National Student Housing Report – October 2025

Occupancy at Yardi 200 schools reached one of the highest levels in recent years, according to the latest Yardi Matrix report.

The U.S. student housing market ended the preleasing cycle on a strong note, with national occupancy estimated to reach 95.1 percent across Yardi 200 universities for the 2025-2026 academic year. It represents one of the strongest performances in recent years, rising from 93.6 percent in 2025. The increase was driven by consistent preleasing activity, strategic rent moderation, and renewed demand across mid-tier university markets.

Although 73 schools recorded lower occupancy rates compared to last fall, only 22 of them trailed behind by 5 percent or more—including The University of Texas at Arlington and Purdue University. On the flip side, 46 universities posted significant recoveries with occupancy increasing more than 5 percent year-over-year. Standout markets included University of Cincinnati, Washington State University and Syracuse University.

A total of 49 schools within Yardi 200 recorded 99 percent or higher occupancy, up from 38 last year. These included powerhouse institutions such as Virginia Tech, University of Missouri, Louisiana State University and University of Wisconsin.

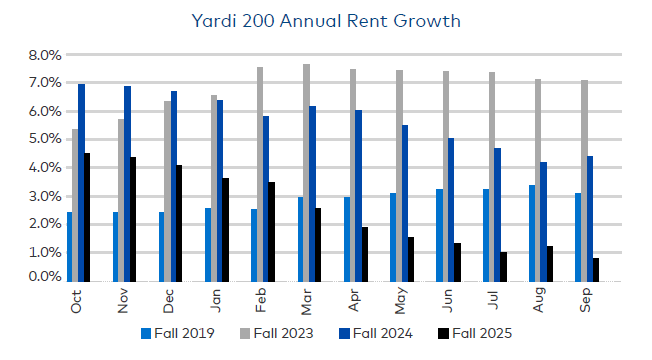

Annual rent increase continued to drop

Average student housing rents held steady at $905 per bed in September, just 0.8 percent in year-over-year growth—the slowest annual increase since Yardi Matrix began tracking the sector in 2017. Compared to the previous month, it rose $2.

The average rent for the leasing cycle was $912 per bed, representing a 2.5 percent annual growth—down from 5.7 percent in 2023–2024 and 6.9 percent the prior year. The slowdown comes from fiercer competition across markets, with operators using more strategic pricing to keep occupancy elevated—even if that means easing rent growth.

Markets that outperformed included University of Missouri, where rents rose 11 percent year-over-year, as well as University of Oklahoma (5.2 percent) and University of Florida (8.5 percent) However, several high-growth markets from previous years saw rent declines, including University of Tennessee (-8.1 percent) and University of Arizona (-6.1 percent).

Approximately 27,000 new beds were delivered nationally in 2025, a decrease from nearly 35,000 in 2024. Another 38,500 beds are under construction, with about 26,500 expected to come online next year. Institutions with notable new supply include Florida State University, University of Michigan and University of Texas at Austin.

In terms of investment volume, 76 student housing properties traded year-to-date as of September for a combined $3.7 billion. This marked a decrease from the 94 transactions totaling $5 billion during the same time frame of the previous year. Although the average price per bed dropped from $107,000 last year to $98,000, it remained well above pre-2024 levels, showing continued strength in student housing values despite fewer large portfolio deals.