Atlanta Multifamily Report – January 2024

Despite rental rates slipping, the city's pipeline has yet to shrink.

Atlanta’s relatively affordable cost of living and diversified economy boosted in-migration over the past decade, contributing to strong rental demand. Yet the nationwide slowdown, economic woes and robust deliveries have cooled transactions and dented gains. Rent development was down 0.5 percent on a trailing three-month basis as of November, to $1,657. Occupancy in stabilized assets also slid, down 130 basis points in 12 months, to 92.8 percent, as of October 2023.

In the 12 months ending in September, Atlanta’s job market expanded 2.3 percent, or 66,800 net jobs, trailing the U.S. rate by 10 basis points. Meanwhile, unemployment stood at 3.4 percent in October, on par with the state and 50 basis points ahead of the national average. Although still healthy, job growth and unemployment figures began to show signs of vulnerability. While education and health services (22,900 jobs) and leisure and hospitality (18,700 jobs) led gains, three other sectors lost 11,500 positions combined.

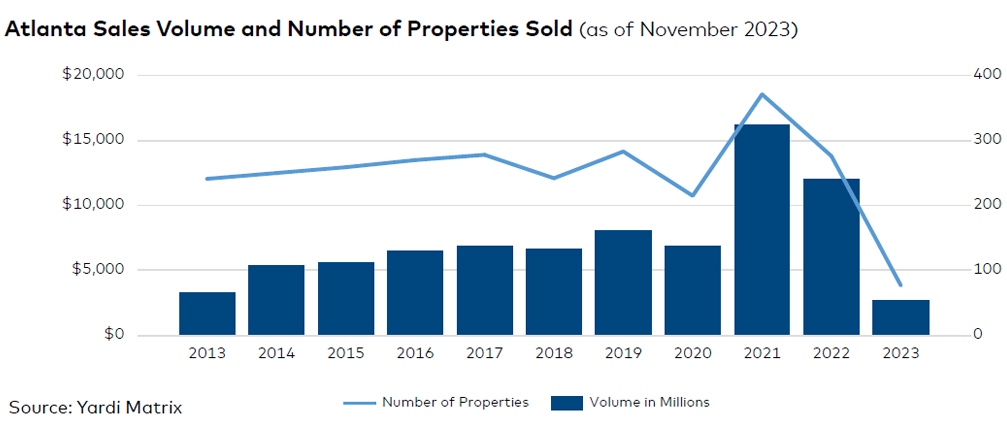

Developers brought 14,544 units online in 2023 through November, setting the stage for a new decade-high. In addition, the area had 37,867 units underway, placing Atlanta’s pipeline among the country’s top 10 busiest. Meanwhile, investors traded just $2.7 billion in multifamily assets in 2023 through November, the lowest volume in at least a decade. By comparison, the metro recorded $28.2 billion in deals during the previous two years combined.