National Multifamily Report – February 2026

Advertised rents have been circling the same figure for 18 consecutive months, according to Yardi Matrix.

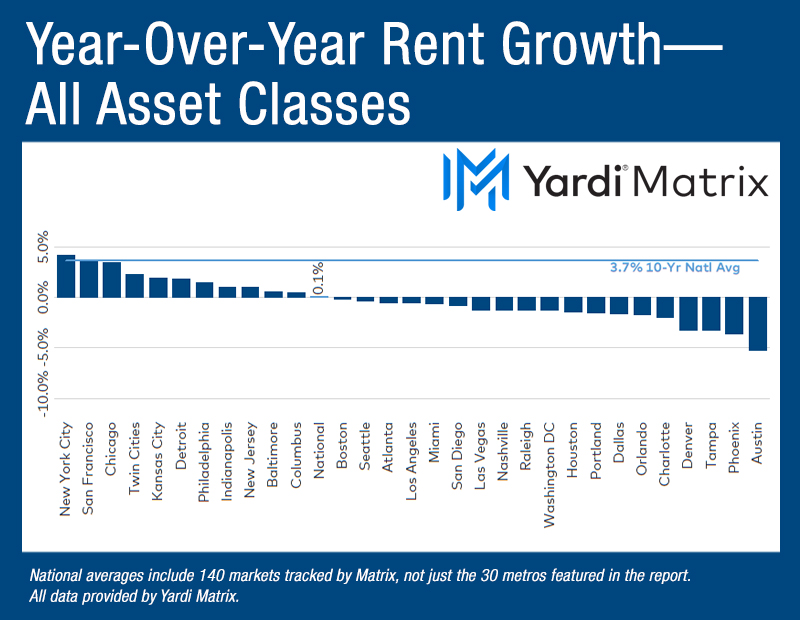

February is typically slow, and the previous month was no exception. U.S. advertised asking rents remained flat at $1,740, marking 18 consecutive months of little-to-no movement, according to Yardi Matrix’s latest survey of 140 markets. The annual growth rate stood at 0.1 percent, down 10 basis points year-over-year. Over in the single-family build-to-rent sector, the same short-term stagnation occurred, although the long-term story was slightly different, with a 0.4 percent annual decrease to $2,191 in February.

Yearly advertised multifamily rent growth fell 0.1 percent as occupancy rates also tumbled 0.4 percent to 94.3 percent in February. Roughly half of Matrix’s top 30 markets registered occupancy declines of 0.5 percent or more, with nearly all such metros also having annual rent growth in the red. A few exceptions consisted of Atlanta and San Francisco, with both metros recording positive occupancy shifts of 0.2 percent. In terms of rent growth, San Francisco (3.6 percent) was among the primary and Midwest markets that saw improvements, alongside New York (4.2 percent), Chicago (3.5 percent) and the Twin Cities (2.3 percent), to name a few.

Gateway markets back in business amid demand realignments

Monthly gains coalesced around gateway metros, with New York (0.9 percent advertised rent growth), San Francisco (0.5 percent) and Chicago (0.3 percent) bucking national trends. Midwest markets such as the Twin Cities (0.2 percent), Kansas City (0.1 percent) and Detroit (0.0 percent) are supported by steady demand and a deficit of new supply, though they lack the strong income growth and return-to-office policies of gateway metros, which ultimately limits their rent growth potential.

Multifamily demand is likely to temper as population growth across the nation has dropped sharply. Between July 2024 and July 2025, the population increased by 1.8 million, a figure below the annual average dating back to 2000, and the lowest increase in half-a-decade. Sun Belt states such as Texas, Florida and the Carolinas recorded the highest population increases; however, the growth rate slowed significantly. In fact, Texas and Florida were also among the states that witnessed the sharpest pullback in the rate of expansion. Lower immigration and domestic migration were some of the factors that drove last year’s poor performance. At a granular level, the same forces could disproportionately depress demand across metros that rely heavily on such population flow.

Single-family build-to-rent rates stood at $2,191 in February, retaining their previous monthly reading. Yet, the rents were down 0.4 percent year-over-year, aligning with occupancy trends, which also dropped 0.5 percent within the same period, ticking down to 94.5 percent in February. Meanwhile, industry trade groups, such as the NRHC and NMHC, continue opposing the 21st Century ROAD to Housing Act, a federal legislation that prohibits institutional SFR investment. Although the bill would not affect the BTR product, its implications could make the sector unattractive for many institutions.

Read the full Yardi Matrix multifamily real estate report.