Insurance Burdens Stymie Investment

The growing scarcity of coverage due to escalating climate risk puts much-needed housing capital in jeopardy.

It’s not the high cost of property insurance that’s likely to chase many homeowners and real estate investors out of California, Florida and other high-risk coastal markets like Texas and Louisiana, but rather the unavailability of property insurance at all, since many insurers licensed to do business in these states are cutting their losses by pulling out.

Those insurers are not renewing policies or writing new business, and those still doing business in high-risk regions are raising premiums and deductibles, limiting their level of liability by capping the policy ceiling and eliminating coverage for certain climate-related damages, such as wind, fire and water damage from hurricanes, wildfires and flooding.

READ ALSO: Next Up? Stay in the Mix Till 2026

State Farm, Allstate, Cincinnati Insurance Cos., AmGUARD Insurance Co., Falls Lake Insurance, The Hartford, Tokio Marine American Insurance Co., American National Insurance, and Trans Pacific Insurance Co. are all pulling out of California, and Farmers Insurance, Progressive, AAA, Bankers Insurance, AIG and Lexington Insurance Company are leaving Florida or reducing their presences there—especially along the coast. Additionally, six insurers are in liquidation in Florida due to losses that drove them insolvent.

Why insurers exit certain markets

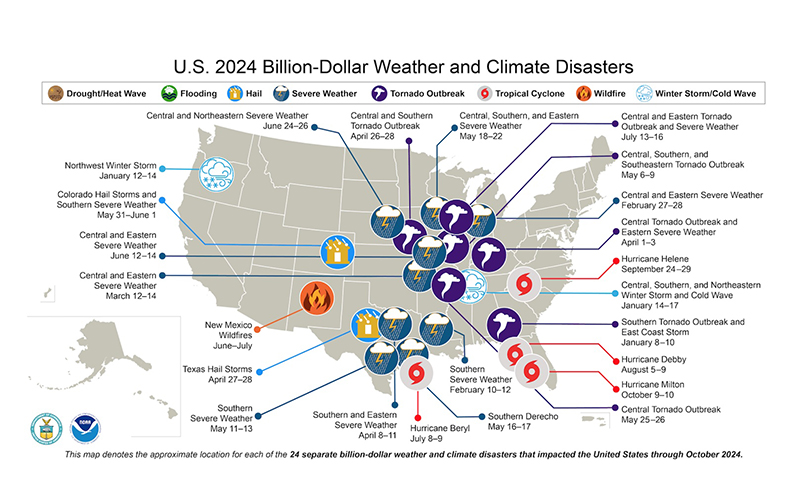

Property insurers have suffered tremendous losses over the last seven years, with 137 billion-dollar disasters that killed more than 5,500 people and cost more than a $1 trillion in damages, according to climate.gov.

Barry LePatner, founder of law firm LePatner & Associates LLP and LePatner Project Solutions LLC, noted that prior to Hurricanes Helene and Milton, the National Oceanic & Atmospheric Administration had recorded 24 weather/climate disaster events so far this year with a total cost of $61 billion. The two latest hurricanes are expected to add another $100 billion or more, he said. The four hurricanes (Beryl, Kirk, Helene and Milton) alone, are estimated to cost between $127 billion and $129 billion, reported USA Today.

Meanwhile, there are 10 major wildfires burning in California, Oregon, Texas, Idaho, Montana, Utah, New Mexico and Wyoming, according to the Fire, Weather & Avalanche Center. Since Jan. 1, 51,320 wildfires have burned 8.14 million acres, reported the National Interagency Fire Center. Wildfires cost between $400 and $900 billion annually, according to a report from the Joint Economic Committee Democrats.

Drastic rise in insurance costs

Since insurers spread their loses over their entire book of business, property insurance costs have accelerated across the board since 2020, rising along with the growing magnitude and frequency of climate-related disasters, noted LePatner, but more so in California and Florida, which are prone to frequent wildfires and hurricanes.

Insurance premiums rose 106 percent overall between 2020 and 2024, according to PwC. Veronika Torarp, a principal in PwC’s Climate Risk and Insurance Practice, noted that non-climate factors, such as inflation and reinsurance expense, also have played a role in rising insurance cost. For example, Nebraska’s property insurance rates more than doubled over the last year, although the state generally has a lower level of climate risk than some other states, Torarp said.

Much of the drastic rise in Nebraska’s premiums is attributable to supply-chain issues and labor shortages, which are driving up the cost of home repairs and replacement, but also to more severe weather events, reported NPR.

at Hub International

Premiums rose between 15 and 30 percent nationwide since 2020 for properties without a claims history, but their coverage has remained unchanged, said Marc Gordon, principal, co-president & CFO at Investors Management Group, a multifamily investment firm that owns and manages 5,200 apartment units nationwide. Premiums tripled, however, over the same period for properties with prior claims and continue to rise exponentially in regions at high risk for catastrophic climate events, he noted.

