Investment Opportunities for the Coming Year

While the usual suspects show market potential, some say that there really are no markets to avoid in 2011.

Not surprisingly, New York, Washington, D.C., Boston and other high-barriers-to-entry cities make it to the list of top apartment markets in 2011. As for the bottom markets, the apartment industry appears positioned to stage such a strong comeback this year that investment sales advisors counsel that all markets—even the currently weak ones—may be coming into play as investment choices.

“In our view, there are no markets to be avoided,” says Gleb Nechayev, senior economist at CB Richard Ellis, Global Research and Consulting, Econometric Advisors, in a typical assessment.

Top 2011 markets

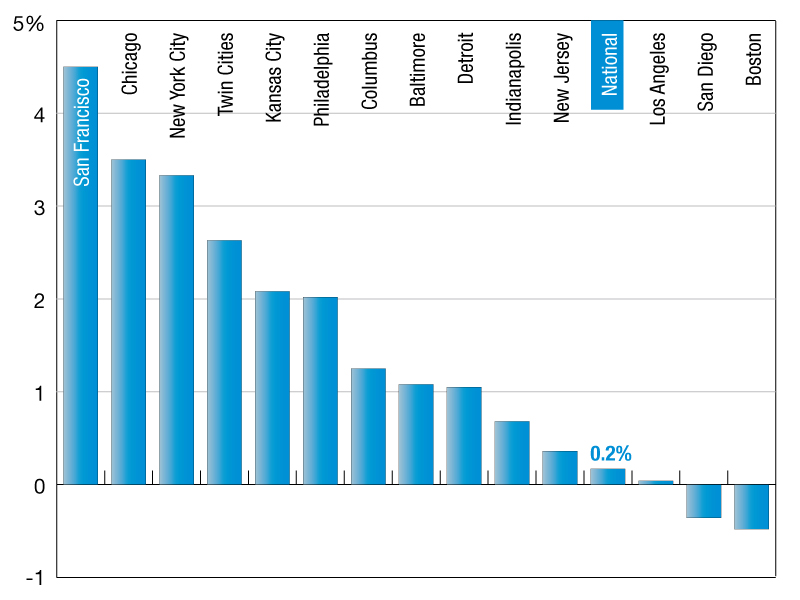

The top apartment markets of 2011 will be New York, Washington, D.C., Boston, San Diego, San Jose, Denver and Seattle, in the view of Hessam Nadji, managing director of research and advisory services at Marcus & Millichap Real Estate Investment Services. In particular, Nadji singles out New York, Washington, D.C. and Boston as markets that will provide the safest investment opportunities as well as the highest returns.

All of Nadji’s favorite markets feature the lowest apartment vacancies in the nation combined with the least prospects for new construction deliveries going forward. In New York, San Jose, San Diego and Washington, D.C., apartment vacancies are already in the low-3 percent to high-5 percent range, and Seattle has a vacancy of about 6 percent, says Nadji. These markets will enjoy strong rent growth this year that will trend in the 5 percent to 8 percent range, well above the national average, he says.

Austin, Texas; San Jose, Calif.; Boston and Northern Virginia are the top 2011 apartment markets picks of Peter Muoio, senior principal of Maximus Advisors (Maximus provides research services to ARA Research in the multifamily housing field). Muoio makes his endorsements based on the potential for short-term value appreciation. All these markets, he says, will have double-digit gains in values from the market trough in 2009 to fourth quarter 2013. Muoio’s forecast calls for apartment values to increase by 30 percent in Austin, 28 percent in San Jose, 20 percent-plus in Northern Virginia and 12 percent in Boston during this period.

At the top of Muoio’s ranking, Austin is experiencing high vacancies: supply in the market will be diminishing to almost zero while demand stays “very, very strong,” says Muoio. Texas is known for over-building and over-leverage, he cautions, but the state has not experienced a severe recession, and the state government is in relatively sound fiscal condition. Moreover, Austin has a high-tech industry. The vacancy rate in Austin is “moving down very rapidly,” says Muoio, from 11.1 percent to 8.2 percent currently. “Expect that kind of rapid recovery” in the market’s rents and NOI as well, he adds.

While the criteria used for selecting the top markets are vacancies for Nadji and value appreciation for Muoio, Nechayev, of CB Richard Ellis, bases his apartment market recommendations on economic rents obtainable today compared to what they were at market peak. “Some markets have already returned, or are very close, to their previous market peaks, while others are still very far from the previous peaks,” Nechayev points out. In effect, Nechayev recommends that the analysis of top markets takes into account where they are in the business cycle. If they are still far from the peak, they are in recovery mode and may not return to their peak rent levels this year. On the other hand, if they are close to their peak rent levels, they may already have recovered.

Based on this standard of comparing current and peak effective rents, Nechayev’s top apartment markets selections for 2011 include Washington, D.C., Baltimore and Pittsburgh, as well as the smaller markets of El Paso, Texas, and Louisville, Ky. These are all cities in which the average apartment revenue (defined as effective rents times occupancy) in the third quarter of 2010 were only 2 percent below the levels attained in the previous market peaks.

