How Multifamily Construction Trended in 2022

Volume through the third quarter was on par with the same period of 2021, according to Yardi Matrix data.

Image by ElasticComputeFarm via Pixabay

This past year proved unpredictable not just for those acting in the investment market, but for developers as well. Inflation woes cast a shadow on the multifamily construction market, as the cost of capital is still rising. However, the severely undersupplied housing stock offers a strong proposition to developers dealing with construction costs, at least in some parts of the U.S., Yardi Matrix development data shows, based on its coverage of all multifamily properties of 50-plus units across 140 markets. To see which markets were most resilient to rising inflation and interest rates from a development standpoint, we focused on construction starts-related data in 2022.

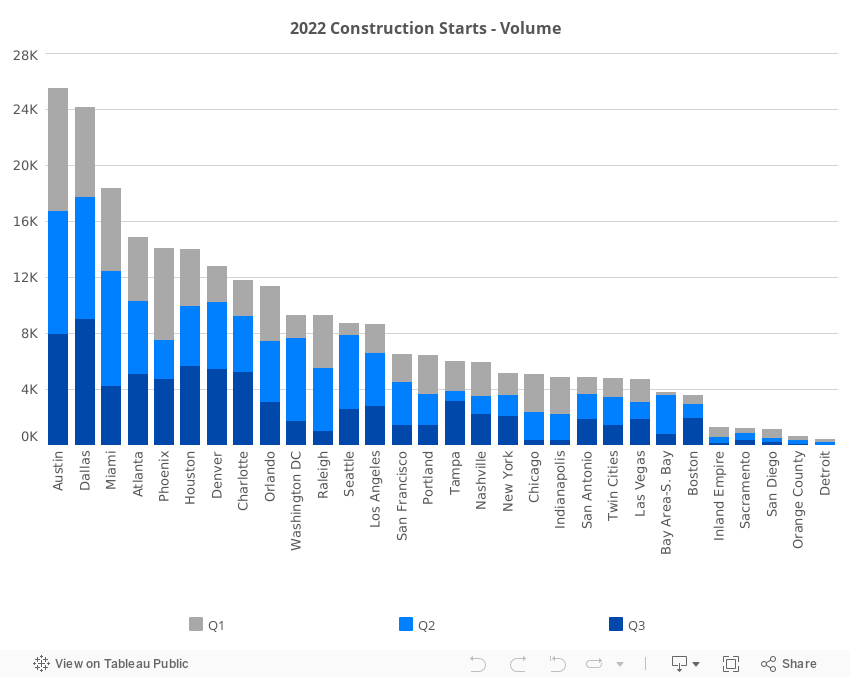

Nationally, the total volume of construction starts in 2022 through the third quarter amounted to 363,575 units—one-third of the total number of units under construction at that time—and just 3.2 percent below the figure recorded during the same interval last year (375,756 units), a year that ended with nearly half a million units breaking ground across the country, more than in any prior year. Lifestyle properties dominated the pipeline, accounting for 80 percent of the projects that broke ground during the first three quarters of the year.

There were roughly 1.1 million units under construction across the U.S. as of the third quarter of 2022, 7.4 percent of existing stock. Moreover, the data reveals a steep decline in the number of deliveries as some 271,000 units were added to the inventory in 2022 through the end of the third quarter. That accounts for 1.8 percent of total stock, trailing the 318,449 units added to the inventory in 2021 during the same interval.

Despite mounting woes plaguing the construction industry, of the total 121 metros tracked, the number of projects breaking ground during the first three quarters of the year rose in 45 markets—compared with the first three quarters of 2021. In another 20 markets, the volume of construction-starts remained flat—sorted based on a growth/decrease margin of +/- 9.9 percent in construction starts on a year-over-year basis. The number of construction-starts decreased in 56 markets.

Looking at Yardi Matrix’s top 30 markets, the pattern remains fairly similar: in 13 markets construction-starts increased, in three of these markets figures remained virtually flat, and starts decreased in 14. One thing that stands out is the pool of metros that either posted gradual increases in the number of construction-starts by quarter or had the third quarter as the strongest interval, seemingly unaffected by rising interest rates and ensuing economic fallout—Boston, New York, Tampa, San Antonio, Dallas, Charlotte, Denver, Houston and Las Vegas.

