MARKET SNAPSHOT: Challenges in Getting Projects to Pencil Out Helps Denver Absorb Its Current Stock

Denver--A tremendous influx of new units in the early 2000s led to a lack of new construction in Denver in the years leading up to the last housing bubble burst, which, in effect, allowed the market to remain relatively stable.

Denver—A tremendous influx of new units in the early 2000s led to a lack of new construction in Denver in the years leading up to the last housing bubble burst, which, in effect, allowed the market to remain relatively stable.

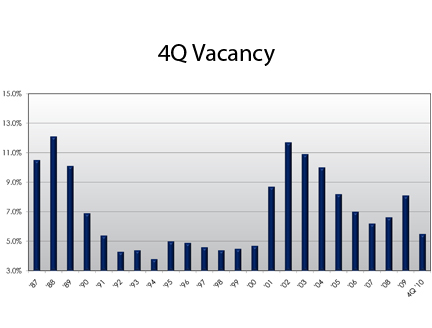

“We saw our market on fire in the late ‘90s and 2000; the break started coming in 2001-2002 with the tech wreck,” recalls Terrance Hunt, principal, ARA-Denver, who adds that the market’s vacancy peaked in the third quarter of 2003 at 13 percent, on a quarterly basis.

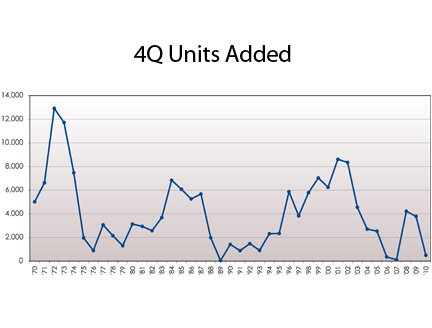

The market saw the addition of 20,000 new units between 2001 and 2002, Hunt tells MHN. “That is as many units as [the market] had delivered in the past 20 years … so it was a perfect storm to create an environment where … trying to lease up those units really took our market down.”

Because of the need for absorption, the market hasn’t seen much in the way of rent growth through the 2000s. “While the rest of the country was ramping up and housing was on fire, Colorado was just finding its legs,” Hunt points out. Consequently, “we didn’t have any oversupply problems and our rents were already depressed.”

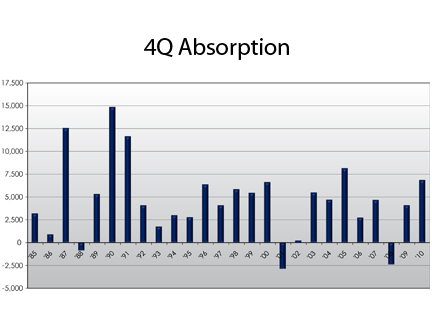

Since the “initial bubble burst,” Hunt notes that the market has experienced record absorption and absorbed 6,800 units in 2010 alone. (It added only 438 units during the same period). Meanwhile, the market is currently 5.5 percent vacant.

“We still have not overbuilt because construction costs have gone up, and rents haven’t grown to justify new construction,” says Hunt.

Effective rents are currently averaging $1.00 per square foot market-wide; Hunt notes that rents will need to be at least $1.20/square foot for the least-expensive product to get built. In the downtown market, rents—which are currently $1.50-$1.65 per square foot—would need to be at least $1.80 per square foot before developers can make the math work, Hunt adds.

Hunt notes that the market’s organic growth will continue to increase demand in the market; “we have over 30,000 kids every year turning 21 in Denver,” he says. “We only have 15,000 vacant units now market-wide. The demand is there.”

The transaction market, meanwhile, has picked up since 2009. Last summer, before the run up in interest rates, cap rates were in the mid-5 percent range, Hunt reports, though he adds that they have gone up approximately 25 to 50 bps.

“What’s taken some of the steam out of that is evidence of rent growth; people are still underwriting lower cap rates than they typically would with the cost of debt and we’re seeing some interest-only money in some assets,” says Hunt. Current cap rates are between 6 percent and 6.5 percent for Class A assets, and Hunt notes that there isn’t much product available over 7.5 percent.

The current buyer profile, says Hunt, is mostly “private syndications with maybe an institutional piece of money. We’re not seeing the REITs in Denver at this time, but they are calling us” about assets in core, downtown locations.

One of Denver’s bright spot is its organic growth, Hunt tells MHN. “The biggest facet of our demographics is the echo boomers because our greatest population boom was in the ’70s with baby boomers that came with their kids; the kids are coming to age of being renters.”

{kind=link}

{kind=link}

{kind=link}