The Washington, D.C. apartment market, says Nechayev, has already recovered, and it is now showing effective rents comparable to those of the late-2000s. Nechayev also cites Boston: although Boston has experienced some home-price declines, single-family housing prices in that market have not been battered, unlike some of the other markets.

Bottom 2011 cities

As for the weakest apartment markets of 2011, all three experts assert that all markets, no matter their position on rankings, can be candidates for investments this year. “Here’s what’s very interesting for 2011: this will be the first year for investors to do well in strong and weak markets because the recovery will be broad-based and not limited just to the best markets,” explains Marcus & Millichap’s Nadji. He adds, “There are opportunities in both good and bad markets because everyone’s recovering.”

Muoio explains there are certain macro factors that will universally boost occupancy rates for multifamily housing this year. Indeed, the continuing drop in homeownership rate is due, in large part, to the lack of confidence in home-buying at present. Also, evidence is emerging of an increase in household formation that typically occurs in the early stages of a recovery. Demographics are “incredibly positive,” with young adults entering the prime renter age group at the rate of about 500,000 per year, says Muoio. At the same time, there has been a nationwide shutdown in new construction. “We are seeing a window of low supply combined with a pop in demand, so vacancies have fallen very quickly,” says Muoio.

Indeed, the improvements in many of the weakest apartment markets have been observed to be rapid. Muoio notes that there are no areas in which rents and occupancy levels are still falling. And Nadji says that even in markets with higher-than-average vacancy rates, vacancies have already dropped by 100 to 250 basis points, implying that concessions will be burned off in even those lagging markets in 2011. “Universally, across the locations we are examining, all markets are improving ahead of schedule at an even faster rate than expected,” agrees Muoio.

Nadji’s selection for the “bottom” apartment markets will be those with the highest vacancies: Las Vegas, Phoenix, Jacksonville, Fla., the Inland Empire, Atlanta and Houston. These are markets that have suffered more than others as a result of the housing crisis, overbuilding, or both. Consequently, these markets have high vacancy rates of about 9 percent to 11 percent—well above the national average (about 6.5 percent), he says. Apartment occupancies in these locations, however, should improve by about 2 percent over 2011, and effective rents should increase as a result of concession burnoff, Nadji forecasts.

For Muoio, the weakest apartment markets in 2011 will be markets that register the least degree of value appreciation. These will be cities that have been particularly hard-hit by the recession and housing downturn: Las Vegas, Riverside, Calif., and San Bernardino, Calif., says Muoio. Still, these markets will experience “modestly” higher valuations this year compared to what was registered at the market trough in 2009, he says.

Indeed, even in these markets, there is “going to be very dramatic improvement in vacancies,” Muoio predicts, although it will take a while before rents will increase. Already, apartment vacancy levels in these cities have begun to improve, says Muoio. And in Las Vegas and San Bernardino, in which there historically has been a tendency to overbuild, vacancies will drop from their peaks as the markets recover.

According to Nechayev, apartments in the following cities are the furthest from their market peaks: Phoenix, Las Vegas, Atlanta, Jacksonville, Fla., Los Angeles, and Seattle. These markets show average revenues (effective rent times occupancy) that are 10 percent or more below their previous high points, says Nechayev.

Nechayev predicts that some of these cities will definitely see apartment rents continue to fall in the near term, but assuming the national economic recovery strengthens through 2011, they could begin to see rent growth in 2012. In the near term, Phoenix for example, will see more risk in 2011—there is still a lot of single-family overhang, he says.

The fact that these markets are the weakest may not by itself be a reason to exclude them as locations for investments next year. “The momentum in even the weaker markets is pretty strong, so we expect rents to increase in these markets,” says Nechayev. Moreover, because they are furthest from their peaks, they may have greater latitude for investment growth compared to the strong markets that may already have recovered, Nechayev points out. And there are plenty of distressed opportunities in Phoenix, for example. “One could argue that places such as Phoenix could offer better opportunities, depending on the objectives of the investor,” he says.

Time to take more risks?

While the bottom apartment markets may now be ripe for investment, a word of caution is in order as there are also plenty of investment risks. While they may be filling quickly, many of the bottom-ranked markets—Las Vegas, Denver or Phoenix—are located in traditionally high-construction areas, notes Nadji. So while investors can feel secure that they will see apartment rent growth for a number of years in some of the safest high-barriers-to-entry cities, investors may need to adopt more of a “get-in-and-get-out” mentality for the bottom-ranked markets, Nadji explains. Moreover, the foreclosure crisis in many of these markets has not bottomed yet.

Nevertheless, if they keep such risks in mind, investors may be able to step out of the safest apartment investment zones in 2011 in view of the strong improvement in fundamentals. “One year ago, it made

sense to subscribe to a conservative investment strategy,” says Nadji. But “in 2011 and 2012, it does make sense to become more risk-tolerant, though we are not suggesting you throw caution to the wind.”