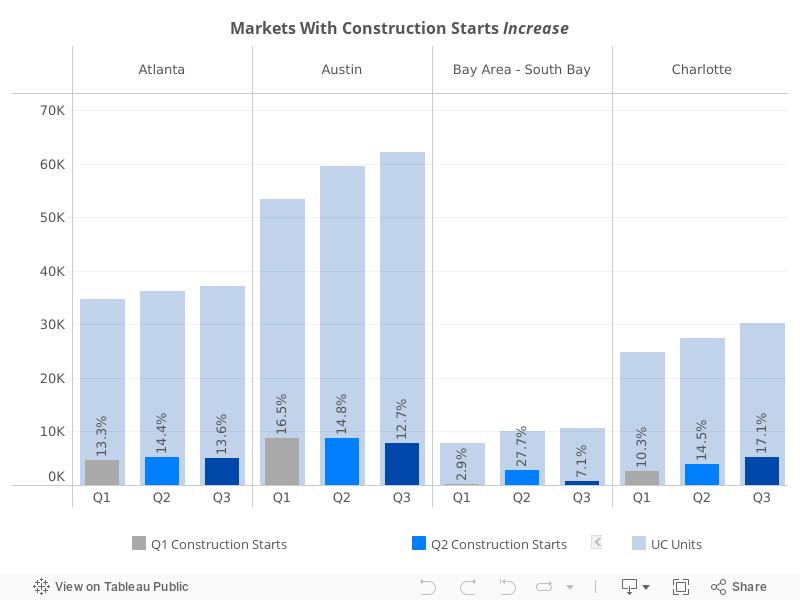

Markets with multifamily construction-starts increases

Through September, multifamily construction starts in these 13 markets amounted to 142,701 units, a 35.7 percent increase compared to the same interval in 2021. Additionally, units that broke ground this year account for 40 percent of the total number of units under construction in these metros (352,879 units). Almost all of these markets benefited from the large migration during the pandemic (except San Jose, but the market has been rebounding nicely in 2022), so it’s not very surprising that construction starts would remain high. However, as migration cools down, it will be interesting to see how much of these units will be absorbed and how fast.

Construction starts increases over the last year ranged between 13 percent in Charlotte and 155 percent in Indianapolis. Looking at these two metros up close, by-quarter numbers stand out: in Charlotte, the number of units breaking ground increased gradually from the first quarter to the third (2,559 units in Q1, 3,997 units in Q2 and 5,198 units in Q3), while in Indianapolis, the dynamic was reversed—a strong Q1 with 2,634 units starting construction, followed by 1,818 units in Q2 and down to just 380 units during Q3).

Markets with a similar dynamic to Charlotte’s—less dependent on increasing interest rates—were only Denver and Houston. Markets sensitive to the Fed’s actions—with construction-starts progressively decreasing from quarter to quarter—were Chicago, Austin and Portland. The latter was one of the four markets which more than doubled the number of construction starts. The other three markets are San Jose, Las Vegas—both up 135 percent year-over-year—and Indianapolis.

Markets with the highest number of construction starts registered during the second quarter were Miami (8,237 of 18,381 units), Atlanta (5,212 of 14,850 units), Orlando (4,356 of 11,336 units), Raleigh–Durham (4,496 of 9,290 units) and San Jose (2,784 of 3,776 units).

In Austin, developers broke ground on 25,508 units, marking the highest volume of units breaking ground among major markets in the country. The figure is 56 percent above the volume of construction starts registered during the same interval last year. A close second by number of units that broke ground during this period was Dallas, with 24,176 units, followed by Houston with 13,975 units.

