National Multifamily Report – March 2023

Short-term rents resume rise after four months with negative growth, according to Yardi Matrix data.

Year-over-year rent growth, through March. Chart courtesy of Yardi Matrix

Despite persisting volatility in the financial markets, multifamily property fundamentals remain stable. The average U.S. multifamily asking rent increased slightly in March, up $3 to $1,706, according to Yardi Matrix’s latest survey of 140 markets. Year-over-year rent growth remained on a slowing trend, up 4.0 percent, 90 basis points below February’s rate and the lowest level since April 2021. Moreover, 21 of the top 30 Matrix metros posted rent gains in March, while the national occupancy remained unchanged during the first quarter of 2023. Meanwhile, the average rent for single-family rentals gained $5 to $2,079, a 2.8 percent year-over-year increase. Occupancy in the sector remained strong at 95.5 percent in February.

The first quarter of the year was the first in the past decade with no gains in multifamily rents. Considering the current landscape, heavily focused on the Federal Reserve-induced economic slowdown, bank collapses (affected by the interest rate hikes) and the substantial deceleration in rents, demand remained robust. Still, rent growth in 2023 is expected to be modest.

Midwest and Northeast markets were at the top of Matrix’s top 30 metro rankings, still led by Indianapolis (8.6 percent). Next in line were New York and Kansas City (6.9 percent), Boston (5.8 percent) and Chicago (5.2 percent). The national occupancy rate slid down 10 basis points to 95.1 percent in February, attributed to a slight decline in the Renter-by-Necessity occupancy rate, down 10 basis points to 95.2 percent in February.

On a monthly basis, rent growth turned positive after four months of contractions, led by metros in the Acela Corridor—Boston (1.0 percent), Washington, D.C. (0.8 percent), New York (0.6 percent) and Baltimore (0.5 percent), and Indianapolis (0.8 percent). By asset class, Renter-by-Necessity rents rose 0.3 percent and upscale Lifestyle rents increased 0.2 percent. The most distinctive change recorded in March was the rebound of Lifestyle rents, as most metros posted negative growth a month ago. Specifically, 19 of the top 30 metros recorded increases in March, and 10 posted declines. In the RBN segment, 21 metros marked monthly gains, and rents fell only in eight. Seattle had a high bifurcation between Lifestyle and RBN, declining 0.3 percent in the former and increasing rising 1.3 percent in the latter, reflecting increased demand for lower-priced units.

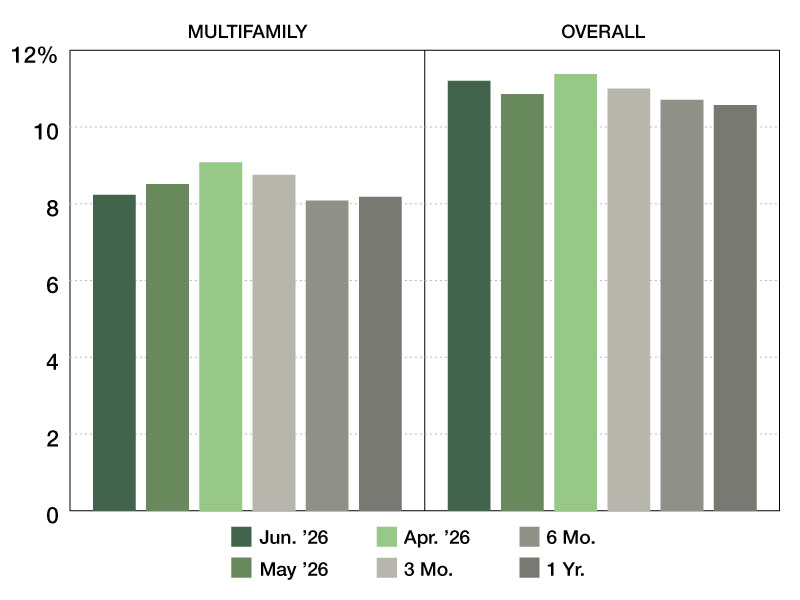

National renewal rent growth increased by a substantial 30 basis points to 9.3 percent year-over-year through January. This is surprising as the metric had been waning since peaking at 11 percent in the fall and is expected to drop in line with the levels of asking rent growth, at 4.0 percent in March. This signals several things: that many renters still afford increases, that demand is decreasing but slowly, and that those who are considering moving to reduce their monthly expenses have limited options in many metros. Meanwhile, national lease renewal rates continued to decline, down to 63.9 percent in January from 65.2 percent in December.

The single-family rental average asking rent rose 2.8 percent year-over-year in March, an 80-basis point decrease from a year ago. This is the equivalent of a $5 gain to $2,079 and comes at the heels of a weak fourth quarter in 2022. Occupancy clocked in at 95.5 percent in February, a 0.6 percent year-over-year decline. Although benefiting from the still tepid single-family home sales, the sector is not spared from financial challenges as mortgage rates and prices remain high. Tight capital market conditions pushed some SFR owners to announce layoffs and/or cutbacks in acquisition plans, while others, growing through build-to-rent programs, face increased costs of construction financing, which is further complicating these efforts.

Read the full Yardi Matrix report.