National Multifamily Report – October 2025

Advertised rental decline visibile across majority of top 30 US markets, according to Yardi Matrix.

The U.S. multifamily market’s cooling continued, according to Yardi Matrix’s latest survey of 140 markets. The average advertised asking rents contracted, falling $4 to $1,743 in October, marking the third consecutive monthly decrease, although year-over-year growth remained flat at 0.5 percent. This also represented the third straight October bearing a similar rental moderation. The build-to-rent sector mirrored multifamily trends as advertised rates declined $6 to $2,195.

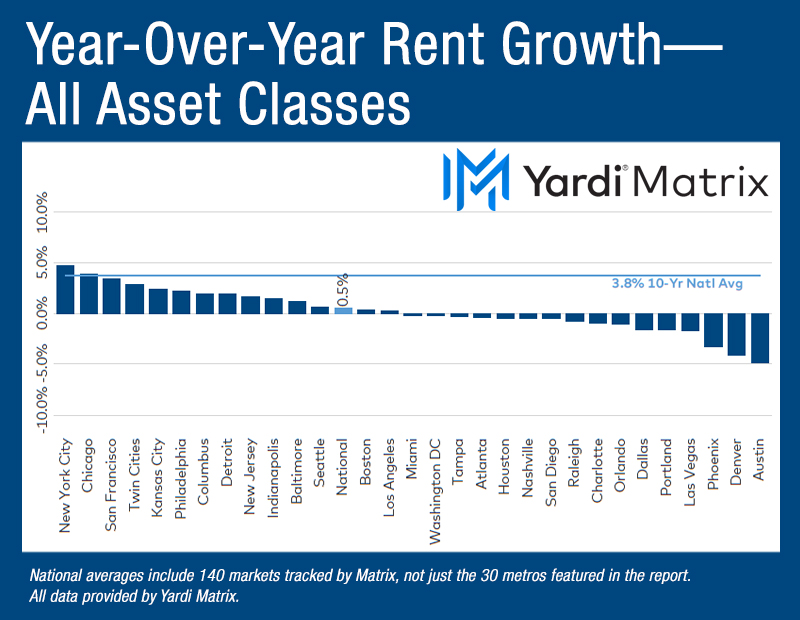

Metros with negative yearly rent growth held a thin majority among Yardi Matrix’s top 30 markets. Gateway and Midwestern metros performed well, with New York breaking into the lead at a 4.7 percent growth, trailed by Chicago (3.9 percent), San Francisco (3.4 percent) and the Twin Cities (2.9 percent). Sun Belt and Western markets saw a slowdown, with Austin leading losses (-4.8 percent), followed by Denver (-4.1 percent), Phoenix (-3.3 percent) and Las Vegas (-1.7 percent). Occupancy rates eased 10 basis points month-over-month, falling to 94.7 percent in September. Yet, the rates are still 0.1 percent higher compared to the same period of last year.

Lifestyle rents stumble as absorption loses steam

Short term, advertised rents dropped almost all over the board, with just two markets recording gains in October. Nationally, the average rate declined 0.2 percent, though Lifestyle property rents fell a steeper 0.3 percent, as opposed to Renter-by-Necessity, which moderated just 0.1 percent. New Jersey and Detroit were the markets that witnessed positive growth, though by just a mere 0.1 percent, aided by an increase in RBN by 0.1 percent and 0.2 percent, respectively. Rents were down in New York (-1.7 percent), Austin (-1 percent), Raleigh, N.C., and Denver (-0.8 percent each).

Another metric showed signs of deceleration as absorption clocked in at 110,000 units across the nation in the third quarter, down from the average of 185,000 apartments recorded during the first two quarters. However, the figure isn’t bad by historical standards, and the decline does not present itself uniformly across the U.S., with the Midwest being hit the hardest and registering a 75 percent decline quarter-over-quarter, followed by the Southeast (55 percent decline), Southwest (43 percent), West (35 percent) and Northeast (29 percent). Pockets of smaller markets saw large absorption, such as Colorado Springs, Colo., which witnessed 8.2 percent of its stock absorbed year-to-date through September, and Savannah-Hilton Head, Ga., (8.1 percent), as well as Charleston, S.C. (7.7 percent).

Single-family build-to-rent advertised asking rents slid $6 to $2,195 in October, maintaining the same figure as last year. However, occupancy was strong, climbing 10 basis points year-over-year to 95.1 percent in September. Across the Matrix Top 30 metros, markets where rents grew had a slim majority, the exact reverse compared to multifamily. Strongest increases hailed from the Midwest, with Twin Cities and Chicago being the front runners (7.0 percent year-over-year each), followed by Grand Rapids, Mich. (5.4 percent), Columbus, Ohio (5.1 percent) and Kansas City, Mo. (4.2 percent).

Read the full Yardi Matrix multifamily real estate report.