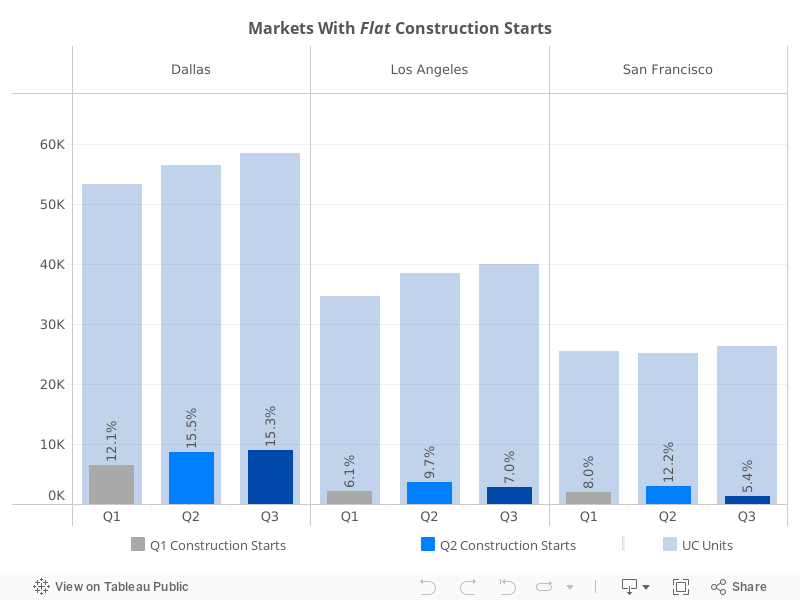

Markets with flat construction starts figures

In three of Yardi Matrix’s top 30 markets, the volume of construction starts was similar to that of last year. In large markets with strong demand for housing, the number of projects that broke ground during the period totaled 39,328 units, above the 37,670 units that started construction in the same interval in 2021. Furthermore, mirroring the national trend, the number of units that broke ground in these metros accounted for 21 percent of the total number of units under construction in these metros (124,792 units).

Of the three, Los Angeles marked a slight 4.3 percent decline in the number of construction starts. Still, the market posted a solid performance, starting the year at a slower pace, with 2,107 units in Q1, rising to 3,748 units during Q2 and moderating again during Q3, to 2,799 units.

San Francisco was just 40 basis points shy from making it into the pool of markets that posted increases in the number of construction starts, up 9.6 percent. The second quarter ranked first with 3,069 units breaking ground across the metro. The increase in the number of units that broke ground this year through September added to the upscale Lifestyle segment (3,645 units in 2022 from 3,072 units in 2021), while the new RBN volume was nearly identical (2,853 units in 2022 and 2,857 units in 2021).

In Dallas, developers broke ground to 24,176 units through September, 41 percent of the projects under construction and 6.5 percent above last year’s figure. The number of new projects breaking ground in the metro increased gradually from one quarter to the next—6,461 units in Q1, 8,745 in Q2 and 8,970 in Q3. With Dallas still relatively affordable, the bulk of construction starts were in Lifestyle projects (23,000 units), more than the 21,000-unit Lifestyle starts registered through Q3 in 2021.

Markets where multifamily construction starts decreased

In 14 markets, starts declined in 2022 through Q3 compared to the same interval in 2021, by as little as 10.4 percent in Phoenix to as much as 78 percent in Orange County. Combined, the total volume of construction starts by units in this category amounted to 23 percent of the total number of units under construction in these markets through September (281,011 units).

The most sensitive markets to the economic landscape shifts were Orange County, San Diego, the Inland Empire, New York City, Nashville, Tampa and Phoenix, as pointed out by the drop in construction starts during Q2. While Orange County, San Diego and the Inland Empire remained on a softening trend into Q3 when construction starts continued to decline, Nashville, Phoenix, New York and Tampa rebounded—the latter two marked their best figures during Q3.

The Twin Cities, Seattle and Washington, D.C. markets saw their best quarter for new projects breaking ground in Q2, and all had Q3 better than Q1. Detroit had strong deliveries, but it is the only metro with construction-starts coming to a halt in Q3. Only Boston and San Antonio kept on a steady upward trend from Q1 through Q3.

Phoenix is one of the markets that benefited the most from the strong migration during the pandemic, but demand appeared to be cooling off this year. The metro poster the lowest drop in starts among the markets in this group and the highest overall number of units started during 2022’s first three quarters. The year started with 6,581 units breaking ground during Q1, but marked a sharp drop during Q2 (2,775 units) and rebounded admirably in Q3 (4,738 units). A substantial 9,340 units were delivered through September.