National Student Housing Report – April 2026

Preleasing remained ahead of last year’s final March estimate, but rent growth continued to decelerate, Yardi Matrix data shows.

Preleasing at Yardi 200 universities for the upcoming academic year reached 65.5 percent in March, according to the latest Yardi Matrix student housing report. The figure was 340 basis points ahead of the final estimate for March 2025 and on pace with March 2024. Early estimates are likely to be revised as more data is collected.

The average advertised rent per bed at Yardi 200 schools rose to $928 in March, up 0.8 percent year-over-year. That marked an improvement from 0.4 percent in February and 0.7 percent in January, but remained well below the 2.6 percent rent growth recorded in March 2025 and the 6.3 percent figure registered in March 2024.

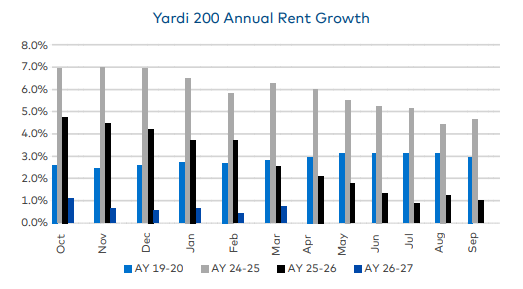

Since October, rent growth for the 2026-2027 leasing season has averaged 0.7 percent, compared with 2.6 percent during the prior leasing season and 5.9 percent during the 2024-2025 cycle.

Yardi Matrix also recently released historical and forecasted on-site enrollment data for the Yardi 200, excluding online-only students. The data shows that although total enrollment increased between 2019 and 2024, only primary state schools recorded on-site enrollment growth.

Preleasing data sends mixed signals

As of March, multiple universities remained well ahead of the Yardi 200 average. Virginia Tech led with 95.5 percent preleasing, followed by University of Missouri and James Madison University, both at 88.4 percent. Penn State followed at 87.3 percent, while Clemson University reached 85.2 percent.

On the other end, several schools were still well below the national average. Among universities with enough reported data points, Houston reached 28.1 percent preleasing, UT-Arlington stood at 28.9 percent, UNC-Greensboro at 40.2 percent, Sam Houston at 44.9 percent and North Texas at 47.6 percent. Most of these markets, however, remained roughly in line with last year’s pace.

Several universities posted stronger year-over-year gains. Ohio State led the way, reaching 74.9 percent preleasing, up 19.9 percent from the prior year. University of Oklahoma followed at 76.4 percent, up 18.8 percent, while University of Iowa reached 81.9 percent, up 17.9 percent. In many of these markets, the growth reflected a recovery following recent pressure from new supply.

Some large markets continued to trail last year’s leasing pace as new construction weighed on performance. North Carolina State was 59.6 percent preleased, down 10.7 percent year-over-year, while University of Tennessee-Knoxville reached 67.5 percent, down 9.9 percent. Purdue University, University of Arkansas and University of Central Florida were also behind last year’s levels, with each market expected to deliver more than 1,600 beds in 2026 and 2027.

Markets where enrollment growth has outpaced new supply continued to post the strongest rent increases. Auburn University, where enrollment rose by more than 3,000 students over the past three years while only 1,400 beds were added, recorded 8.3 percent annual rent growth in March. Nevada-Reno followed a similar pattern, with enrollment up more than 3,000 students since 2022 and only 734 beds added, pushing rent growth to 8.2 percent.

Meanwhile, markets with recent rent gains and new development faced more pressure. According to the student housing report, Purdue rents fell 9.2 percent in March, returning to September 2024 levels. University of Arizona rents declined 8.1 percent year-over-year, while North Texas and Baylor posted drops of 7.5 percent and 6.5 percent, respectively.