Phoenix Multifamily Report – June 2023

After two great years, the market is now correcting course.

Phoenix rent evolution, click to enlarge

Phoenix’s robust stock expansion continues to impact rates and occupancy. The average rate posted the weakest performance among major U.S. markets, down 2.8 percent year-over-year through April, to $1,608. Meanwhile, the national figure decelerated to 3.2 percent, reaching $1,709. Occupancy slid 130 basis points in the 12 months ending in March, to 94.0 percent, with a larger decline in the Renter-by-Necessity segment.

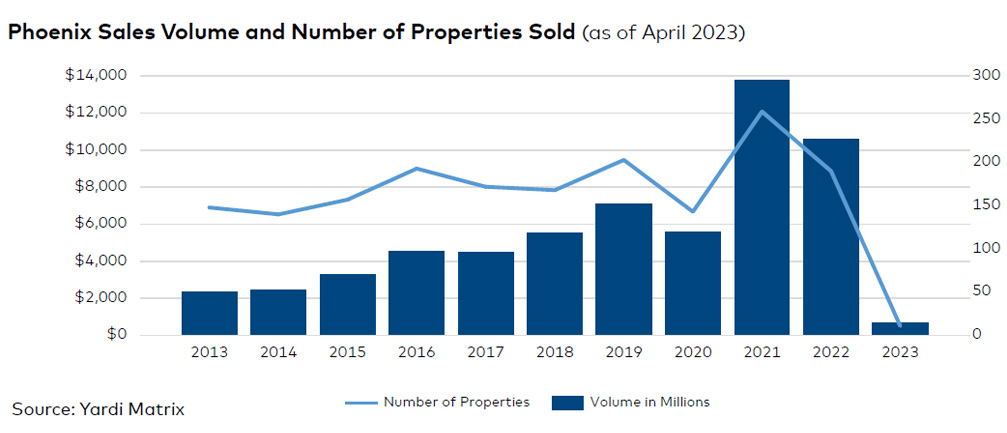

Phoenix sales volume and number of properties sold, click to enlarge

Unemployment stood at 2.9 percent in March, flat for four consecutive months, leading the state and U.S. figures, both at 3.5 percent. Employment grew by 3.1 percent, or 54,900 jobs, in the 12 months ending in February, with only trade, transportation and utilities contracting, down by 5,600 positions. Education and health services and leisure and hospitality led gains, and both are poised for continued growth. Moreover, Phoenix’s industrial market continues to expand. Notable planned and underway projects include LG Energy Solution’s $5.5 billion battery-manufacturing complex and KORE Power’s $1.3 billion gigafactory.

Phoenix. Photo by DutcherAerials/iStockphoto.com

Developers delivered 3,159 units this year through April and had an additional 33,201 units underway, with a substantial number of these slated for completion by year-end. Meanwhile, investment activity slowed, amounting to $667 million year-to-date through April, for a price per unit that slid 25 percent, to $241,227. However, the rate was still significantly above the $178,275 U.S. figure.