Seattle Multifamily Report – February 2024

Despite macroeconomic headwinds, the market has stayed strong.

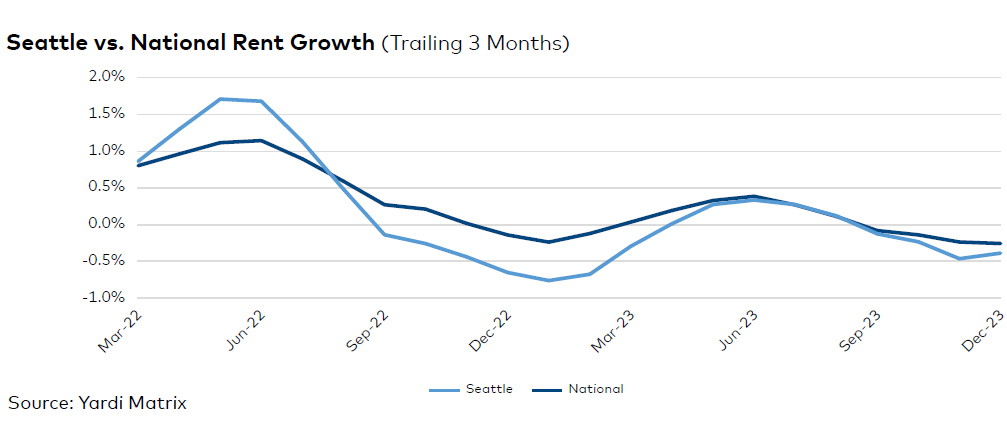

Seattle’s multifamily fundamentals were still relatively healthy at the end of 2023, following a challenging year. Rents declined 0.4 percent on a trailing three-month basis through December, lagging the U.S. rate by 10 basis points. Demand remained steady, as reflected by the occupancy rate in stabilized properties, which rose 0.2 percent in the 12 months ending in November, to 95.3 percent.

In the 12 months ending in October, Seattle employment expanded 2.8 percent, or 42,500 jobs, outperforming the 2.3 percent U.S. figure. Meanwhile, the unemployment rate rose to 4.0 percent in November, according to preliminary data from the Bureau of Labor Statistics, reaching the highest level in more than two years. The rate was on par with the state yet behind the 3.7 percent U.S. figure. Education and health services and leisure and hospitality led gains, adding 23,200 jobs combined. However, two sectors contracted—information lost 5,400 jobs and construction shed 1,500 positions. Amid a challenging period for tech at large, Seattle’s professional and business services sector gained 2,700 jobs.

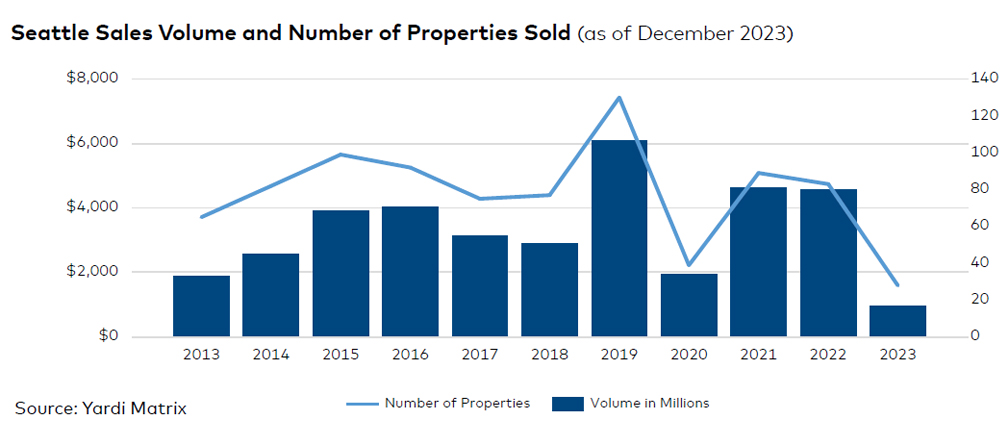

Developers delivered 7,463 units in 2023, which was the lowest volume since 2013 (6,589 units). The construction pipeline comprised 30,904 units underway in the third quarter, but posted a decline in the number of new construction starts. Meanwhile, investors remained cautious, trading less than $1 billion in 2023, marking the lowest annual volume of the past decade.