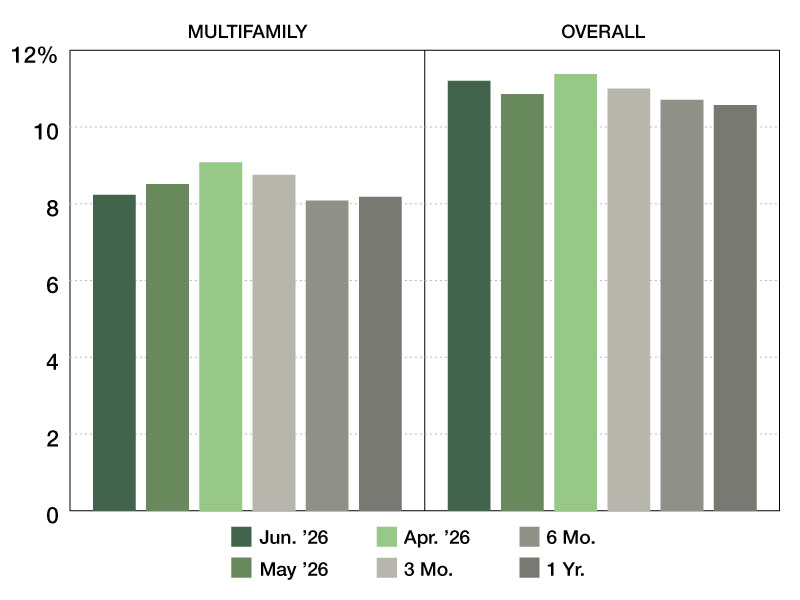

Freddie Mac Revises 2017 Outlook

In this video, the GSE concludes that, despite performance moderating from cycle highs, the U.S. multifamily market should remain healthy into 2018.

By Sanyu Kyeyune

Since the beginning of 2017, Freddie Mac has fine-tuned its multifamily performance forecast to reflect market shifts. In its recently released mid-year outlook, the multifamily housing finance provider predicted lower origination volume and more temperate vacancy rate increases. The company also offered that the remainder of 2017 should bring about more subdued absorption of new units—especially in cities with higher average asking rent—than in prior years. Here are some of the most notable findings, detailed also in a video featuring Vice President Steve Guggenmos and Manager Sara Hoffmann, both of Freddie Mac’s multifamily research and modeling department.

Although the multifamily market is expanding nationwide, the extent of this growth has been inconsistent across individual markets.

The multifamily market is poised for growth through 2017 and into 2018, though the degree of growth will vary across metros, depending on the rate of absorption of new deliveries. Nationwide, demand has kept pace with oncoming supply, helping to keep fundamentals strong. But, in areas with vacancy rates above historical averages, slower absorption is more likely, with the potential effect of disrupting fundamentals.

The upcoming construction peak will increase vacancies, albeit moderately, but the oncoming supply should align with demand in most areas.

Multifamily completions are set to peak toward the end of 2017 and in early 2018, with the onslaught of supply pushing vacancy rates upward. But, the rise in vacancies—which remain at historic lows in most markets—should occur more slowly than Freddie Mac predicted at the beginning of 2017. Positive trends in employment, demographics and lifestyle preferences continue to generate demand for multifamily rental units.

Most metros will end 2017 with vacancy rates below historical averages.

So far in 2017, Washington, D.C., San Francisco, New York and Miami have led the country in new completions, which, coupled with lagging demand, have compressed rent growth and pushed vacancy rates above their historical averages.

Most areas with vacancy rates that have trended toward their historical averages—such as Houston, Boston and Baltimore—will likely see rents rise, but at a slower pace than earlier in the cycle.

In cities where demand has typically exceeded supply—among them, Sacramento, Calif., Dallas and Raleigh, N.C.—rents have more room to keep growing. Unsurprisingly, nearly all of the cities projected to experience the highest gross income growth fall into this category, including Portland, Ore., Colorado Springs, Colo. and Nashville, Tenn.

At year-end 2017, after the supply influx has taken hold, the average vacancy rate will creep up to 4.7 percent, while employment growth will contribute to rent growth of 4.2 percent, as per Freddie Mac’s forecast.

Investors’ uncertainty has begun to dissipate, and the debt markets have responded with vigor.

The first half of 2017 saw many investors sitting on the sidelines and awaiting more clarity about the health of the economy. More recently, their confidence has resumed, and even though investor demand will continue responding to a strong market, it will likely be at lower levels than in the past few years. But, the sector still remains attractive: multifamily originations are set to achieve another record, reaching between $270-280 billion and representing a 3-5 percent year-over-year increase.

Video courtesy of Freddie Mac