Increased Demand Pushes Up Rents in Las Vegas

The city’s multifamily recovery is a safe bet, given that it ranks among the top 10 metros for population growth.

Las Vegas rent evolution, click to enlarge

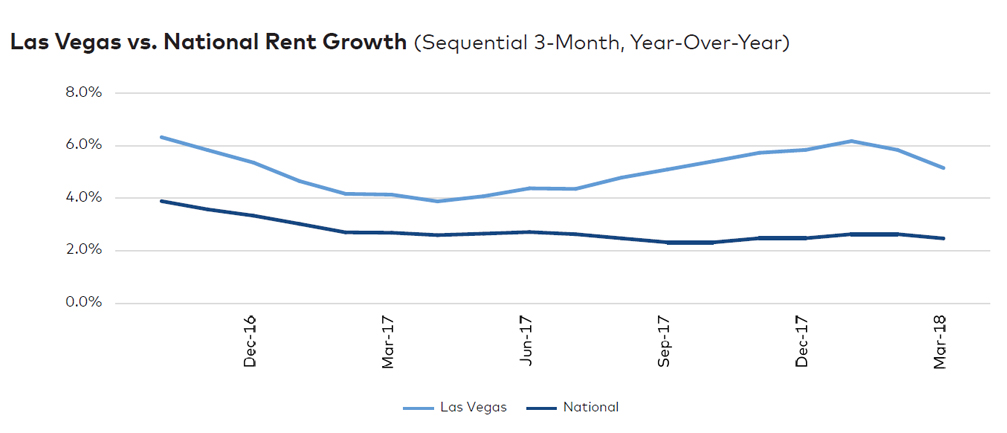

Despite having tourism and leisure and hospitality as its main economic drivers, Las Vegas has been a late bloomer in this real estate cycle. But the city’s full recovery is a safe bet, given that it ranks among the top 10 metros for population growth and had the second-largest employment gain in the country, at 2.9 percent in 2017. These factors have pushed rents up 5.3 percent year over year through March, to $980, still trailing the $1,372 U.S. average.

Up by 18.4 percent, construction led the metro’s employment expansion in 2017, adding 11,000 new positions. In-progress deliveries exceed 5,200 apartments for rent in Las Vegas, 4,300 of which are slated for completion by year-end. Moreover, several projects are likely to maintain this trend in the coming years: The $1.9 billion Las Vegas Riders NFL stadium broke ground in January and needs about 3,000 workers, while the $1.4 billion expansion of the Las Vegas Convention Center calls for more than 7,900 employees.

Transaction activity has softened in 2018, with some $317 million in apartments trading through March, following two consecutive years that each saw sale volumes above $2.4 billion. Per-unit prices remained virtually flat across the metro, continuing to mirror investors’ focus on Renter-by- Necessity properties. Yardi Matrix forecasts rents will rise 4.8 percent in 2018.

Read the full Yardi Matrix report.