Feasibly Inc., a firm that offers bank-ready feasibility studies for real estate projects. “So while it won’t mirror office-level distress, we are seeing a meaningful rise in transaction-driven distress tied to debt, not occupancy.”

Over the last three years, both office and multifamily lenders have “extended and pretended,” hoping the Fed would lower interest rates to a level that makes refinancing feasible without an injection of significant equity. Since that has not come to pass, the amount of forced or distressed multifamily sales is rising as lenders lose patience.

The end of extend and pretend

According to a report from credIQ, multifamily overall delinquency reached 1.37 percent as of the third quarter of 2025, representing a 12-year high—the highest since the post-Great Financial Crisis recovery era and a dramatic escalation from the near-zero stress environment of 2021–2022.

Approximately $806 billion in multifamily debt will mature between 2026 and 2028—about $300 billion this year, according to Dave Boros, vice president of capital markets and student housing at NMHC, who noted that across the board of major lending groups, banks and debt funds are the largest holders of this debt.

“During a super low interest rate environment of 2021-2022, we had a lot of transactional activity—a lot of stuff was purchased with the idea of increasing rents, or doing minor upgrades, thinking that could dramatically increase rents,” Boros continued. “That did not necessarily materialize. And on top of that, interest rates went up.”

Rising costs amid stagnant or declining rents

Adding to the havoc around maturing debt and related delinquencies are increasing operational costs amid a surge in new apartment deliveries and encroaching government restrictions on rent growth.

The greatest delinquencies are specific to overbuilt Sun Belt markets such as Austin, Texas, and Phoenix, where there is stress from flat or declining rent growth, as well as in markets like New York City, where rent growth is regulated by rent caps, Connolly noted. “Rent-stabilized portfolios there are showing distress levels of around 11 percent as expenses outpace allowable increases,” he said.

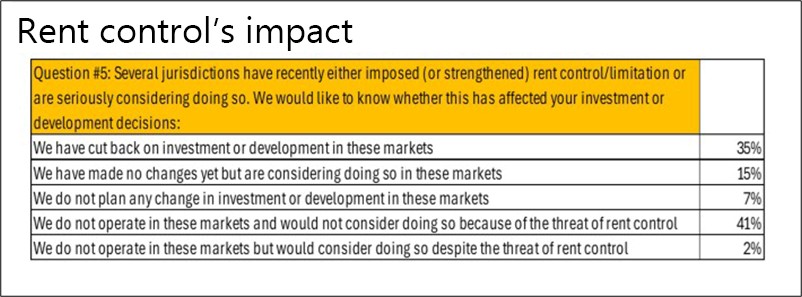

Rent controls, Boros suggested, not only put a damper on people’s interest in investing in those markets but also encourage landlords to raise rents, even when operational costs remain unchanged. In a recent survey of apartment conditions, 91 percent of NMHC members said that they’re cutting back or not going to invest in those markets because of the threat of rent control.

He noted, for example, that implementation of onerous rent controls in Washington, D.C., and Maryland’s Montgomery and Prince George’s counties has resulted in a dramatic decrease in applications for multifamily development. Prior to rent control, there were 821, 603 and 656 building permits issued for multifamily projects in Montgomery County in 2022, 2023 and 2024, respectively. With the implementation of rent control in 2025, multifamily building permits fell to just 7, Boros said.

If you have an annual cap, like 3 percent, landlords are likely to raise rents to the maximum each year, whether or not their expenses increase, Boros continued. This is because the cost to operate the property could go up next year beyond the allowable rental rate increase due to a new property tax law or something else, like an increase in insurance. Now the higher expenses may exceed rent collected, potentially affecting the landlord’s ability to pay for property repairs or the mortgage, he noted.

Values declining in overbuilt markets

The flood of new apartment deliveries in some markets is contributing to an increase in delinquencies and forced or distressed sales. “Value declines are most pronounced in pandemic-era high-growth markets like Austin, Tampa and Phoenix, where a surge of new supply has eroded pricing power,” said Connolly, noting that in these markets, appraisal values are often coming in below loan balances, forcing owners to inject capital to refinance.

Distressed opportunities are also emerging in the Sun Belt and in high-regulation states like California. “The common thread is a combination of elevated operating costs—insurance and labor, in particular—and expiring rate caps, which pushed otherwise stable assets into forced-sale situations, where debt costs exceed property income,” he pointed out.

The vintage of the asset seems to be more of a factor on valuations than location, suggested Shlomi Ronen, founder & managing principal of Dekel Capital. He noted that 1970s and ‘80s vintage properties are generally out of favor with investors, which is driving cap rate expansion of those assets.

Distressed multifamily sales inevitable

Multifamily distress is likely to present in pockets, not as a “panic and collapse” scenario, said Bodin, noting that demand for housing remains strong, which keeps properties operating even when capital structures are stressed. There’s a deep refinance ecosystem—agencies, banks, life companies and private credit that are still active in multifamily, he noted.

Lenders are more willing to work with multifamily than office borrowers because the collateral is generally financeable and sellable, Bodin suggested, noting that as a result, the system tends to push toward extensions and recapitalizations, not immediate liquidation. “That matters because it creates options: refinance, extend, partial paydown, pref. equity (issuance of preferred equity shares), or recap (recapitalization), instead of a forced sale at any price.”