But premiums are only part of the story. Chip Stuart, practice leader for Real Estate Specialty at global insurance brokerage Hub International, noted that in California, for example, deductibles have more than doubled over the past five years, going from $5,000 or $10,000 to $25,000. Insurers remaining in the state are also limiting their liability by reducing the coverage ceiling to $2.5 million to $5 million.

“If I have a multifamily building in, say Santa Monica, who am I going to insure it with?” Stuart remarked. “Well, you’re going to have to come to somebody like Hub, and we’re going to put it out into the wholesale markets, and you’re probably going to have maybe one or two or three carriers insuring it.”

Alternatives to traditional insurance

In California, property owners in high-risk areas must now rely primarily on “non-admitted” insurers (out-of-state insurers not licensed to do business in California), which are considered a wholesale line or surplus market, to provide coverage, Stuart continued. He noted that these insurers charge high premiums. In addition, since non-admitted insurers must pay a 3 percent tax to sell business in the state, they pass it on to clients. Taxes collected, however, go into the state’s FAIR fund, an “insurance-of-last resort” program, which is managed by the state, with coverage provided by “admitted” insurers.

Wholesale-line insurers have treaties (contracts) with reinsurers but have restricted policy coverage ceilings to no more than $5 million, Stuart said. Therefore, insurance brokers like Hub must piece together multiple policies to provide multifamily owners adequate insurance coverage to meet lender requirements, including coverage of damages related to climate-related events.

Additionally, 32 states and the District of Columbia offer one or more forms of last resort insurance, such as FAIR plans, beach/wind plans, or Citizen Property insurance, which cover both residential and commercial property damages in markets where private insurance is unavailable or weather-related perils are excluded from standard policies.

Enrollment in these programs, which generally charge more than standard insurance policies, has increased dramatically in recent years, especially in high-risk regions, reported LowerMyBills. In California, the premium for the FAIR plan in 2024 averages $3,200 annually on a $300,000 home, compared to $1,480 a year for a typical homeowner policy. These policies also have coverage limits. In California, the top payout is limited to $3 million, which is generally enough for residential properties but may not be enough coverage for commercial properties, such as apartment buildings and hotels

Ramifications of insurance issues

and LePatner Project Solutions LLC

Property insurance “is the basic underlying element” of getting a loan, LePatner noted. “If you can’t get that insurance, or you’re paying ridiculously high premiums for increased risk, then lenders are going to say, ‘Why should I be a backstop for a development that is in such a high-risk area?’”

Property values may drop in markets with extreme insurance costs, Torarp suggested, citing a report from CBRE that attributed a 3.6 percent decrease in multifamily property values nationwide since Q4 2019 due to rising insurance costs. The report noted, however, that property values have not been impacted by insurance costs in high-risk markets with strong housing demand, like South Florida.

As a result, investors are beginning to leave high-risk states, too. “The risk is substantial, and investment decisions being made are very, very much in concert with the impact of these insurance issues,” LePatner suggested. When making decisions, investors must factor in operational expenses like insurance costs to determine if an investment has merits for themselves and their investors.

He said that high insurance costs and limited coverage in these markets has increased risks while reducing net operating income and the ability to secure loans without additional policies to cover various potential perils—if available.

Fannie Mae, for example, states that if a property is in an area prone to specific weather perils, then coverage needs to be purchased for those perils. “Properties must have separate windstorm coverage if that is excluded from standard catastrophe loss coverage and flood insurance if located in a flood plain,” Torarp explained.

“When you see 400 percent, 600 percent increases over several years with higher deductibles and less coverage, No. 1, investors are more concerned and take their business and money elsewhere,” LePatner noted. “No. 2, in states such as California and Florida, insurers have stopped writing coverages, so you can’t even get coverage in certain markets, which means you can’t get a loan from a lender.

“The ramifications are that investors and lenders are going to less volatile areas, areas where they have a chance of securing reasonable insurance coverage without facing risks that require putting up major dollars for risks because the deductible is so much higher.”

Developers LePatner has spoken with in with new investments in Kansas or New Mexico or other low-risk markets, say they are happier in these places because they don’t have concerns about insurance coverage, and it’s less expensive to build there than in California or New York or Florida.

Investors Management Group is among the multifamily investors that decided to steer clear of high-risk markets. For example, the company decided a few years ago to exit the Florida market because of the risks and rising insurance costs.

“We also felt the value proposition did not support operating in some Florida coastal locations with high chances of natural disaster,” Gordon said. “We didn’t want to be in a market where there is an extremely high risk each year that the property will be flooded or subject to material damage.”