While investors are likely to see a significant amount of multifamily distressed opportunities, Manning contended that they would look different than office distress. “Rather than empty buildings being handed back to lenders at pennies on the dollar, multifamily distress is manifesting as ‘rescue capital’ opportunities (preferred equity injections) and forced sales where sponsors simply run out of time to refinance,” he said. “We are seeing a marked increase in properties being sent to special servicing or sold at or below their loan balances, particularly among syndicators who relied heavily on floating-rate debt.”

Unlike distress in the office market, Bodin pointed out that opportunities in multifamily distress will come from situations where the multifamily refinance wall meets a second problem, such as:

- Floating-rate bridge loans where debt service reset is higher and DSCR (Debt Service Coverage Ratio) collapsed below 1.0, the minimum indicator of positive cash flow (Lenders usually require a DSCR between 1.25 and 1.5)

- Deals underwritten to aggressive rent growth that didn’t materialize or where expenses surged

- Oversupplied submarkets where lease-up risk or concessions pressure NOI

- Properties with near-term capex needs and no clean takeout or

- Sponsors who can’t or won’t write a check to pay down to new proceeds.

“What makes 2026 particularly important is that this wall grew meaningfully as borrowers exercised extension options over the past two years, effectively pushing maturities forward into a tighter rate and underwriting environment,” Bodin explained. “Multifamily is at the center of the maturity discussion because the volume of debt coming due is large enough that refinancing capacity, structure and proceeds will matter deal-by-deal.”

Delinquency accelerating in CMBS Debt

Refi issues show up more quickly in CMBS than the traditional lending market due to more watchlist activity, special servicing, and loan-level resolutions, especially where proceeds come up short or the capital stack is floating-rate, Bodin noted.

CMBS multifamily delinquency rates surged, reaching between 6.85 percent and 7.47 percent in early 2026, with the special servicing rate climbing above 8.14 percent, according to Manning. “This is a stark increase from the historically low rates seen just a few years ago, driven largely by floating-rate loans hitting their maturity dates without viable takeout financing,” he said.

Meanwhile, banks, driven by regulatory pressures (such as the Basel III Endgame) and a desire to reduce overall commercial real estate exposure on their balance sheets, are aggressively tightening loan criteria. Manning noted that they are lowering maximum loan-to-value and increasing DSCR requirements, effectively making it impossible for many transitional or slightly distressed assets to secure conventional bank financing.

Lenders lending with tighter underwriting

Fannie Mae and Freddie Mac, Bodin said, also have tightened DSCR requirements, effectively forcing borrowers to bring more equity to the table to refinance.

“Conventional multifamily lending—especially the agencies—remains open for business, and that steady liquidity is a big reason multifamily is working through maturities deal-by-deal, rather than through a disorderly reset,” Bodin continued, suggesting that the difference is in execution.

“Today’s refinancings are underwritten to today’s rents, expenses and debt costs, which can mean lower proceeds and more structure—paydowns, reserves, or a recap in finance that restructures the company’s capital mix, typically by exchanging debt for equity or vice versa, to stabilize finances, fund growth, or take profits,” Bodin continued, noting that this may involve strategies, such as issuing debt to pay a dividend or buying back shares.

In this period of surging mortgage maturities, bridge lenders, or debt funds, and other alternative lenders are filling a very specific role: helping borrowers bridge to stabilization, execution certainty or an eventual agency or balance‑sheet take‑out, noted Bodin. “As long as exit paths remain viable and liquidity remains abundant, there’s little incentive for lenders to materially pull back.”

READ ALSO: Multifamily Lending Light in Sight

Boros said that debt fund lenders also are engaged in lending situations where a new construction loan is maturing or an existing asset is being repositioned but not far enough along for a life company or a government-sponsored enterprise takeout, like Freddie or Fannie.

He emphasized, however, that debt funds are being pretty disciplined in their underwriting, a reflection of the increase in lower-quality applicants over the last six months. As a result they have tightened loan spreads to 200 to 300 over SOFR (secured overnight financing rate) compared to 350 to 400-plus over SOFR a year ago.

“Bridge and private lenders have shifted from ‘extend and pretend’ to requiring fresh capital, especially for borrowers seeking refinances or extensions,” said Connolly. “Underwriting is materially tighter because lenders are anchoring to in-place cash flow rather than forward rent growth assumptions, which reduces proceeds and increases borrower equity needs.”

Meanwhile, Bodin contended that no broad tightening of criteria in the bridge or private credit market is expected, as the amount of liquidity behind these strategies remains substantial and continues to shape lender behavior. “While deal volume has surged as owners work through maturities and capital needs, it’s been met by a parallel influx of private credit capital and bank warehouse capacity, which keeps lending conditions competitive.”

Manning noted, however, that bridge lenders are enforcing strict debt yield floors, often starting at 7 percent to ensure the property can carry the debt, though spreads remain wide, typically SOFR + 450 to 850 bsp, resulting in all-in rates of 8.50 percent to 12.50 percent.

He also pointed out that bridge lenders are aware of execution risk and are requiring a clear, mathematically sound exit strategy (usually a path to permanent agency or CMBS debt) before extending a bridge loan. “If a borrower cannot prove they will meet permanent financing DSCR requirements post-renovation or lease-up, the bridge lender will not fund the deal,” Manning said.